- LME nickel declines 5% w-o-w amid cautious sentiment

- Exchange inventories remain near multi-year highs

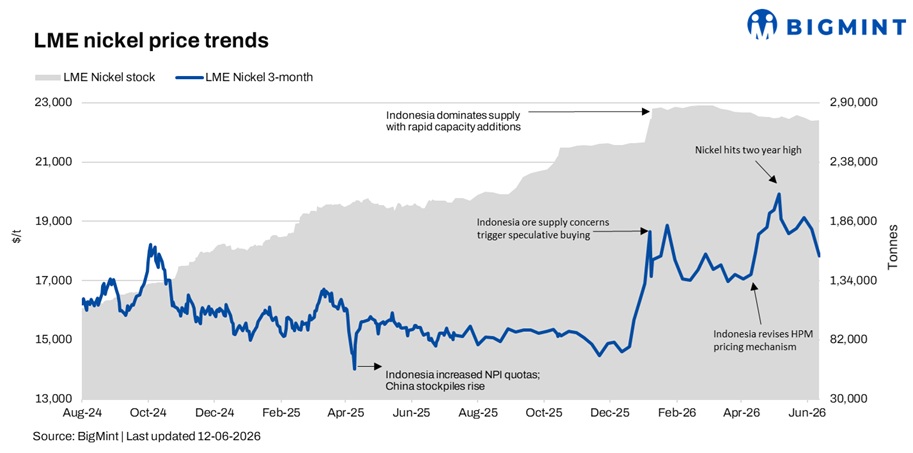

London Metal Exchange (LME) nickel futures declined 5% w-o-w to $17,830/t on 12 June 2026 from $18,750/t a week earlier. Meanwhile, LME nickel inventories increased marginally to 274,938 t from 274,236 t over the same period, highlighting continued inventory pressure on the market.

Nickel prices remained under pressure as growing exchange inventories and weak stainless steel demand outweighed ongoing concerns surrounding Indonesia’s ore supply restrictions. Combined nickel inventories across the LME and Shanghai Futures Exchange (SHFE) have risen to nearly 469,000 t, the highest level since 2015, reinforcing concerns of continued oversupply in the refined nickel market.

Inventory burden weighs on sentiment

Market participants noted that rising refined nickel inventories, particularly in China, have emerged as a key bearish factor. China’s refined nickel imports increased significantly during the first four months of 2026, contributing to higher domestic stock levels and dampening expectations of a near-term market rebalancing.

At the same time, uncertainty surrounding US inflation, interest rates, and a stronger dollar continued to weigh on investor sentiment across the broader non-ferrous metals complex.

Indonesia premium loses momentum

While Indonesia’s reduced ore mining quotas and supply restrictions continue to support the market fundamentally, participants increasingly believe these risks have already been priced in. Concerns have also eased amid expectations that Indonesia could revise quotas later in the year, as seen in previous years.

Additionally, Indonesia’s decision to exclude nickel pig iron (NPI) from its proposed strategic export control framework has been interpreted as a signal that policy tightening may be less severe than initially feared.

Outlook

Nickel prices are expected to remain range-bound in the near term as the market balances persistent inventory overhang against ongoing supply-side risks from Indonesia. Future price direction will largely depend on Indonesian mining policy developments, Chinese stainless steel production trends, and inventory movements across global exchanges.

Leave a Reply