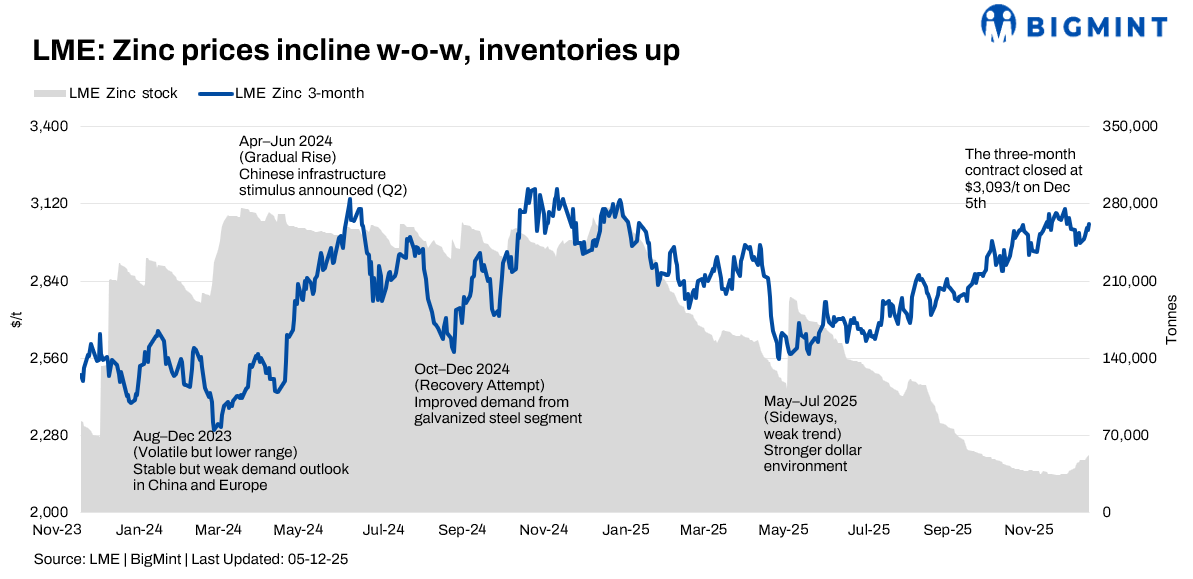

- LME zinc 3‑month prices gain 0.12% w-o-w

- LME stocks continue to build, up 5% w-o-w

The London Metal Exchange (LME) zinc market traded firm to higher over 1-5 December 2025, with prices supported by structurally tight global inventories and fresh supply‑side concerns, even as rising LME stocks and macro uncertainty capped aggressive upside. Sentiment stayed cautiously bullish, with traders watching Chinese mine maintenance, export flows and the pace of inventory rebuild on LME.

Price trends

LME zinc 3‑month prices started the week at about $3,089/t on 1 December and ended near $3,093/t on 5 December, a small but positive weekly change of roughly +0.12%. Over the same period, the LME zinc cash official price rose from $3,315/t on 1 December to $3,222/t on 5 December, meaning that after an early spike to $3,350.50/t on 2 December, cash prices corrected but still finished the week modestly above late‑November levels of $3,255/t on 28 November against $3,222/t, the early‑December average, which implies a near‑flat to slightly negative weekly cash move.

However, zinc prices rose by about 1.5% from late‑October cash levels of around $3,170/t showing that despite intraweek volatility and post‑spike correction, both cash and 3‑month prices remain somewhat firmer on a rolling monthly comparison.

Inventory analysis

LME zinc stocks continued to build but remained low in an absolute sense. Exchange inventories rose from 52,375 t on 1 December to 52,450 t on 2 December and then to 54,325 t by 4 December, compared with 51,750 t on 28 November; this represents a w-o-w increase of 5.0% (from 51,750 t to 54,325 t). Even after this buildup, stocks at 54,325 t were only modestly above 50,000 t compared with 34,000 t at the start of November 2025, underscoring ongoing tightness versus recent 2025 norms. At the same time, SHFE zinc inventories fell 4.4% on the week from 144,000 t (28 Nov) to 137,500 t (4 Dec), keeping the broader global inventory picture tight and helping offset the price-dampening impact of higher LME stocks.

MCX zinc trends (1-5 December)

On India’s Multi Commodity Exchange (MCX), zinc futures extended their prior up‑move, broadly tracking LME. Front‑month contracts traded around INR 308,150/t on 1 December, with reports of prices touching roughly INR 309,000/t on 3 December (about 0.3% gain) on the back of improved spot demand and positive overseas cues. By 5 December, near‑month zinc on MCX was hovering close to INR 310,600/t, around 2.5% higher than levels seen at the end of November, supported by firm LME, tight global stocks and resilient domestic demand from galvanising and alloy segments.

SHFE zinc trend

On the Shanghai Futures Exchange (SHFE), the most‑traded January 2026 zinc contract maintained an upward bias, recording a five‑day winning streak into early December. The contract traded near 22,650 CNY/t at the start of the week and closed around 22,740 CNY/t, a daily gain of about 1% on 2 December, with the weekly move leaving prices at their highest since August. Stronger macro tone, falling SHFE inventories (down 4.42% w-o-w) and expectations of concentrate tightness due to mine maintenance in central and southwest China all contributed to the firmer SHFE structure.

Korea Zinc subsidiary wins climate award

Steel Cycle, a Korea Zinc subsidiary, won the Minister of Climate, Energy and Environment Award on 4 December for its RHF-based waste-processing technology. The company recovers about 50,000 tons of zinc hydroxide annually from steelmaking dust, converting hazardous waste into reusable raw material. The recognition highlights Korea Zinc’s growing leadership in circular-economy practices and low-emission metal recycling.

Outlook

Across LME, MCX and SHFE, zinc is entering December with a cautiously bullish bias- prices are near recent highs, inventories remain thin outside China, and mine shutdowns plus steady refined exports from China keep the supply side tight. However, the sharp percentage rise in LME stocks since early November, along with lingering concerns over Chinese demand and global growth, suggests rallies may be incremental rather than explosive, with dip‑buying likely emerging near technical and cost‑support zones.

Leave a Reply