- Benchmark TC/RCs may turn negative in 2026, 1st time in history

- Copper may see 150,000-t deficit in 2026, conc tightness deepens

At this year’s LME Week 2025 in London, copper dominated discussions, reflecting the metal’s critical role in global electrification and infrastructure demand. The event, held over 13-18 October, drew miners, traders, and smelters from across the world, all focusing on a market that remains tight but uncertain.

They saw intense debate around the future of copper pricing, smelter margins, tightening supply, and the viability of traditional concentrate benchmarks. Traders, miners, and smelters agreed that the market is heading toward a deep structural shift, with treatment and refining charges (TC/RCs) plunging to levels that threaten smelter profitability worldwide.

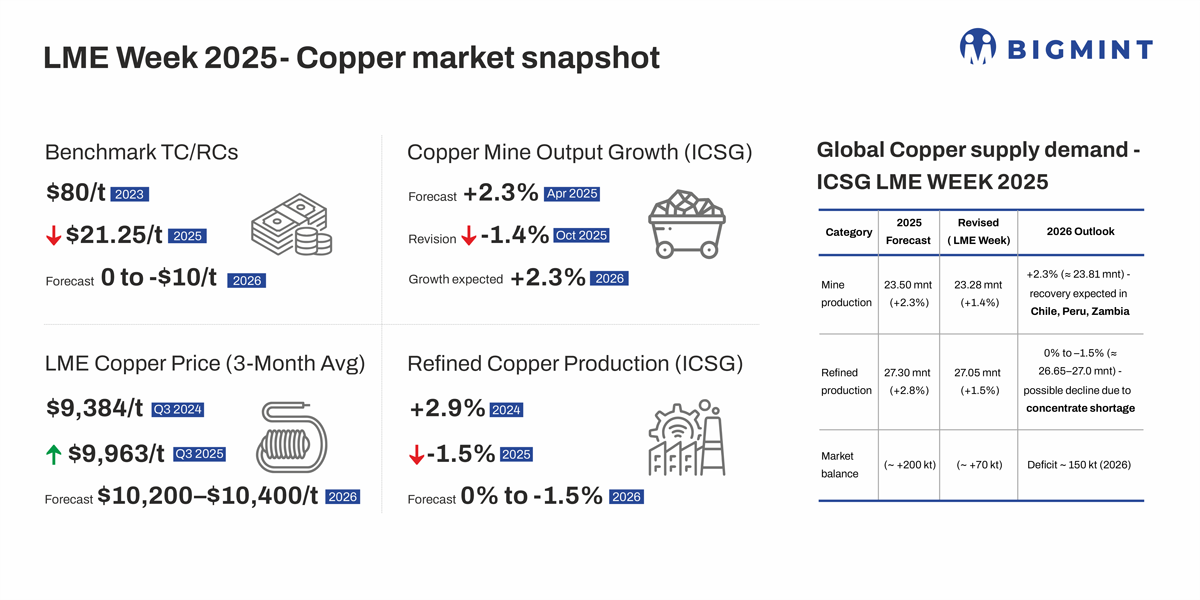

Notably, market participants agreed that the copper concentrate market remains extremely tight, with benchmark TC/RCs collapsing from around $80/tonne (t) in 2023 to $21.25/t in 2025. Several traders and smelter executives warned that 2026 contracts could approach zero or even negative levels, highlighting deep supply stress. The global copper balance is expected to swing into a deficit of around 150,000 tonnes in 2026, as smelters face reduced feed availability despite an expected mine recovery in Chile, Peru, and Zambia.

Highlights

Falling TC/RCs strain smelters’ profitability

Copper’s benchmark concentrate contract — the annual TC/RC set by major Chinese smelters and Chile’s Codelco – has come under growing strain as spot charges collapse. Spot TC/RCs in Asia have dropped to around $25-30/t and 2.5-3¢/lb, compared to the 2024 benchmark of $80/t and 8¢/lb. The steep decline signals severe tightness in mine supply and growing imbalance between miners and refiners.

Executives from major smelting companies, including JX Nippon, Mitsubishi Materials, and Aurubis, said during the conference that such low charges are unsustainable. Several smelters in China and Southeast Asia are reportedly planning production cuts or maintenance downtime to cope with narrowing margins. “It’s becoming a survival game for many smelters,” one Japanese trader said.

Mine disruptions squeeze global supply

The tightness originates from multiple mine disruptions across key producing nations. Freeport-McMoRan’s Grasberg mine in Indonesia, Codelco’s El Teniente and Chuquicamata in Chile, and First Quantum’s Panama mine closure have collectively removed over 500,000 t of copper concentrate from global supply since late 2024. The International Copper Study Group (ICSG) now projects mine output growth at just 1.4% for 2025, sharply lower than the 3% forecast earlier this year.

Meanwhile, global refined copper demand is expected to grow by 3.5-4% in 2025, driven by the energy transition, EV production, and grid expansion. This will likely result in a 200,000-250,000 t refined copper deficit, extending tight market conditions through CY’26.

Copper prices show bullish momentum

Copper prices remained buoyant through LME Week. The LME 3-month contract hovered near $9,950/t, up about 6% y-o-y, supported by speculative interest and supply concerns. Some participants believe the price could test $10,500/t in early 2026 if no major mine restarts occur.

Beyond price and supply, a key topic of discussion was whether the benchmark system itself will survive. Several delegates argued that the traditional annual benchmark may lose relevance, as spot and regional contracts increasingly dominate trading. Large smelters in China, India, and Europe are pushing for more flexible, short-term arrangements that reflect real-time market dynamics instead of a single global benchmark negotiated once a year.

A senior representative from a Chilean miner commented, “The market is fragmenting – there is no longer one uniform benchmark, and regional differentiation is the new reality.” This sentiment was echoed by European traders, who highlighted the divergence between Chinese spot TC/RCs ($25/t) and European terms (around $35-40/t).

Geopolitical and trade issues also coloured the discussion. The US 50% tariff on Chinese metal products and ongoing logistical challenges have altered trade flows, while energy costs in Europe continue to pressure smelter margins. Some analysts warned that if TC/RCs stay at current lows into 2026, at least 10-15% of global smelting capacity could face temporary shutdowns or consolidation.

Participants remain bullish on market

Despite short-term strain, many delegates were optimistic about copper’s long-term fundamentals. Demand from renewables, EVs, and power infrastructure is expected to lift annual copper consumption to around 30 million tonnes (mnt) by 2030, up from 25 mnt in 2024. The supply gap is widening, but new projects such as Kamoa-Kakula Phase 3 (DRC) and QB2 in Chile may offer partial relief from 2026 onward.

In summary, LME Week 2025 highlighted a copper market caught between surging demand and constrained mine output. With TC/RCs near record lows, smelters face one of the toughest years in a decade, while miners hold a stronger hand in negotiations. The industry’s long-standing benchmark system may be fading, replaced by a more fragmented, real-time pricing structure – a sign of how rapidly copper’s world is changing.

Leave a Reply