- Oil prices drop by over 6% on hopes of Middle East de-escalation

- Copper sentiment stays bullish amid tight supply, tariff concerns

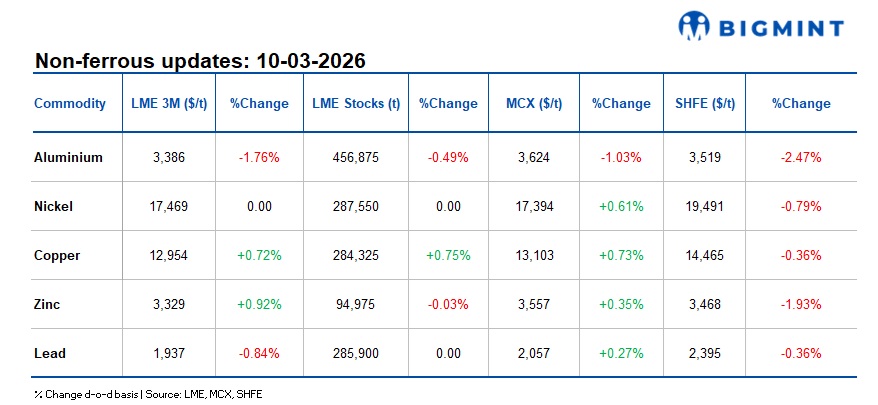

Base metals on the London Metal Exchange (LME) traded on a mixed note d-o-d on 10 March 2026. Aluminium declined 1.76% to $3,386/t, while zinc advanced 0.92% to $3,329/t. Lead slipped 0.84% to $1,937/t, and nickel remained largely unchanged at $17,469/t. In contrast, copper posted gains of 0.72%, reaching $12,954/t.

Warehouse inventory movements were also mixed but broadly stable. Aluminium stocks edged down 0.49% to 456,875 t, and zinc inventories dipped slightly by 0.03% to 94,975 t. Nickel inventories remained steady at 287,550 t. Meanwhile, copper stocks increased by 0.75% to 284,325 t, while lead inventories were unchanged at 285,900 t.

Domestic market overview

Domestic non-ferrous scrap prices in India remained largely stable across key markets, indicating balanced demand and cautious trading activity. Aluminium tense scrap (loose), ex-Delhi, held steady at INR 224,000/t, while ex-Chennai prices also remained unchanged at INR 230,000/t.

However, copper armature scrap (Cu 99%), ex-Delhi, declined by INR 5,000/t (0.4%) to INR 1,140,000/t from INR 1,145,000/t. The drop reflects mild selling pressure amid fluctuations in refined copper prices and cautious procurement by downstream buyers.

Other market updates

Oil prices slide over 6% on hopes of Middle East de-escalation

Global crude oil prices dropped sharply on 10 March after comments from US President Donald Trump suggesting that the ongoing Middle East conflict could end soon, easing concerns over prolonged supply disruptions.

Brent crude fell around 6-7% to nearly $92-94/bbl, while WTI declined to about $88-91/bbl, retreating from the previous session’s surge above $119/bbl, which had been driven by fears of supply shortages amid the escalating US-Israel-Iran conflict and output cuts from Gulf producers.

The market correction reflects cooling geopolitical risk sentiment, as expectations of a quicker resolution to the conflict reduced concerns about disruptions to global oil flows, particularly from the Middle East region. However, analysts noted that oil markets may remain volatile as geopolitical developments continue to unfold.

Aluminium retreats on profit booking as supply concerns ease

Aluminium prices declined as investors booked profits after US President Donald Trump indicated a potential quick resolution to the Middle East conflict, easing immediate supply concerns.

The most-active SHFE aluminium contract fell 2.47% to RMB 24,505/t, while LME three-month aluminium dropped 1.76% to $3,386/t, retreating from recent multi-year highs.

Earlier gains were driven by disruptions in the Strait of Hormuz, a key route for Gulf shipments accounting for nearly 9% of global aluminium supply. However, aluminium remains vulnerable to renewed volatility if geopolitical tensions escalate again.

Copper rally driven by supply tightness, tariff concerns, mine disruptions

Copper prices are strengthening amid tight global supply, driven by fears of potential US tariffs, disruptions at major mines, and rising demand linked to electrification and infrastructure expansion.

Market participants are also stockpiling copper ahead of possible US import tariffs, which could tighten availability on global exchanges. At the same time, production challenges at key mining operations have constrained supply, further supporting prices.

The combination of limited mine output, policy uncertainty, and strong demand from sectors such as EVs, power infrastructure, and AI-related projects is expected to keep the copper market tight, sustaining bullish sentiment in the near term.

Leave a Reply