- MCX zinc prices rise by 1.43% w-o-w

- SHFE zinc prices follow bullish trend

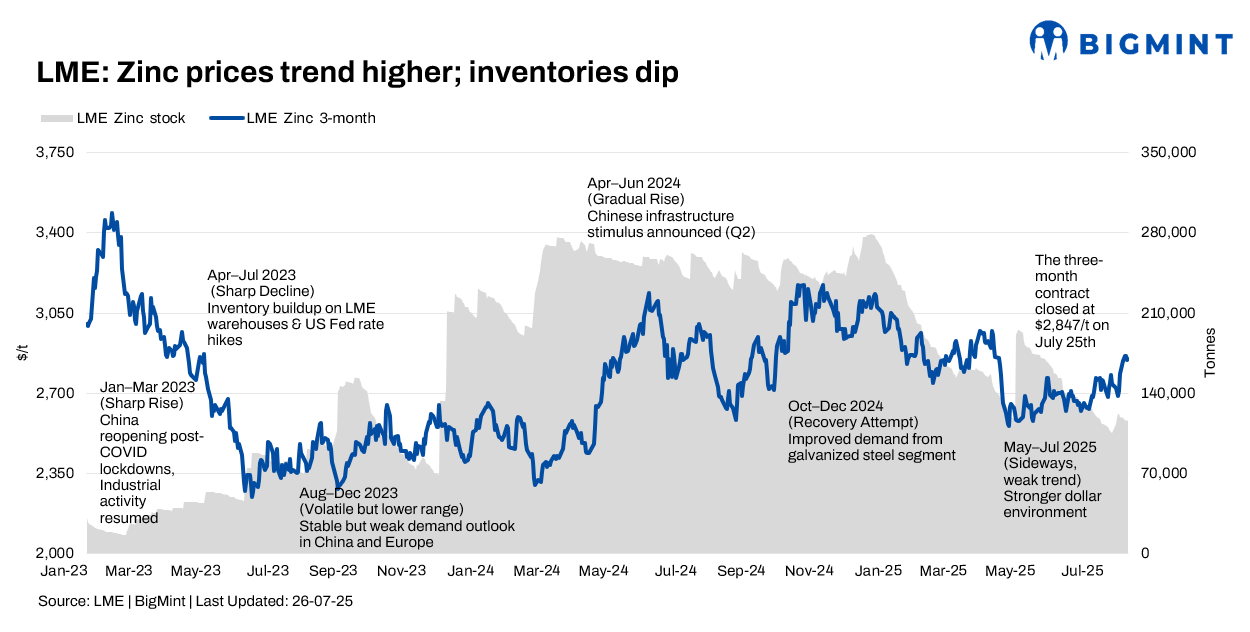

London Metal Exchange (LME) zinc prices closed slightly higher w-o-w during Week 30 (21-25 July 2025), driven by expectations of Chinese stimulus support and declining stocks, which limited supply. However, over the week, LME prices experienced volatility due to changing macroeconomic sentiment, inventory shifts, and regional demand dynamics.

Prices trend higher; inventories dip

LME zinc cash-settlement prices edged higher w-o-w, and the three-month contract closed at $2,847/t on 25 July, rising by $65/t as against $2,782/t on 18 July.

Prices, which closed at $2,780.50/tonne (t) on 18 July, initially saw continued upward momentum on 21 July, closing at $2,844.50/t. However, there was a slight drop during the week to $2,854.00/t on 24 July, suggesting a period of consolidation following the previous week’s rally.

Zinc prices were influenced by renewed optimism regarding potential stimulus measures, but also faced pressure from profit booking and concerns about ongoing US trade negotiations.

LME zinc stocks decreased during the week, to 115,775 t on 25 July from 118,225 t on 21 July. This decline in LME inventory, particularly the rise in cancelled warrants (59,900 t on 21 July), reduced the amount of readily available metal, contributed to a tightening supply outlook.

MCX zinc rises (21-25 July)

MCX zinc prices climbed up by 1.43% to settle at INR 269,050/t on 25 July from INR 265,250/t on 21 July, driven by optimism over potential stimulus measures.

Prices fluctuated during the week, with a low of INR 266,050/t and a high of INR 270,600/t on 24 July.

By 25 July, MCX zinc faced resistance near INR 270,000/t levels, showing signs of potential downside amid rising volatility.

Macroeconomic drivers

- Macroeconomic factors played a significant role. A weaker US dollar in the first half of July generally supported base metal prices, including zinc.

- China’s Q2CY’25 GDP growth exceeded expectations, but concerns about the second half’s momentum remained due to potential softening exports and patchy domestic demand.

- SHFE zinc prices followed a bullish trend in Week 30, with the most-active September 2025 contract opening at around RMB 22,895/t ($3,188/t) on 21 July. Prices climbed up steadily, reaching a high of approximately RMB 22,995/t by mid-week. The contract closed at RMB 22,945/t on 25 July, reflecting a w-o-w gain, driven by falling SHFE warehouse inventories and optimism over potential policy support in China.

- The SHFE/LME zinc price ratio fluctuated this week, oscillating at around 8.1. This level is critical as it indicates the closed status of the import window for Chinese zinc ingots.

- Investor sentiment remained bearish due to growing oversupply and weak consumption trends. The International Lead and Zinc Study Group (ILZSG) forecasts a global surplus of 93,000 t for 2025. This surplus is attributed to a projected 4.3% rise in mine output (to approximately 12.43 million tonnes) and a 1.8% increase in refined production (to approx. 13.73 million tonnes), while global demand is expected to rise a more modest 1.0%, mainly driven by galvanised steel demand.

Outlook

The LME zinc market in Week 30 witnessed a complex interplay of factors. While LME prices experienced upward momentum, fuelled by macroeconomic optimism and tightening LME inventories, the strength of the rally was tested by weak end-use demand in China and rising domestic inventories. Increasing treatment charges (TCs) for imported zinc ore reflect global supply constraints and will be a factor for Indian smelters. The outlook remains cautious, with ongoing macroeconomic uncertainty and demand dynamics influencing price direction.

Leave a Reply