- LME stocks remain high in absolute terms

- MCX lead futures rise slightly w-o-w

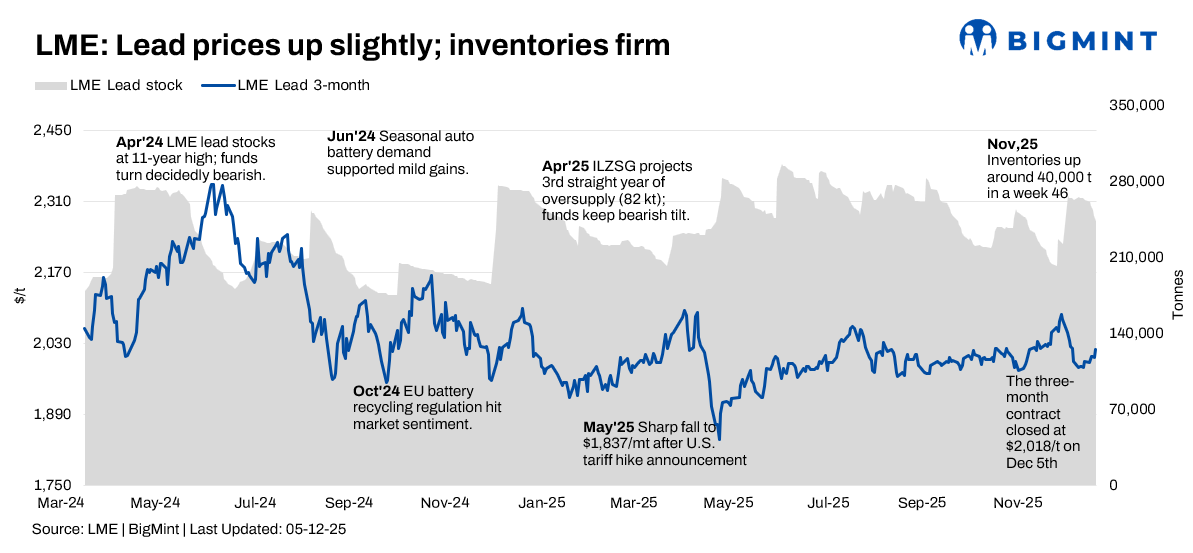

The London Metal Exchange (LME) lead market traded largely range-bound to slightly softer during 1-5 December 2025, with prices constrained by ample exchange stocks and a well-flagged global surplus. Seasonal support from winter battery-replacement demand provided only modest relief. Market sentiment remains cautious amid ILZSG expectations of a 102,000 t refined lead surplus in 2025, significantly higher than the 32,000-t year-to-date surplus, as the 2.4% refined output growth outpaced the 1.9% demand growth. Demand was primarily supported by steady replacement batteries and emerging industrial applications, partially offset by EV-led substitution headwinds in China.

Traders kept their gaze fixed on China’s modest 0.5% refined demand growth outlook, resilient global secondary recycling (now over 50% of supply), and possible US tariff risks affecting battery imports. Meanwhile, supply expansions across Australia, Mexico, and China continue to reinforce structural oversupply.

Price trends

LME 3-month lead prices were broadly stable, opening near $1,992/t on 1 December and ending at $2,018/t on 5 December — a marginal 0.1% week-on-week increase. The LME cash official price remained range-bound around $1,946-1,967/t, with intraday moves driven mostly by currency dynamics and broader base-metal flows rather than lead-specific fundamentals.

On a rolling one-month basis, 3-month prices remain effectively flat versus late-October levels near $2,000/t, highlighting how lead continues to lag the stronger zinc complex despite similar cost and regulatory backdrops.

Inventory analysis

LME lead stocks remained high in absolute terms but trended lower through the week, falling from 260,875 t on 1 December to 243,550 t on 5 December (down 6.6% w-o-w). Despite this drawdown, inventory levels in the mid-200,000-tonne range still signal structural oversupply. Combined registered and off-warrant stocks are estimated to exceed 400,000 t, with load-out queues persisting in hubs such as Singapore.

Chinese onshore inventories were broadly stable during the same period. As a result, the global physical market remains comfortably supplied, even though weekly LME outflows offered marginal price support.

MCX lead trends (1–5 December)

On India’s MCX, lead futures mirrored the subdued global tone. The near-month contract traded around INR 182,700/t on 1 December and closed near INR 182,850/t on 5 December, a slight 0.08% weekly increase. Domestic prices reflected steady but unspectacular demand from replacement batteries and inverter markets, weighed down by high imports and abundant global availability.

SHFE lead trend

On the SHFE, the most-traded January 2026 lead contract eased from RMB 17,000/t on 1 December to approximately RMB 16,900/t by 5 December, a 0.6% weekly decline. Prices hovered near multi-month lows, pressured by weak property-sector fundamentals and EV-driven substitution, though intermittent smelter cutbacks offered temporary cost support.

IFC Invests in GFCL EV to boost India’s battery materials ecosystem

The International Finance Corporation (IFC) has invested US $50 million in GFCL EV Products Ltd, a Gujarat Fluorochemicals subsidiary, to establish India’s first fully integrated EV battery-materials facility in Gujarat. The plant will produce LiPF₆, electrolytes, LFP cathodes, and PVDF/PTFE binders, significantly reducing India’s dependence on imports. The investment strengthens the country’s clean-energy supply chain and accelerates the transition toward sustainable mobility.

Outlook

Across LME, MCX, and SHFE, lead enters December on a neutral-to-soft bias. Elevated global inventories and the ILZSG-projected surplus limit upside potential, while replacement-battery demand provides a floor in the backdrop of China’s subdued 0.5% demand growth. Unless deeper supply disruptions emerge or significant macro stimulus materializes, prices are likely to remain range-bound with a mild downside skew. Upside risks hinge on unexpected demand boosts from grid-storage applications or tighter secondary-supply dynamics.

Leave a Reply