- LME stocks continue to build to around 99,000 t

- MCX zinc retains mild upward trend

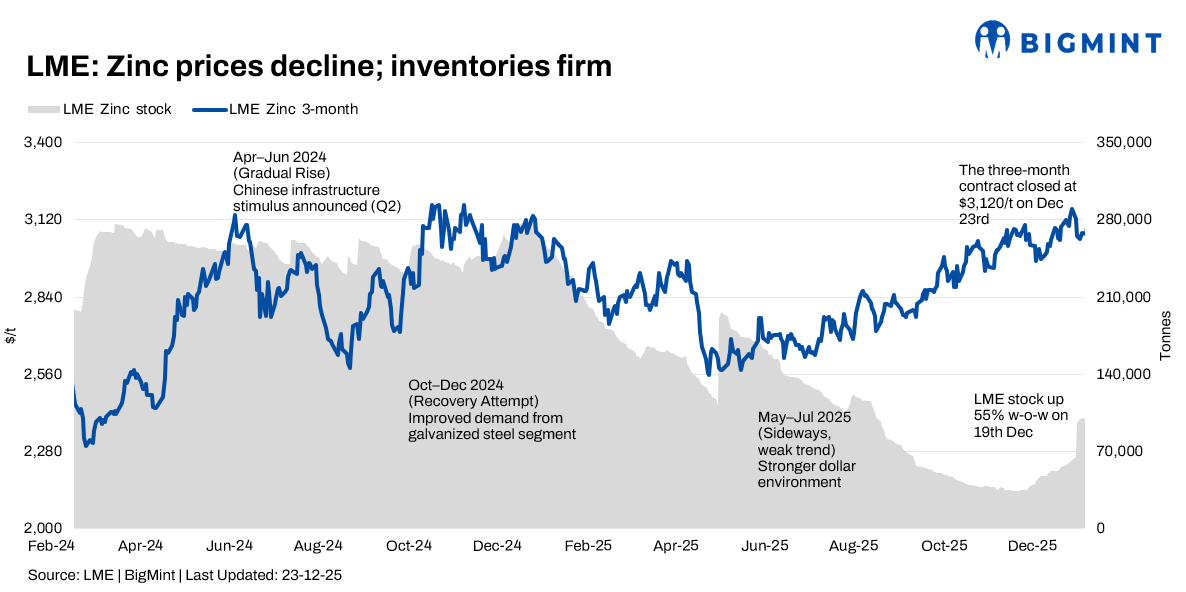

The global zinc market entered a low-liquidity consolidation phase during 22-26 December, as holiday closures-most notably the LME shutdown on 25 December-curtailed trading activity. Prices eased marginally after strong gains in November and early December, but the broader bullish bias remained intact, supported by tight global availability outside China and firm physical market signals.

Price trends

LME zinc prices traded in a narrow range through the week. CFD benchmarks placed zinc at around $3,091/t on 24 December, down 0.3% d-o-d, but still up 2.9% m-o-m and 1.6% y-o-y. By 26 December, LME/SHFE spot-equivalent prices clustered around $2,906-2,919/t, reflecting a mild pullback from the mid-December intra-month peak of $3,200-3,220/t.

The week’s subdued price action largely reflected thin liquidity, light profit-taking following the November rally, and a firmer US dollar. Importantly, prices remain well above early-November levels, indicating that the recent softness is corrective rather than trend-reversing.

Inventory analysis

LME zinc inventories continued to gradually rebuild into late December, with stocks holding just below 100,000 t. Warehouse inventories stood at 99,250 t on 22 December, easing marginally to 98,975 t on 23 December. While stocks have risen sharply from early-November lows of around 35,900 t-an increase of nearly 80%-absolute inventory levels remain historically tight, limiting downside risks.

MCX zinc trends (22-26 December)

In India, MCX zinc futures mirrored the calm global tone but retained a mild upward bias. The 31 December contract settled at INR 302,750/t on 22 December, rising to INR 311,650/t by 26 December, marking a w-o-w gain of around 3%. Intraday prices largely remained within the INR 303,000-312,000/t range.

Trading volumes were subdued due to the holiday period, with open interest declining. However, m-o-m, MCX zinc prices remained modestly positive, supported by higher international benchmarks, tight global supply conditions, and steady demand from the galvanising and alloy-consuming sectors.

SHFE zinc

On the Shanghai Futures Exchange, zinc remained firmer than the LME. The most-traded February 2026 contract traded around RMB 23,000-23,100/t, supported by declining domestic inventories and falling treatment charges amid tight concentrate supply.

Smelter production cuts and low on-hand stocks helped offset weaker global macro sentiment. The SHFE/LME ratio rebounded, narrowing import losses and effectively closing the export arbitrage window, implying reduced refined zinc exports from China in December compared with earlier months.

Outlook

Zinc prices are expected to remain range-bound in the near term due to year-end liquidity constraints and economic uncertainty. However, tight inventories, firm physical premia, and constrained concentrate supply continue to provide a supportive floor. Market focus will shift in early January toward Chinese restocking trends, treatment charge movements, and the pace of LME inventory rebuilds.

Leave a Reply