- LME stocks jump early in the week, pressuring prices; slight late-week drawdown offers limited support

- MCX zinc tracks global weakness; SHFE prices trend lower through the week

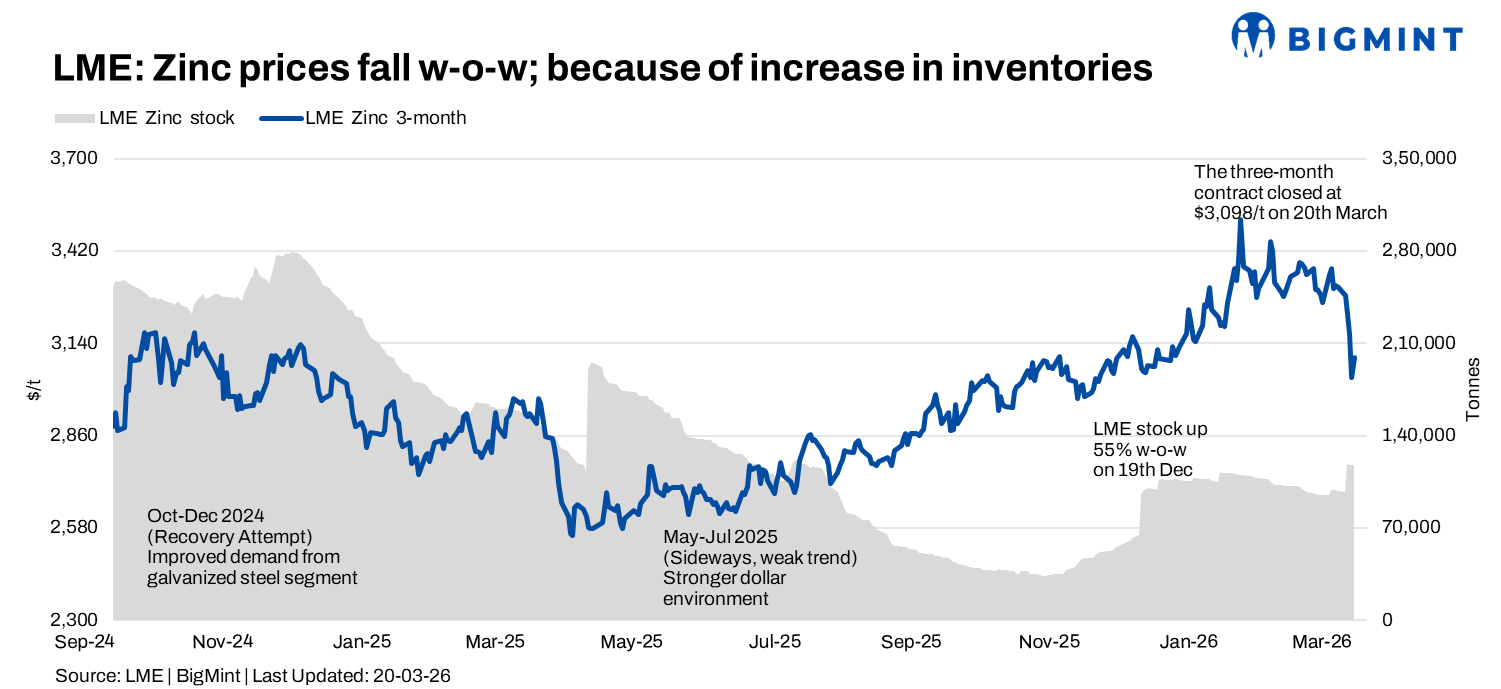

London Metal Exchange (LME) zinc prices declined sharply in the week ended 20 March, weighed down by a significant build-up in exchange inventories and cautious market sentiment. Prices corrected throughout the week, briefly slipping below the $3,100/t mark, as rising stocks and weak buying interest pressured the market.

Price trends

Zinc cash prices on the LME opened at $3,240/t on 16 March and trended lower across the week amid persistent selling pressure. Prices fell to a weekly low of $3,010/t on 19 March before recovering slightly to close at $3,065.5/t on 20 March. On a w-o-w basis, cash prices declined by around 6%, compared with $3,270/t on 13 March, marking a clear shift from the previous week’s consolidation phase to a more pronounced correction.

The three-month contract followed a similar trajectory. Prices opened at $3,285/t on Monday and declined steadily to $3,037/t mid-week, before settling at $3,098/t by Friday. The contract registered a w-o-w decline of approximately 6%, reflecting broad-based weakness across the forward curve. Overall, the market remained under pressure, with limited buying support as participants adopted a cautious stance amid rising inventories and softer global cues.

Inventory analysis

LME zinc inventories recorded a sharp increase during the week, emerging as the primary factor influencing price direction. Stocks rose significantly from 97,500 t on 16 March to 118,375 t on 17 March, indicating a substantial inflow into exchange warehouses. Inventories remained elevated in the following sessions, easing marginally to 117,675 t by 20 March.

On a w-o-w basis, stocks increased by over 20%, marking a notable shift in visible supply conditions. Although a slight drawdown was observed toward the end of the week, overall inventory levels remained high, limiting any meaningful price recovery. The sharp build in stocks suggests improved near-term availability in the exchange system, which weighed heavily on market sentiment and contributed to the downward pressure on prices.

MCX zinc trends (16-20 March)

On the Multi Commodity Exchange (MCX), zinc futures mirrored the global downtrend, with prices declining steadily throughout the week. The active April 2026 contract opened at INR 326,050/t on 16 March and fell consistently to close at INR 307,200/t on 20 March, registering a w-o-w decline of nearly 6%.

The contract traded within a range of INR 305,350/t to INR 326,950/t during the week. Market activity picked up in the mid-week sessions, with open interest rising from 1,635 lots at the start of the week to a peak above 2,200 lots, before easing slightly to 2,018 lots by Friday, indicating initial fresh positioning followed by some profit booking.

Domestic demand from the galvanising sector remained steady, though buying activity was largely need-based amid falling prices.

SHFE zinc trend

On the Shanghai Futures Exchange (SHFE), zinc prices also trended lower during the week, reflecting weak sentiment across the global base metals complex. SHFE zinc declined from around $3,482/t on 16 March to $3,428/t by 19 March, indicating a gradual but consistent downtrend. The movement aligned with LME trends, with Chinese market participants remaining cautious amid declining prices and uncertain demand conditions.

Outlook

In the near term, zinc prices are expected to remain under pressure, with the recent sharp increase in LME inventories likely to cap any strong upward movement. If stock levels remain elevated or see further inflows, prices may test the $3,000-3,050/t support range. On the upside, any recovery could face resistance around $3,150-3,200/t.

Leave a Reply