- Macro optimism, softer US dollar lend support to zinc prices

- Indian futures track global gains but face muted consumption

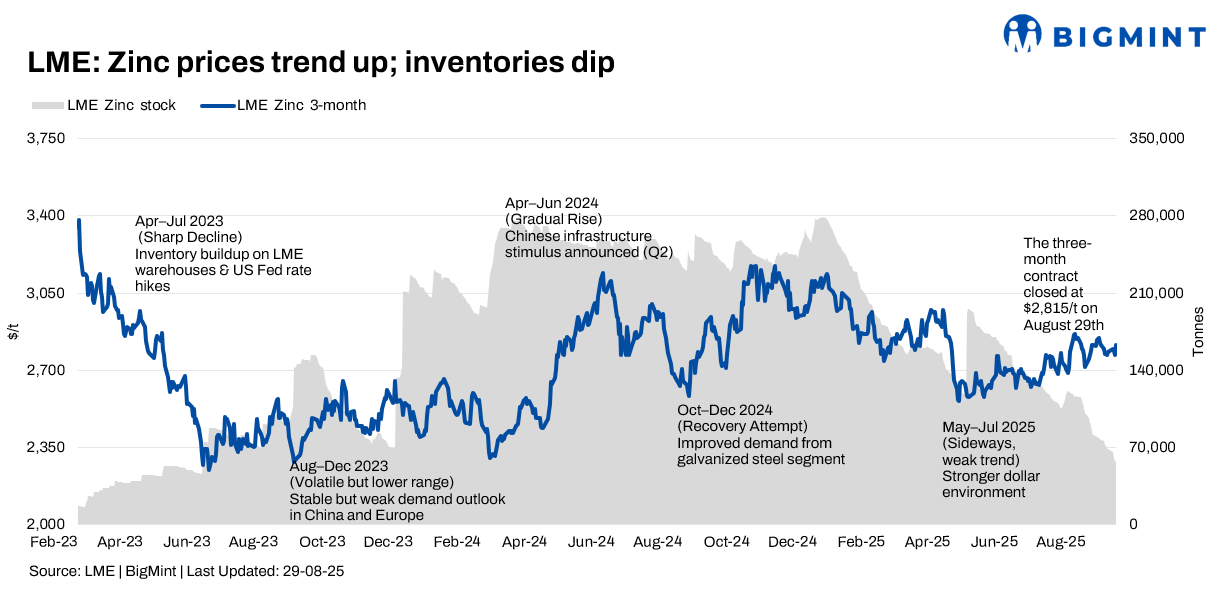

The London Metal Exchange (LME) zinc market experienced upward momentum during Week 35 (25-29 August 2025), largely supported by continued destocking of LME inventories, positive macroeconomic signals, and a softer US dollar. With the recovery in prices, market sentiment turned cautiously optimistic despite persistent oversupply concerns in China.

Price trends

LME zinc cash-settlement prices trended upward during the week, showing a recovery from the previous period’s downturn. Prices opened at $2,789/t on 26 August and closed higher at $2,815.50/t on 29 August. The three-month LME Zinc contract mirrored this pattern, closing at $2,815/t on 29 August against $2,794.50/t on 26 August.

Inventories

LME zinc inventories continued their sharp decline during the week, falling from 65,525 t on 26 August to 56,500 t on 29 August. This continuous destocking indicates a tightening global supply of readily available zinc and provided strong support for prices. However, this trend contrasted with the situation in China, where domestic inventories continued to increase, to 144,500 t across seven locations by 28 August. This divergence suggests persistent oversupply concerns within the domestic Chinese market, where weak demand continues to impact inventory levels.

Structural factors behind inventory drawdowns

Despite the sharp fall, analysts caution that LME warehouse levels are not always a reliable proxy for true global availability. Much of the remaining inventory is concentrated in Singapore, where zinc has repeatedly moved in and out of sheds as part of warehouse arbitrage cycles rather than reflecting underlying demand. In fact, Singapore’s zinc exports surged to 153,000 t in the first half of 2025, filling regional supply-chain gaps left by smelter disruptions in Japan, South Korea, and Australia. At the same time, China has ramped up production, with refined zinc output rising 4% y-o-y in January-July and expected to accelerate further in August, supported by improving concentrate supply from new mines in the DRC and Russia. This uneven landscape explains why LME spreads remain in mild contango despite depleted stocks, suggesting the broader market is not yet convinced of a genuine squeeze.

MCX zinc trends (25-29 August)

MCX zinc prices experienced a positive w-o-w performance, aligning with the recovery in global markets. The futures contract, which closed at INR 265,650/t on 25 August, rose to INR 267,250/t on 29 August. This upward trend in the Indian market was supported by improved global macroeconomic sentiment following Fed Chair Jerome Powell’s measured Jackson Hole speech, which eased concerns about aggressive rate hikes. Additionally, tightening LME inventories provided further support. However, domestic factors and underlying demand concerns continued to influence trading activity, tempering the gains.

Zinc producers – key updates

Among key producers, Hindustan Zinc Limited reported a strong performance, with a 47 percent y-o-y profit surge in Q4FY’25. It awarded an EPC contract to L&T for its Debari smelter upgrade. The company also signed an MoU with Epiroc to deploy advanced digital safety technology in its underground mines and is evaluating uranium mining opportunities, contingent on policy approval for private sector participation.

Vedanta Limited, meanwhile, posted an 11.7 percent y-o-y decline in net profit for Q1FY’26 and continues to face scrutiny over governance practices at Hindustan Zinc.

On the international front, Hudbay Minerals announced on 27 August that it has resumed operations at Snow Lake in Manitoba after a mandatory evacuation order was lifted.

On the same day, Ivanhoe Mines announced the completion of its debottlenecking programme at the Kipushi Zinc Mine in the Democratic Republic of Congo, which was finished ahead of schedule and under budget.

Outlook

The near-term zinc outlook remains cautious. While falling LME inventories and easing macroeconomic concerns are lending support, persistent oversupply concerns in China and weak domestic demand are expected to keep prices volatile. Market participants will closely track Chinese demand trends, supply-chain flows from Singapore, and broader global economic signals for further direction.

Leave a Reply