- Oversupply, weak demand put pressure on nickel prices

- NPI prices are rising amid supply constraints

- Shifts in global nickel supply dynamics

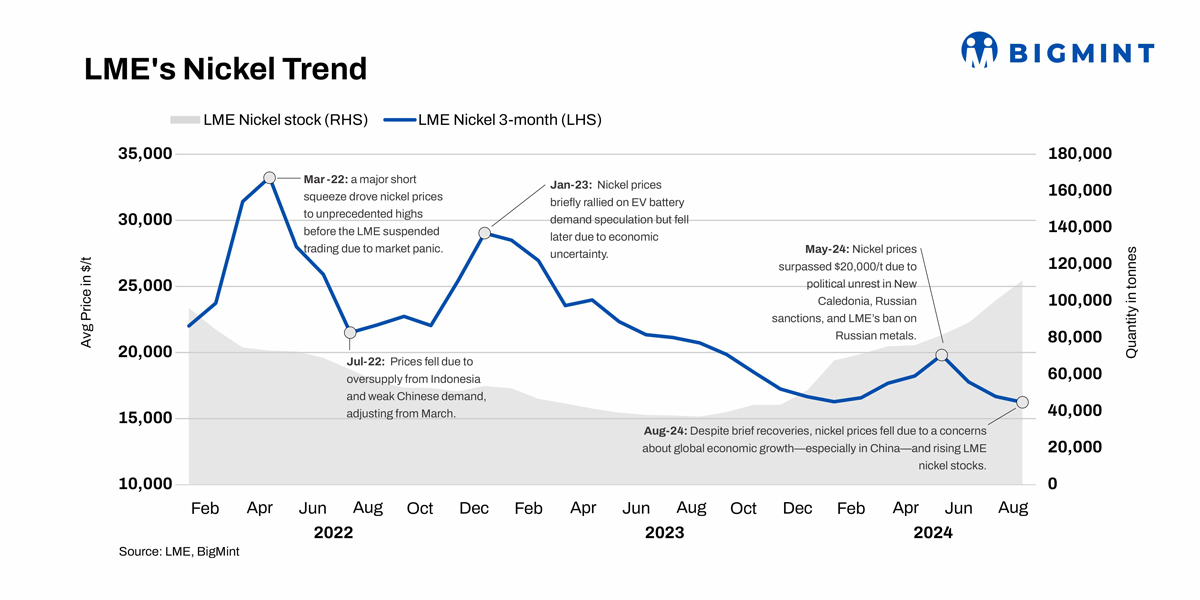

The recent decline in nickel prices, as reported by Metal Miner, highlighted a significant shift in the market dynamics. In July, nickel prices dropped by 4.43% and have continued to trend downward into August. This decline effectively erased the gains made earlier in the year during a speculative uptrend.

In the first quarter of 2024 (Q2 2024), nickel prices on the London Metals Exchange (LME) experienced considerable fluctuations. Prices initially surged to over $21,000/t, driven by supply disruptions and geopolitical tensions. However, by the end of June, prices had fallen sharply to $17,291/t. This drop was primarily due to bearish market sentiment and concerns over oversupply.

These developments suggested a more cautious outlook for the nickel market, with potential implications for industries relying on this metal, such as stainless steel production and electric vehicle battery manufacturing. The market may continue to face challenges if the current trends persist.

Price trends, challenges in nickel pig iron (NPI)

Rising NPI prices: Since the beginning of 2024, prices of Indonesian nickel ore and nickel pig iron (NPI) have experienced notable increases. Nickel ore prices have surged significantly, with laterite ore (1.2% nickel content) rising by over 16% and ore with 1.6% nickel content climbing nearly 50% by early August. Concurrently, NPI prices from Indonesia have risen by almost 8% since the start of the year.

Factors driving price increases: The primary driver of the earlier price increases was the limited availability of nickel ore in Indonesia. Delays in issuing mining licenses by the Indonesian authorities have significantly constrained the supply of ore, contributing to the price surge.

Government actions, ore reserve concerns: In response to the rapid depletion of nickel reserves, the Indonesian government has implemented a moratorium on new nickel smelter constructions to conserve the country’s dwindling resources. Reports indicate that Indonesia’s high-grade nickel ore reserves could be exhausted within the next 13 to 15 years if extraction continues at the current rate. This government action aligns with earlier forecasts predicting that high-grade reserves might be depleted by 2029. Additionally, the remaining low-grade deposits, primarily used for battery production, are also expected to diminish soon.

Implications for NPI smelters: The depletion of nickel ore reserves has sparked discussions about potentially limiting the number of nickel pig iron (NPI) smelters. It remains uncertain whether such restrictions would impact existing plants or only those still in the planning stages. Looking ahead, recent developments-such as the rise in NPI prices and the expansion of nickel listings by Tsingshan Group on the LME-suggest an expectation of continued high demand and rising prices. These trends reflect ongoing challenges in the nickel market, driven by limited domestic ore supply in Indonesia and increased imports from the Philippines.

Weak stainless steel demand exerting pressure on prices

BigMint’s assessment reveals that the price of 304 HRC, exw-Mumbai, fell by 12% y-o-y, reaching INR 178,000/t in August 2024, down from INR 202,750/t the previous year. This decline is mainly attributed to weak demand for finished products and volatility in raw material prices.

The global stainless steel market remains weak, marked by a significant drop in demand. The Stainless Monthly Metals Index (MMI) decreased by 4.47% from July to August, reflecting a continuing buyer’s market and low optimism among distributors. Q2 2024 results underscored this softness, showing a 4.9% decline in stainless steel shipments from Q1 2024, as well as a y-o-y decline. Additionally, sectors such as commercial food service and other end-use industries are reporting weaker sales, further exerting pressure on stainless steel prices.

Nickel production, inventory in LME

Nickel production remained high, and inventory levels at the London Metals Exchange (LME) have been increasing, signaling an oversupply situation. Despite recent supply disruptions due to geopolitical issues and mine shutdowns, the market is projected to experience a surplus of 109,000 t in 2024, according to the International Nickel Study Group (INSG) forecast. Indonesian and Chinese nickel production are expected to constitute a significant portion of global output, with a marked increase in ore imports from the Philippines.

In June, the Philippines continued as China’s primary source of nickel ore and concentrates, with exports exceeding 4.39 mnt. However, this represented a 10% decline compared to the previous year. For the first half of 2024 (H1’FY24), China’s total imports of nickel ore from the Philippines were around 14 mnt, a 3% y-o-y decrease. Concurrently, China’s imports of nickel sulfate from Indonesia surged, with Indonesia supplying 77.4% of this material, up from 16% in 2023.

The Philippines is also a key supplier to Japan, South Korea, and Indonesia. Since May, it has increased its nickel exports to Indonesia and is aiming to become the world’s leading nickel producer. The Philippines is planning to establish three new nickel processing plants by 2028 and is considering imposing taxes on nickel ore exports to encourage increased investment in domestic processing infrastructure.

Nickel in battery applications

Demand for nickel in battery applications, especially in nickel-manganese-cobalt (NMC) batteries, has been weak, according to SMM. While nickel sulfate prices surged earlier in the year, they have since fallen significantly due to a slowdown in NMC battery production and weaker overall demand. In China, nickel sulfate prices dropped from RMB 33,000/t ($4,617/t) in early June to RMB 27,000/t ($3,777/t) by the end of the month. Despite nickel sulfate’s importance in battery production, current market conditions suggest limited potential for price increases in the near term.

Outlook

The nickel market is currently marked by weak prices and oversupply. Subdued demand for stainless steel is impacting nickel’s role in stainless steel production. With high production levels and increasing inventories, the nickel market is expected to remain under pressure. Additionally, the decline in demand for battery-grade nickel highlights broader challenges in the industrial metals sector. As the market contends with these conditions, future developments in global production, inventory levels, and demand from key sectors will be critical to monitor.

Leave a Reply