- LME stocks rise early in the week before easing; market stabilises after recent correction

- MCX zinc trades rangebound; SHFE prices recover slightly toward week-end

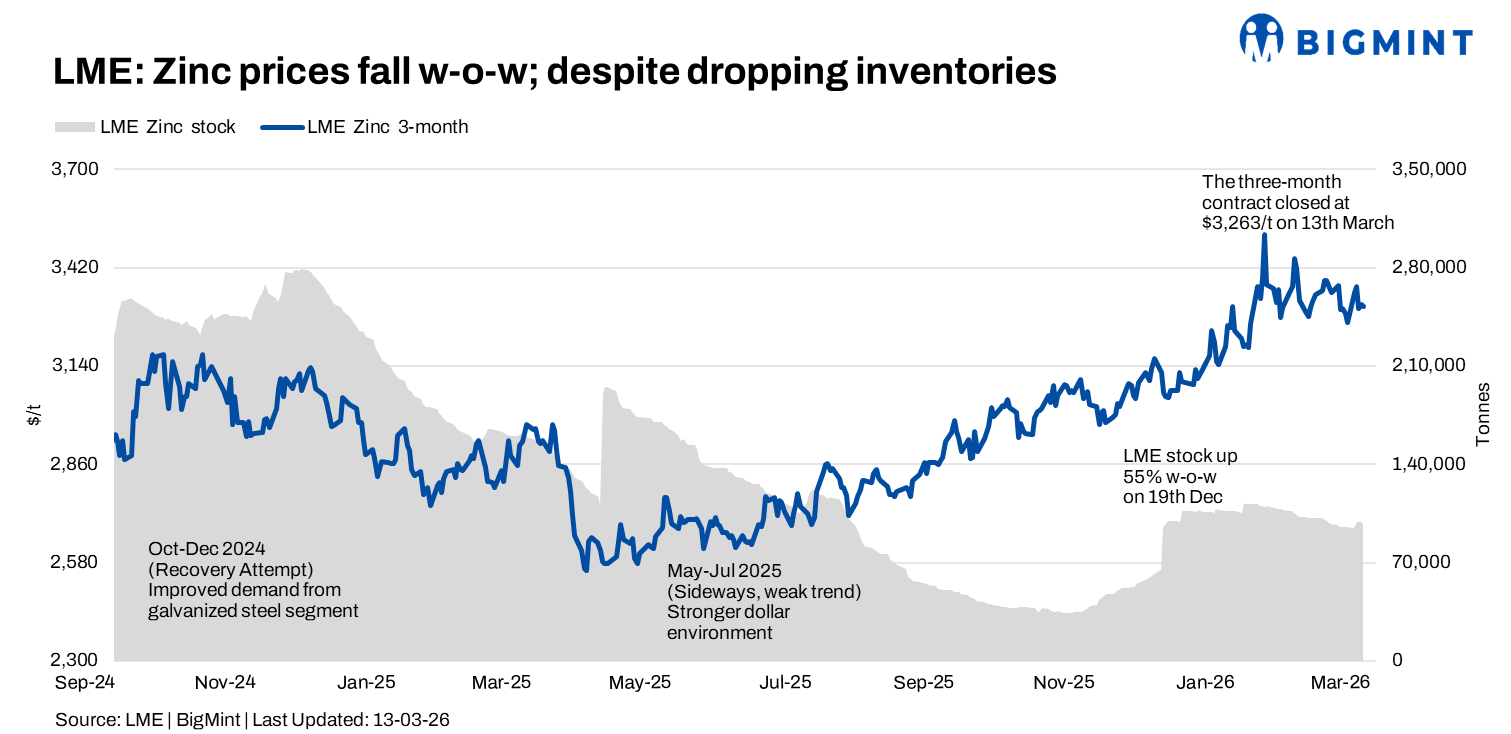

London Metal Exchange (LME) zinc prices moved lower in the week ended 13 March, easing from early-week levels as the market consolidated following recent volatility. While prices remained near the $3,300/t range, fluctuations in exchange inventories and cautious buying activity kept upside momentum limited.

Price trends

Zinc cash prices on the London Metal Exchange opened at $3,320/t on 9 March and moved higher in the early sessions before weakening mid-week. Prices touched a low of $3,264/t on 12 March before recovering slightly to $3,270/t by 13 March.

On a w-o-w basis, cash prices declined by around 1%, compared with $3,304/t on 6 March, reflecting mild consolidation after the previous week’s pullback.

The three-month contract followed a similar trajectory. Prices opened at $3,348/t on Monday, rose briefly to $3,366/t on Tuesday, and then softened to $3,309/t by Friday. Compared with $3,263/t in the previous week, the contract posted a marginal w-o-w increase of around 1.5%, indicating partial recovery in forward prices.

Overall, the market traded within a relatively narrow band as participants adopted a cautious stance following recent volatility across the base metals complex.

Inventory analysis

LME zinc inventories showed mixed movements during the week, initially rising before declining toward the end of the period.

Stocks increased from 94,975 t on 6 March to 98,950 t on 10 March, reflecting fresh arrivals into exchange warehouses. However, inventories gradually declined in the subsequent sessions, falling to 97,900 t by 13 March.

On a w-o-w basis, visible stocks rose by roughly 3%, although the late-week drawdown suggests continued physical offtake from warehouses.

Despite the temporary rise in inventories earlier in the week, overall stock levels remain relatively low compared with historical averages, indicating that underlying supply conditions remain moderately tight.

MCX zinc trends (9-13 Mar)

On the Multi Commodity Exchange of India (MCX), zinc futures traded within a narrow range during the week, broadly tracking global cues.

The active April 2026 contract traded between INR 325,250/t and INR 329,850/t during the period. Prices opened at INR 326,050/t on 9 March and settled slightly higher at INR 327,250/t on 13 March, marking a modest w-o-w gain of around 0.4%.

Trading volumes increased toward the latter part of the week, while open interest rose from 765 lots at the start of the week to 1,516 lots, indicating fresh participation and positioning in the futures market.

Domestic demand from the galvanising sector remained steady, although most buyers continued to procure material on a need-based basis.

SHFE zinc trend

On the Shanghai Futures Exchange (SHFE), zinc prices initially declined before recovering gradually during the week.

SHFE zinc was assessed at around $3,536/t on 9 March, falling to $3,468/t on 10 March amid early-week selling pressure. Prices then stabilised and edged higher to $3,493/t by 13 March.

The movement broadly mirrored global trends, with Chinese market participants remaining active but cautious amid fluctuating sentiment across base metals.

Outlook

In the near term, zinc prices are expected to remain within the $3,250-3,300/t range. Short-term support may come from relatively low exchange inventories and stable physical demand. However, intermittent inventory inflows and cautious buying interest could limit strong upward momentum.

If inventories resume a consistent downward trend toward the 95,000 t level or lower, prices may attempt another move toward the $3,350-3,400/t range. Conversely, if stock levels stabilise and broader base metals sentiment weakens, zinc could test the $3,200-3,250/t support zone.

Leave a Reply