- LME tin inventories rise sharply w-o-w

- High prices dampen downstream buying interest

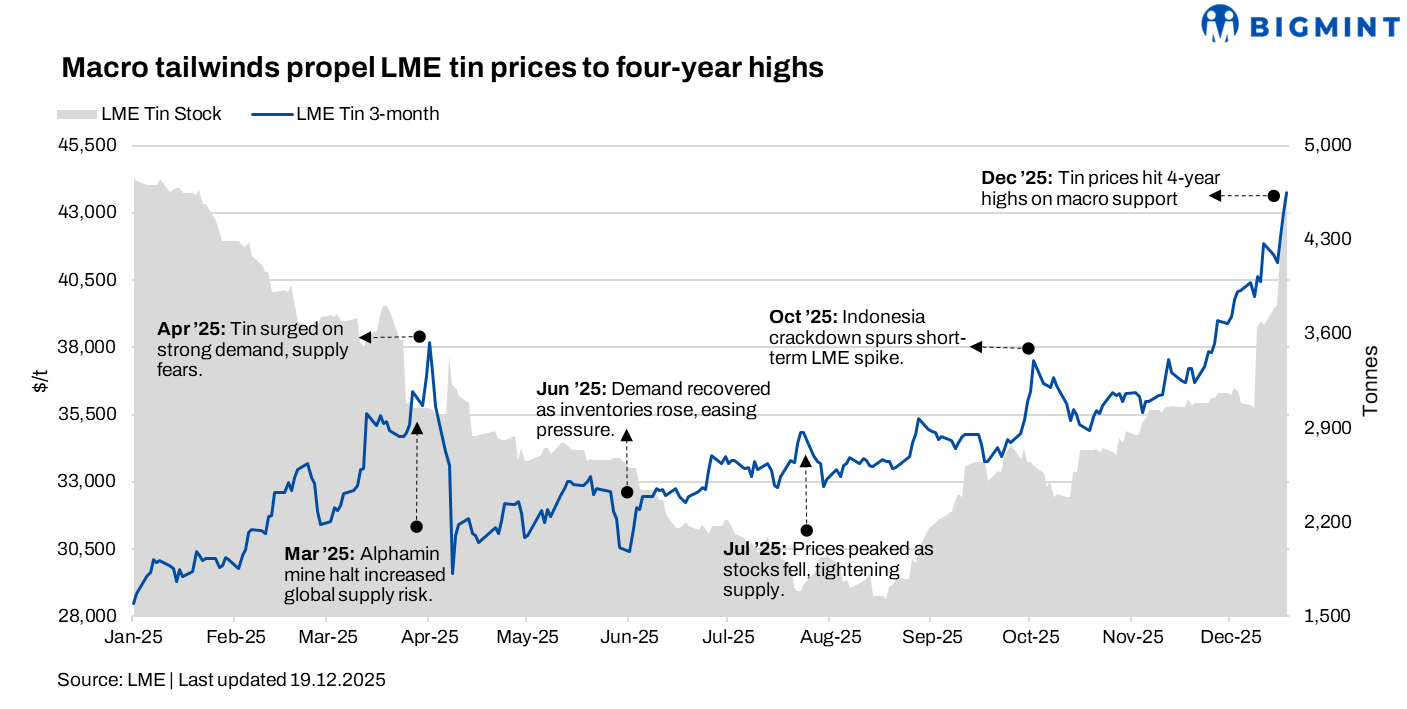

Tin prices on the London Metal Exchange (LME) surged to a four-year high level in the week ended 19 December (week 51) as weaker-than-expected US inflation fuelled expectations of Fed rate cuts, pressured the US dollar, and drove fund inflows into commodities despite weak downstream demand.

Pricing, inventory trends

LME tin prices averaged $42,295/tonne (t) in the week ended 19 December, marking an $1,643/t or 4% rise w-o-w from the previous week. The week began with prices at $41,450/t, which inched up to around $42,125/t mid-week and then closed higher at $43,750/t.

Meanwhile, tin inventories at LME-registered warehouses rose 22% to 4,174t from 3,429 t in the previous week.

What impacted prices?

LME tin prices rose mainly due to supportive macro factors outweighing near-term fundamental pressures. The softer-than-expected US November CPI strengthened market expectations for Fed rate cuts, weakening the US dollar and encouraging capital inflows into commodities, which provided a strong financial boost to tin prices. At the same time, expectations of relatively stable smelter output in December limited immediate supply-side downside, reinforcing bullish sentiment. However, the price increase was largely driven by macro liquidity and sentiment rather than demand fundamentals, as high prices suppressed downstream buying and spot market activity remained sluggish, increasing volatility at elevated price levels.

Outlook

In the short term, LME tin prices are likely to remain volatile at elevated levels. While macro sentiment and fund inflows may continue to offer support, rising exchange inventories, rebounding Indonesian exports, and subdued downstream demand could cap further upside and increase the risk of price corrections.

Leave a Reply