- Lingering concerns over US economic outlook prompt price drop

- SHFE prices remain under pressure despite holiday stockpiling

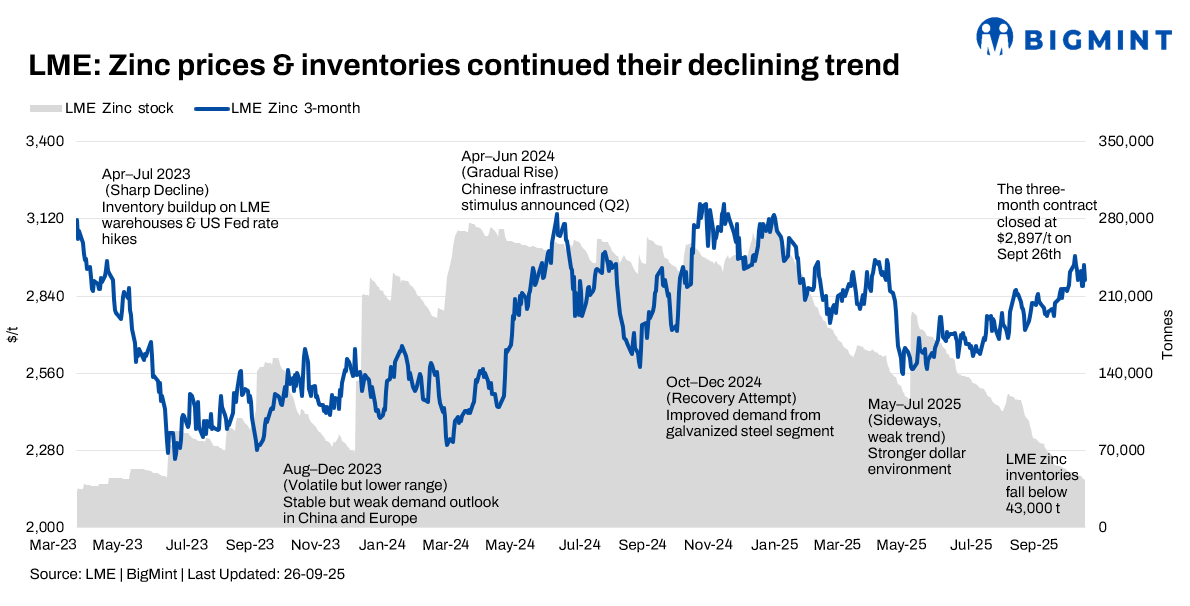

The London Metal Exchange (LME) zinc market trended down during Week 38 (22-26 September 2025), influenced by macroeconomic signals from the US and continued fluctuations in inventory levels. Prices witnessed a largely sideways movement over the five-day period, with a downtrend earlier in the week, which was followed by a brief rebound and a sharp decline again.

Price trends

LME zinc cash-settlement prices trended downward over 22-26 September, falling by around $50/tonne (t). Prices opened at $2,985.00/t on 22 September and fell 2.5% to $2,910.50/t on 23 September. The decline was fuelled by profit-booking and lingering concerns over the US economic outlook, despite earlier signals from the US Federal Reserve suggesting caution regarding aggressive interest rate hikes. Prices rebounded 3.5% later in the week, reaching a high of $3,012.00/t on 25 September before settling lower at $2,935.00/t on 26 September. This fluctuation reflected a mixed market sentiment, with prices hovering at highs despite a hawkish tone from the US Fed.

Inventory analysis

LME zinc inventories continued their declining trend during the week, reaching 42,775 t (down 8.7%) by 26 September from 46,825 tonnes on 22 September. This continued destocking indicates a tightening global supply of readily available zinc and provided a strong impetus for late-week price support.

MCX zinc trends (22-26 September)

MCX zinc mirrored global swings but closed the week with a marginal increase. Prices opened at INR 283,050/t on 22 September and touched a low of INR 276,250/t the same day (-2.4% intraday on 22 September). Prices rebounded to INR 285,050/t on 25 September (+3.2% from the week’s low) before softening slightly to settle at INR 284,150/t on 26 September, ending the week +0.4% higher than the opening level. Tightening LME stocks supported Indian prices, but demand concerns capped gains.

SHFE zinc trend

SHFE zinc prices remained under pressure for most of Week 38, influenced by weak domestic fundamentals and lingering oversupply concerns, which overshadowed supportive factors such as holiday stockpiling. The most-traded SHFE zinc 2511 contract opened at RMB 21,960/t on 22 September and closed at RMB 21,980/t on 26 September, showing an overall relatively flat trend with some intraday volatility. While a pre-holiday restocking demand did lead to a slight decline in domestic inventory, market perception of a continued supply-demand imbalance, combined with fluctuations from Fed-related signals, capped any sustained upward movement and led to a pullback in prices towards the week’s end. The SHFE/LME price ratio also pulled back to around 7.5 and fluctuated, with the zinc ingot import window remaining closed.

Appian secures $150 million financing for Rosh Pinah zinc mine expansion

Appian Capital Advisory has secured a $150 million debt facility from Standard Bank to complete the Rosh Pinah 2.0 zinc mine expansion in Namibia, which is on track for Q3 2026 commissioning. The project, over 80% complete, will nearly double throughput to 1.3 million tonnes (mnt)/year, add new underground deposits and processing facilities, and leverage a solar park supplying 30% of energy, which is set to expand to 16.3 MWp.

Outlook

The near-term zinc market outlook remains uncertain. While declining LME inventories and a softer US dollar could provide some support, persistent oversupply concerns in China and global macroeconomic uncertainties are expected to keep prices volatile. The market will be waiting for a clearer indication of a genuine pick-up in Chinese demand.

Leave a Reply