- Manual-mining ban extended in DRC’s North, South Kivu

- China’s tin ore imports plunge in Oct’25 amid limited supply

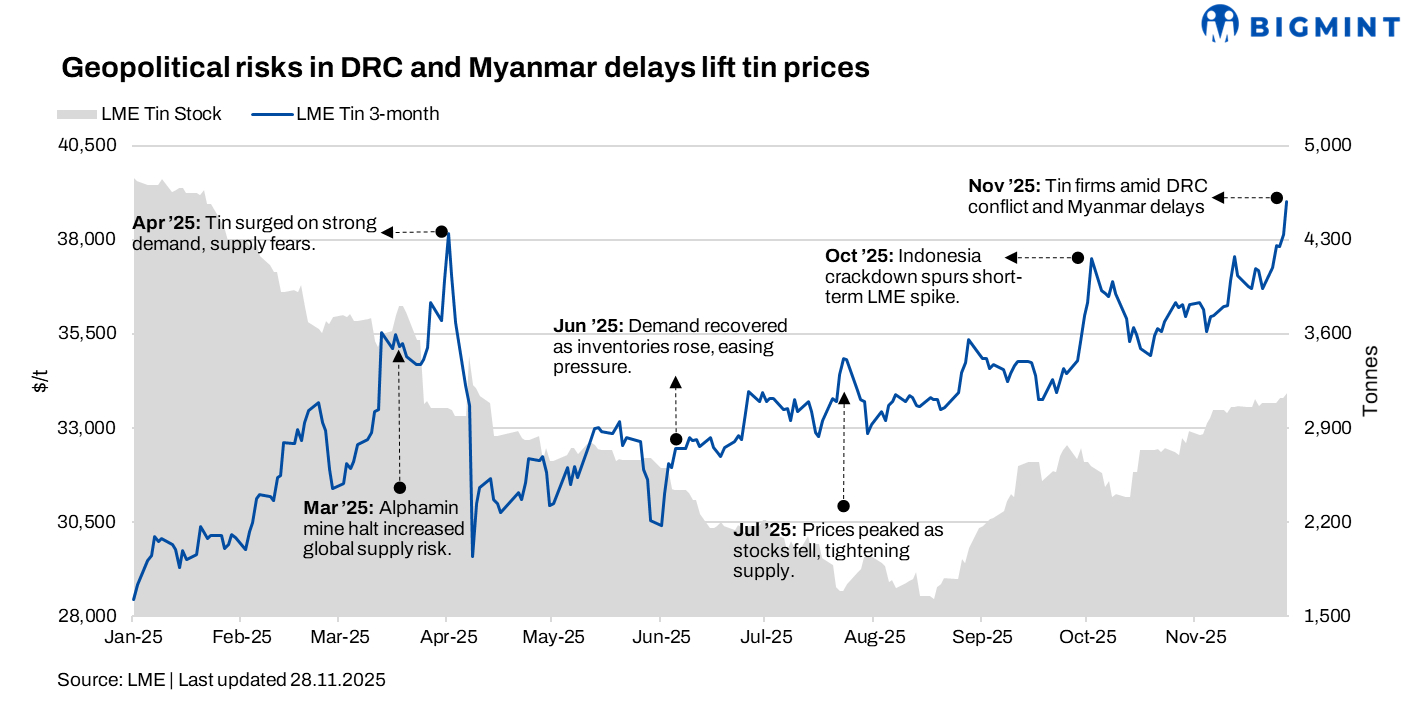

Tin prices on the London Metal Exchange (LME) inched higher during week 48 of CY’25 (24-28 November), driven by escalating geopolitical tensions in the eastern belt of the Democratic Republic of the Congo (DRC), extended mining bans, and slow production recovery in Myanmar. Tight supply, low inventories, and rising logistical risks underpinned market sentiment and price resilience.

Pricing, inventory trends

LME tin prices averaged $38,022/tonne (t) in week 48, marking an $1,099/t or 3% rise w-o-w from week 47 (17-21 November). The week began with prices at $37,275/t, which inched up to around $37,825/t mid-week and then closed at $39,010/t.

Meanwhile, tin inventories at LME-registered warehouses rose to 3,116 t from 3,075 t in week 47.

What impacted prices?

LME tin prices firmed up w-o-w, as escalating geopolitical tensions in key African producing regions heightened supply-side risks. Intensified conflict across major tin-mining provinces in the eastern DRC raised concerns over future transport disruptions and higher logistics costs, even though operations at the Bisie mine remained unaffected for now.

Markets also priced in tighter raw material availability, with the extension of the manual-mining ban in DRC’s North and South Kivu adding to worries over ore flows from a region supplying roughly 8% of global output. Meanwhile, Myanmar’s slow production recovery — hampered by the rainy season, equipment constraints, and labour shortages — kept Chinese smelters facing limited feedstock, reflected in a sharp y-o-y drop in October imports.

With inventories at historically low levels and supply uncertainties rising, traders built in a geopolitical premium, lifting LME tin prices. Despite cautious downstream buying, fragile supply conditions and low stock coverage continued to support prices over the week.

Outlook

Tin prices are likely to remain supported in the near term due to ongoing geopolitical tensions in the DRC, extended mining restrictions, and slow production recovery in Myanmar. Tight global supply, low inventories, and logistical uncertainties may continue to underpin market sentiment, while high prices could limit downstream purchasing activity.

Leave a Reply