- LME zinc stocks continue to rebuild into mid-Dec’25

- China’s proactive fiscal policy measures announced on 12 Dec

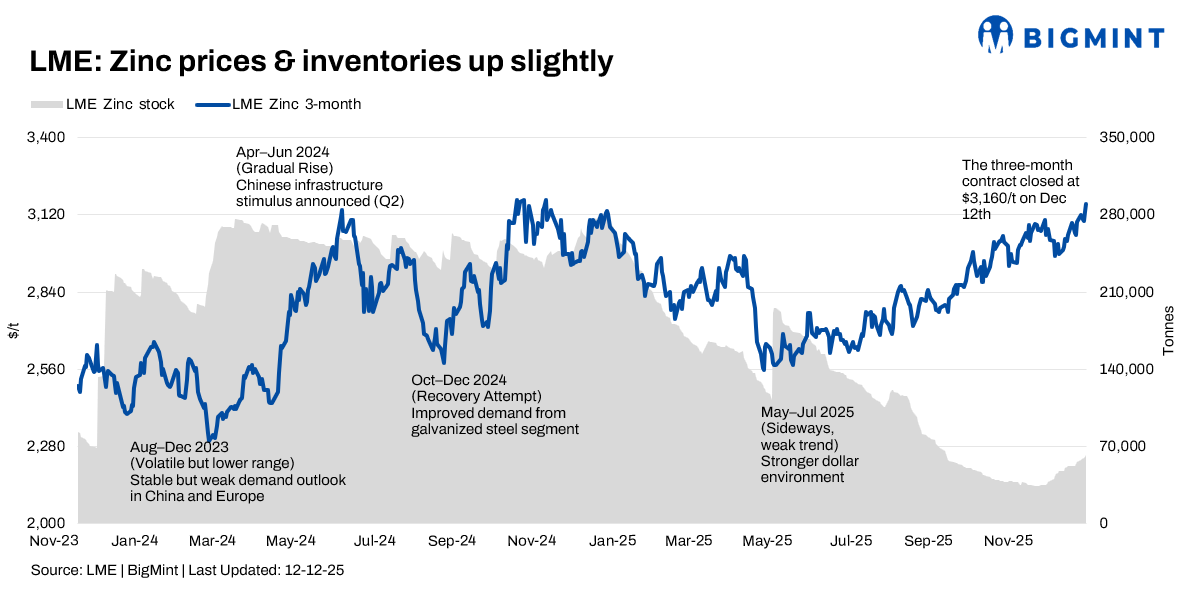

The London Metal Exchange (LME) zinc market entered a mild corrective phase during 8-12 December 2025, easing from early-December highs as profit-taking emerged and a firmer US dollar, alongside broader macro uncertainty, weighed on sentiment. This pullback followed a strong rally in the first week of December. Despite the correction, overall market sentiment remained cautiously constructive, supported by mine maintenance in China, tight ex-China inventories, and firm physical premia. The near-term bias, however, shifted toward consolidation rather than a continuation of the earlier upward momentum.

Price trends

LME zinc cash-settlement prices declined over the week, easing from an early-December high of $3,350.50/t on 2 December to $3,242/t by 12 December, as profit-taking followed the initial rally. In contrast, the LME three-month zinc contract showed relative resilience, rising from around $3,120/t on 8 Dec to $3,160/t by 12 December, indicating underlying support on the forward curve.

Despite the decline in cash prices, zinc remained about 2.7% higher on a one-month basis compared with levels near $3,050/t in mid-November, and roughly 1.4% above year-ago prices of around $3,088/t. This suggests the broader uptrend since November remained intact, with recent weakness largely driven by near-term profit-taking rather than a shift in fundamentals.

Inventory analysis

LME zinc stocks continued to rebuild into mid-December, extending the recovery that began in early November. Inventories rose from 54,325 t on 4 Dec to 60,350 t by 11 December, an increase of 6,025 t or about 11.1% w-o-w. Available exchange stocks during 8-12 December therefore remained in the low- to mid-60,000-t range.

Despite this increase, absolute LME holdings remain historically low and represent less than one day of global refined zinc consumption. As a result, the market continues to view the inventory situation as tight rather than comfortable, limiting downside risk during price corrections.

MCX zinc trends (8-12 Dec)

MCX zinc prices moved higher over the week, outperforming global benchmarks. Near-month contracts, which had recently traded in the INR 313,000-315,000/t range, recorded an approximate 2.9% w-o-w gain. The divergence from LME reflected a combination of currency effects, tighter domestic availability, and steady demand from the galvanising and alloy sectors. Market sentiment on MCX turned cautiously optimistic, supported by firm global spreads and expectations of eventual US rate cuts, despite the broader international consolidation.

SHFE zinc trend

On the Shanghai Futures Exchange (SHFE), the main January 2026 zinc contract traded largely sideways during the week, fluctuating within a narrow CNY 22,400–22,700/t band and posting a net weekly change of less than 1%. SHFE-monitored inventories declined sharply, falling from around 144,200 t on 1 December to approximately 136,000 t by 8 December, a drop of about 5.9% w-o-w. Stocks continued to fall during 8-12 Dec, easing further to roughly 133,000 t, tightening domestic availability.

China fiscal stimulus and demand outlook

China’s proactive fiscal policy measures announced on 12 December added medium-term support to zinc demand expectations. The increase in the fiscal deficit to around 4% of GDP and the issuance of roughly 3 trillion yuan in special bonds are expected to support infrastructure development, urban renewal, and rural projects. Construction, which accounts for roughly 40% of China’s zinc consumption through galvanised steel used in buildings and bridges, is likely to be a key beneficiary.

Additional support is expected from measures aimed at stabilising the property sector and reviving manufacturing activity, including incentives for electric vehicles, appliances, and machinery, all of which are zinc-intensive end-use segments. While these policies did not immediately reverse the early-Dec price correction, they reinforced the medium-term demand outlook and contributed to continued tightness in SHFE inventories.

Outlook

Zinc is expected to consolidate in the near term, with downside supported by tight inventories and supply constraints, while upside may be capped by producer hedging and renewed profit-taking. Incoming macroeconomic data and clarity on the timing of US interest-rate cuts will be key drivers of price direction.

Leave a Reply