- LME aluminium resilient near $3,400/t despite broader market weakness

- EGA adjusts logistics to sustain aluminium exports amid Gulf tensions

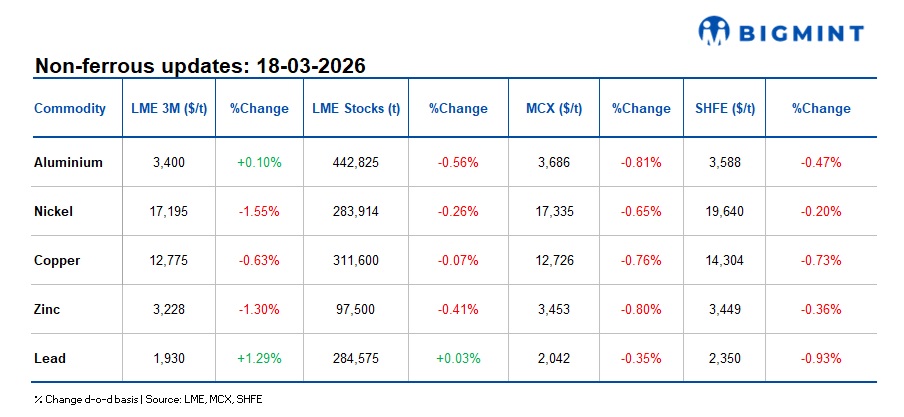

Base metals on the London Metal Exchange (LME) traded mixed but largely lower d-o-d on 18 March 2026, amid cautious market sentiment. Aluminium inched up 0.10% to $3,400/t, while zinc declined 1.30% to $3,228/t. Lead gained 1.29% to $1,930/t, whereas nickel fell 1.55% to $17,195/t, and copper slipped 0.73% to $12,775/t.

Warehouse inventory levels were mostly lower. Aluminium stocks decreased 0.56% to 442,825 t, while zinc inventories dipped 0.41% to 97,500 t. Nickel stocks fell 0.26% to 283,914 t, and lead inventories edged up 0.03% to 284,575 t. Meanwhile, copper stocks declined slightly by 0.07% to 311,600 t.

Domestic market overview

Domestic non-ferrous scrap prices in India showed mixed but largely stable trends, reflecting cautious market sentiment. Aluminium tense scrap (loose), ex-Delhi, remained unchanged at INR 240,000/t, while ex-Chennai prices also held steady at INR 244,000/t.

Meanwhile, copper armature scrap (Cu 99%), ex-Delhi, declined by INR 2,000 or 0.2% to INR 1,108,000/t from INR 1,110,000/t, indicating weak buying sentiment in the market.

Other updates

Gulf producers reroute oil as Hormuz disruption intensifies

Gulf oil producers are accelerating efforts to bypass the Strait of Hormuz after Iran effectively restricted maritime traffic through the critical chokepoint, which typically handles ~20% of global oil and LNG flows.

Major exporters such as Saudi Arabia and the UAE are increasing utilisation of alternative pipeline routes. Saudi Arabia has ramped up flows through its East-West pipeline to ~5.9 mb/d (with ~7 mb/d capacity), while the UAE is diverting crude via the Habshan-Fujairah pipeline to maintain export continuity.

However, these alternative routes offer limited capacity compared to seaborne flows, highlighting structural constraints in global supply chains. The disruption underscores rising logistics risks and supply tightness, adding upward pressure on oil prices and increasing volatility across global energy and commodity markets.

Japanese refiners cut runs further

Japanese refiners have further reduced operating rates as crude supply disruptions from the Middle East intensify due to the ongoing Iran conflict. Refinery utilisation fell to 69.1% for the week ending 14 March, down sharply from 77.6% a week earlier and over 80% before the conflict.

The cuts reflect tightening availability of Middle Eastern crude, with the Strait of Hormuz disruption severely impacting supply flows to Asia. The decline in refining activity highlights growing stress across regional energy supply chains, adding to global oil market tightness and volatility.

Global energy security diverges amid as Iran crisis

The ongoing Iran conflict and disruption of flows through the Strait of Hormuz are exposing varying levels of energy security across major economies, with global markets facing heightened volatility. The strait typically carries ~20% of global oil and LNG trade, making the disruption a major supply shock.

The United States remains relatively insulated due to strong domestic oil and gas production, while Europe is more vulnerable given its reliance on imported energy and LNG. China, although a major importer, is better cushioned in the short term due to large reserves and a higher share of domestic energy sources.

Overall, the crisis highlights diverging resilience across global economies, with prolonged disruptions likely to sustain elevated energy prices, inflationary pressures, and volatility across commodity markets.

EGA reroutes aluminium exports via Oman

Emirates Global Aluminium (EGA) is shifting its aluminium exports and raw material imports through Oman’s Sohar port to bypass disruptions in the Strait of Hormuz, a critical global shipping route.

The company plans to truck alumina feedstock to UAE smelters and transport finished aluminium back to Sohar for export, as regional producers adjust logistics amid ongoing conflict.

The Gulf region accounts for ~9% of global aluminium supply, and rerouting challenges highlight growing logistics constraints and supply risks, supporting elevated aluminium prices and increasing volatility across global metals markets.

Rusal swings to loss on rising costs, lower output

Russia’s aluminium major Rusal reported a net loss of $455 million in 2025, reversing a $803 million profit in 2024, mainly due to rising costs and lower primary aluminium output.

Despite a 22.6% rise in revenue to $14.81 billion, the company’s cost of sales surged 32.3%, driven by higher alumina costs and increased sales volumes. Aluminium production declined by ~2%, even as sales volumes grew 16.4% to 4.49 mt.

Rusal continues to face indirect pressure from Western sanctions and weaker demand in Europe, prompting a shift in focus toward Asian markets. Higher aluminium prices (up 5.2% to $2,652/t) provided some support, but were insufficient to offset cost pressures.

Leave a Reply