- Inventory draws signal tightening spot availability

- China smelter margins remain constrained by low TCs

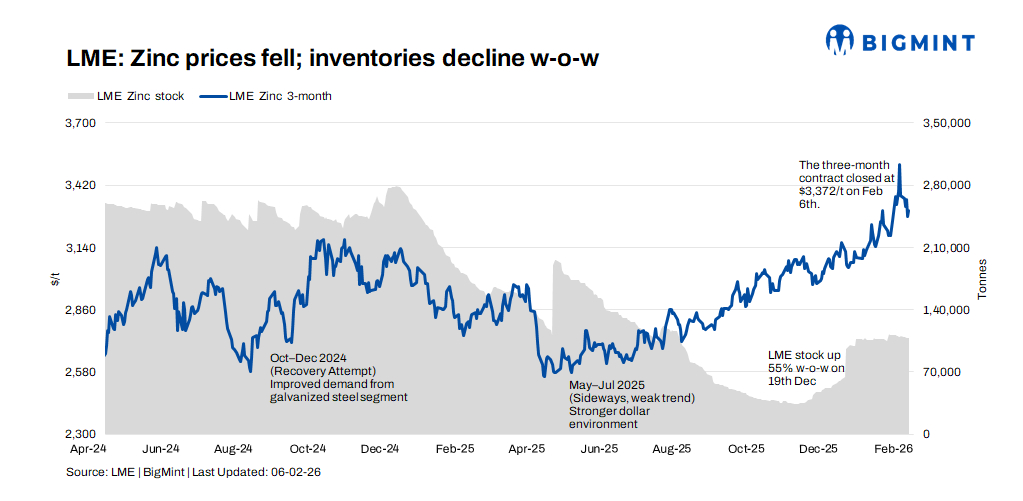

London Metal Exchange (LME) zinc prices fell in the week ended 6 February, pressured by profit-taking and softer macro sentiment, even as underlying fundamentals remained supportive amid ongoing concentrate tightness and steady galvanising demand.

Price trends

LME zinc cash prices opened the week at $3,372/t on 2 February but came under pressure mid-week, sliding to $3,255/t on 5 February before settling at $3,290/t on 6 February, marking a 2.4% w-o-w decline.

The three-month contract followed a similar trajectory, easing from $3,360/t at the start of the week to $3,306.5/t by 6 February, down around 1.6% w-o-w. Prices struggled to sustain levels above the $3,350/t resistance, with downside testing emerging amid broader base metals consolidation.

Inventory analysis

LME zinc inventories continued to trend lower for a fourth consecutive week, declining by around 1.4% w-o-w to 107,600 t as of 6 February, compared with 109,100 t at the start of the week.

While modest inflows were reported earlier in the week, consistent daily withdrawals outweighed arrivals, indicating tightening spot availability. Market participants noted that although visible stocks are thinning, buying interest remains selective at current price levels.

MCX zinc trends (2-6 Feb)

On the MCX, zinc futures displayed heightened volatility but closed the week marginally higher, tracking mixed global cues. The active March 2026 contract traded in a wide range of INR 314,000-333,000/t, reflecting sharp intraday swings.

Prices opened the week at INR 327,000/t on 2 February and settled at INR 328,600/t on 6 February, up around 0.4% w-o-w. Trading volumes peaked early in the week alongside a rise in open interest, suggesting fresh participation, though later sessions saw profit-booking as prices approached the upper end of the range. Domestic supply remained comfortable, with demand largely driven by need-based galvanising consumption.

SHFE zinc trend

The SHFE zinc market weakened during the week, with the active contract declining from RMB 26,187/t on 2 February to RMB 24,704/t on 6 February, marking a 5.7% w-o-w drop.

Prices came under pressure amid softer domestic sentiment and weakness across China’s non-ferrous complex. The decline also reflected cautious downstream buying and constrained smelter margins, as low treatment charges continued to signal underlying concentrate tightness. Despite the pullback, physical premiums remained relatively stable, indicating that near-term supply tightness has yet to fully ease.

Outlook

Zinc prices are expected to remain muted in the near term, with concentrate tightness and declining LME inventories offering underlying support. However, upside momentum may remain capped unless macro sentiment improves or fresh supply-side disruptions emerge. Market participants are likely to stay cautious, focusing on hand-to-mouth purchases amid elevated price volatility.

Leave a Reply