- Market lacks strong bullish triggers

- Gradual stock drawdown cushions downside

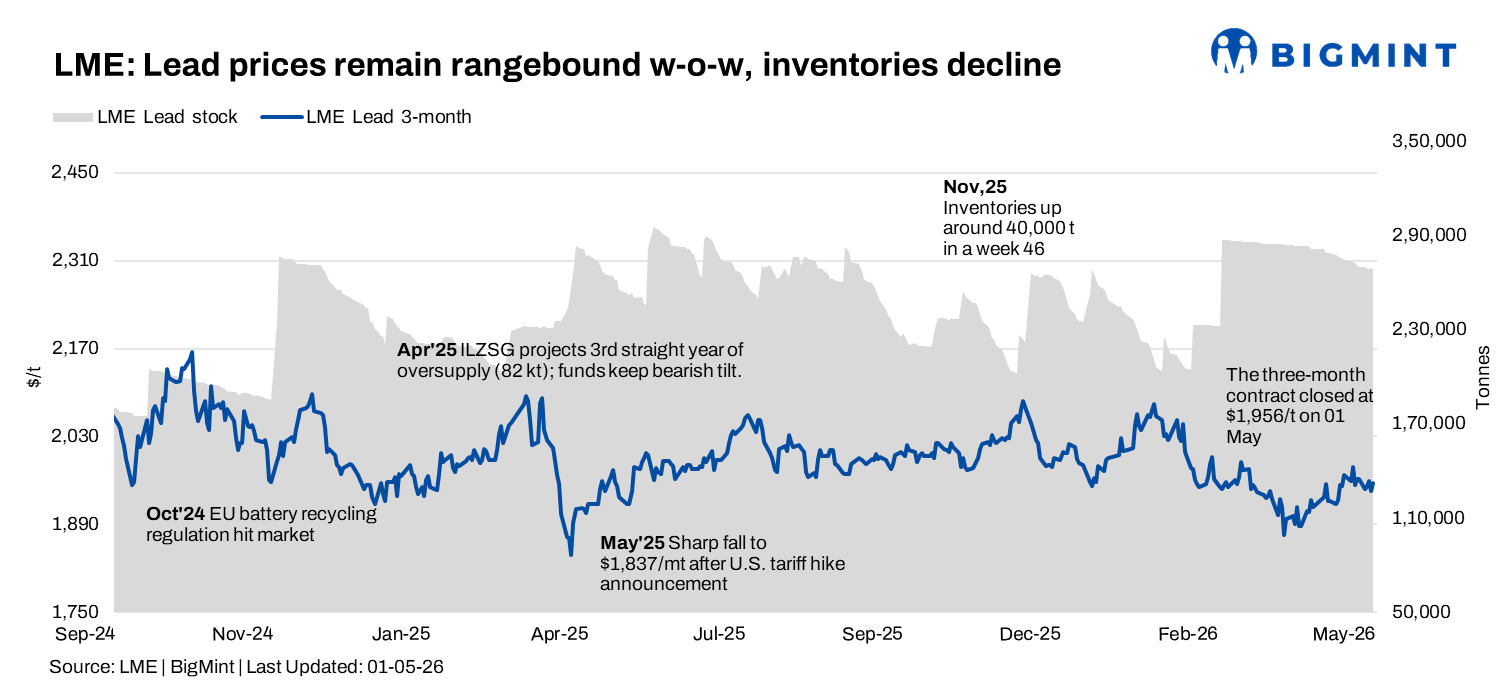

Lead prices on the London Metal Exchange (LME) remained largely range-bound in the week ended 1 May 2026, with limited directional movement and a slightly softer bias. While prices witnessed minor fluctuations through the week, the broader trend stayed sideways as cautious sentiment and need-based buying capped strong upside.

Price trends

The LME three-month lead contract opened the week at $1,945.50/t on 27 April and followed a fluctuating trend.

Prices rose to a weekly high of $1,959/t on 29 April before easing to a low of $1,944/t on 30 April. The market remained stable towards the end of the week, closing at $1,956/t on 1 May.

On a w-o-w basis, prices edged down marginally by around 0.3%, indicating the absence of strong momentum on either side.

Overall, prices traded within a narrow band, with resistance seen near the $1,960-1,980/t range, while support was observed around $1,940/t.

Inventory analysis

LME lead inventories continued their gradual downward trend during the week, declining from 270,025 t on 24 April to 268,500 t by 1 May.

This marks a net drawdown of around 1,525 t, reflecting steady outflows from exchange warehouses.

The moderate pace of decline suggests stable consumption patterns, offering mild support to prices. However, the absence of sharp stock depletion indicates no immediate supply tightness, keeping the overall market balanced.

SHFE lead trends

On the Shanghai Futures Exchange (SHFE), lead prices remained largely stable with a narrow trading range.

Prices hovered between $2,385/t and $2,398/t during the week, closing at $2,394/t on 1 May.

The muted movement indicates subdued sentiment in the Chinese market, with limited buying interest and lack of strong recovery signals.

MCX price movements

On the Multi Commodity Exchange (MCX), lead futures traded in a narrow range and ended marginally higher during the week.

The May 2026 contract opened at INR 202,000/t on 27 April and declined sharply early in the week before stabilising, closing at INR 199,400/t on 1 May-down around 1.3% w-o-w.

Prices moved within a range of INR 198,700/t to INR 202,000/t, reflecting initial weakness followed by sideways consolidation.

Open interest declined from 303 lots at the beginning of the week to 290 lots by 1 May, indicating mild long liquidation and cautious participation. Trading volumes also moderated significantly after early-week activity.

Outlook

Lead prices are expected to remain range-bound in the near term, with support seen around $1,940/t and resistance near the $1,960-1,980/t range.

Ongoing inventory drawdowns may provide some underlying support, but subdued demand conditions and cautious market sentiment are likely to limit any sharp upside.

The overall trend is expected to remain stable, with prices continuing to trade within a narrow band amid balanced market fundamentals.

Leave a Reply