- Supply disruption fuels speculation

- Inventories edge down w-o-w

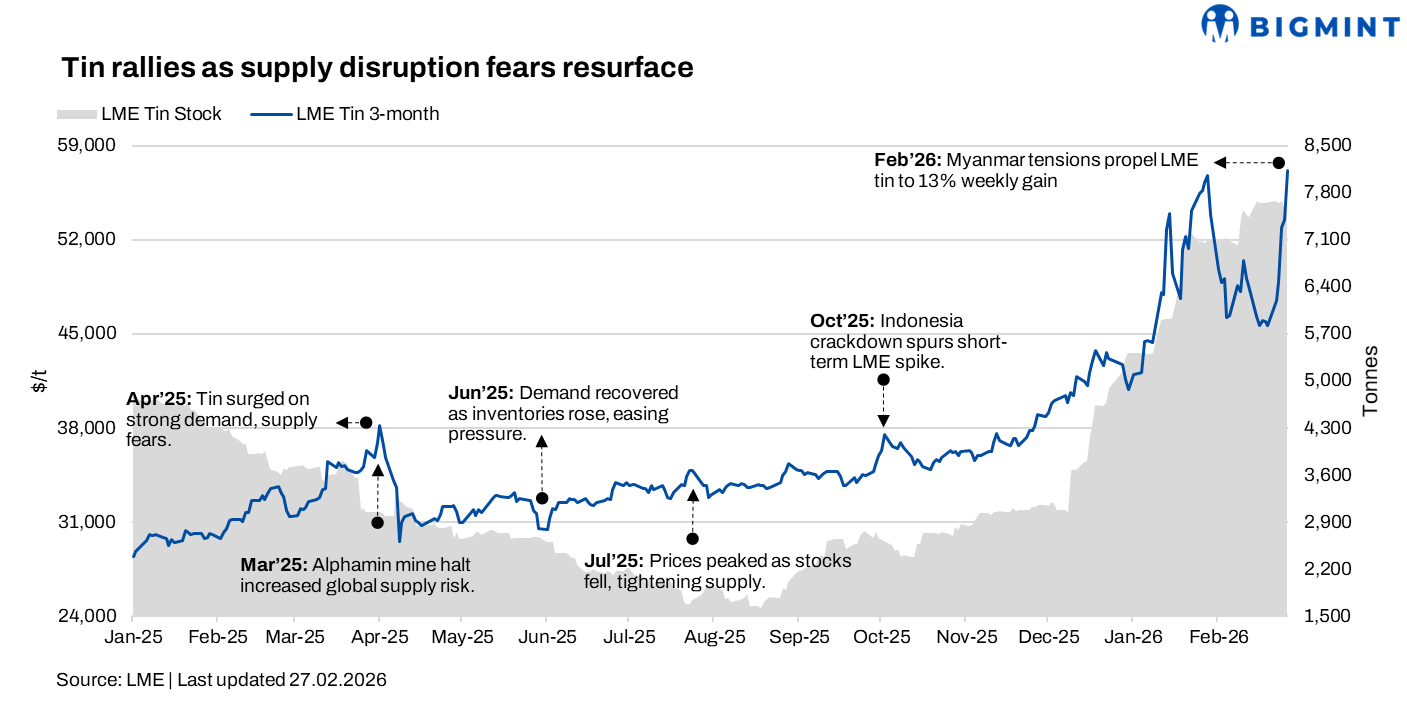

Tin prices on the London Metal Exchange (LME) gained 13% in the week ended 27 February 2026. LME tin prices climbed sharply w-o-w, driven by renewed Myanmar supply concerns, earlier Indonesian export constraints, and speculative fund activity, even as physical demand recovery and spot market participation remained relatively subdued.

Pricing, inventory trends

LME tin prices averaged $51,994/tonne (t) in the week ended 27 February, marking an $6,098/t or 13% rise w-o-w from the previous week. The week began with prices at $47,475/t, which inched up to around $52,920/t mid-week and then closed at $57,175/t.

Meanwhile, tin inventories at LME-registered warehouses fell marginally to 7,627 t from 7,657 t in the previous week.

Factors impacting prices

LME tin prices moved higher w-o-w, supported primarily by renewed market concerns over potential disruptions to Myanmar’s tin ore supply. Speculative interest intensified after news of conflict developments in Myanmar, prompting funds to push the three-month contract higher. Although the actual conflict area remains far from the main tin-producing Wa region and the direct short-term impact on supply appears limited, the headlines were sufficient to reignite risk premiums in the market and drive futures prices upward.

On the overseas supply side, earlier constraints stemming from Indonesia’s January RKAB quota approvals had sharply reduced exports, tightening near-term availability. While exports have since shown signs of recovery in February, the previous decline — particularly the significant m-o-m drop — continued to lend support to prices by reinforcing perceptions of supply-side vulnerability. At the same time, strong exports to China highlighted steady regional demand flows, further underpinning market sentiment.

Domestically, elevated prices have tempered spot market activity, as downstream enterprises have been slow to fully resume operations following the holiday period. Tin prices rising above the RMB 430,000/t level suppressed immediate restocking interest, with many consumers opting to digest existing inventories. Despite relatively slow physical circulation and limited visible destocking, macro sentiment and event-driven trading dominated price direction, encouraging active fund participation and keeping prices elevated.

Outlook

Tin prices are likely to remain elevated in the near term, supported by lingering Myanmar-related risk premiums and still-tight visible inventories. However, with Indonesian exports normalising and downstream Chinese demand only gradually recovering post-holiday, upside momentum may slow. If spot transactions fail to improve above RMB 430,000/t, profit-taking could trigger short-term volatility and a technical pullback.

Leave a Reply