- Weak stainless steel demand, easing geopolitical risks weigh on prices

- LME inventories increase marginally but supply concerns persist

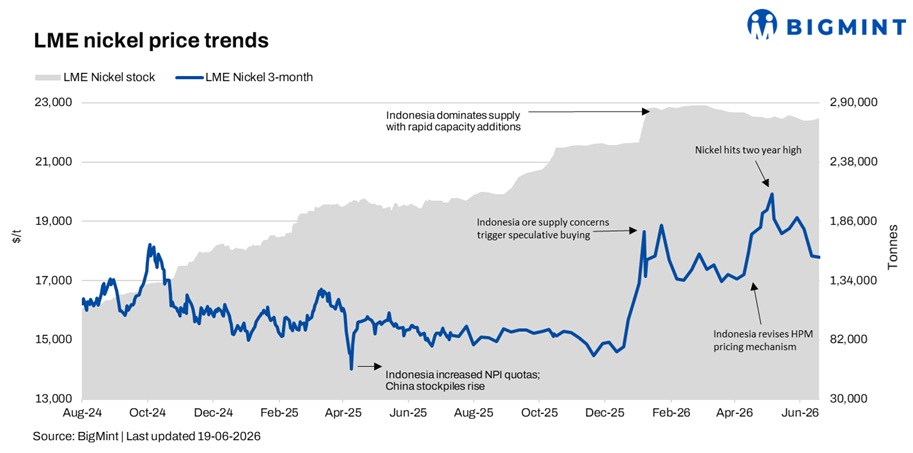

London Metal Exchange (LME) nickel futures inched down during the week ended 19 June 2026, closing at $17,780/t compared with $17,830/t a week earlier. Meanwhile, LME nickel inventories also showed limited movement, standing at 276,216 t against 274,938 t in the previous week, reflecting a balanced market amid mixed supply and demand signals.

Indonesia policies keep supply outlook in focus

Market participants continued to monitor developments in Indonesia’s nickel sector, where tighter mining regulations, revised ore pricing mechanisms, higher royalty rates, and stricter production controls have raised concerns among investors. Chinese companies, which account for a significant share of Indonesia’s nickel refining capacity, have highlighted rising production costs and regulatory uncertainty, prompting concerns over future investment and supply growth.

The Indonesian government’s efforts to strengthen control over its mineral resources and promote higher-value downstream processing are expected to tighten oversight of nickel output, potentially affecting the pace of future supply additions. These developments continued to provide underlying support to nickel prices despite broader market weakness.

Demand pressure, easing geopolitical risks cap upside

On the demand front, stainless steel markets across Asia remained subdued, with buyers largely adopting a wait-and-watch approach amid weak end-user demand and adequate inventories. Market participants reported limited spot activity, while concerns over slowing industrial activity continued to weigh on nickel consumption expectations.

Additionally, the recently finalised US-Iran agreement has eased geopolitical tensions in the Middle East, reducing concerns over disruptions to global energy supplies. The subsequent decline in crude oil prices has softened inflation expectations and lowered risk premiums across commodity markets. Market participants noted that the reopening and normalisation of traffic through the Strait of Hormuz could ease sulphur supply constraints outside China, potentially reducing production costs across parts of the nickel value chain. Combined with elevated LME nickel inventories, these developments have limited upside momentum in nickel prices despite ongoing supply-side concerns from Indonesia.

Outlook

Market participants expect nickel prices to remain largely stable in the near term. While Indonesia’s evolving regulatory framework and potential supply-side constraints may offer support, weak stainless steel demand and cautious macroeconomic sentiment are likely to cap significant upside. The market will closely watch developments in Indonesia’s mining sector, inventory trends, and stainless steel production levels for clearer price direction.

Leave a Reply