- Exide Industries reported a net profit of INR 221 crore in Q2

- MCX Lead prices closed around INR 183,550/t on November 14th

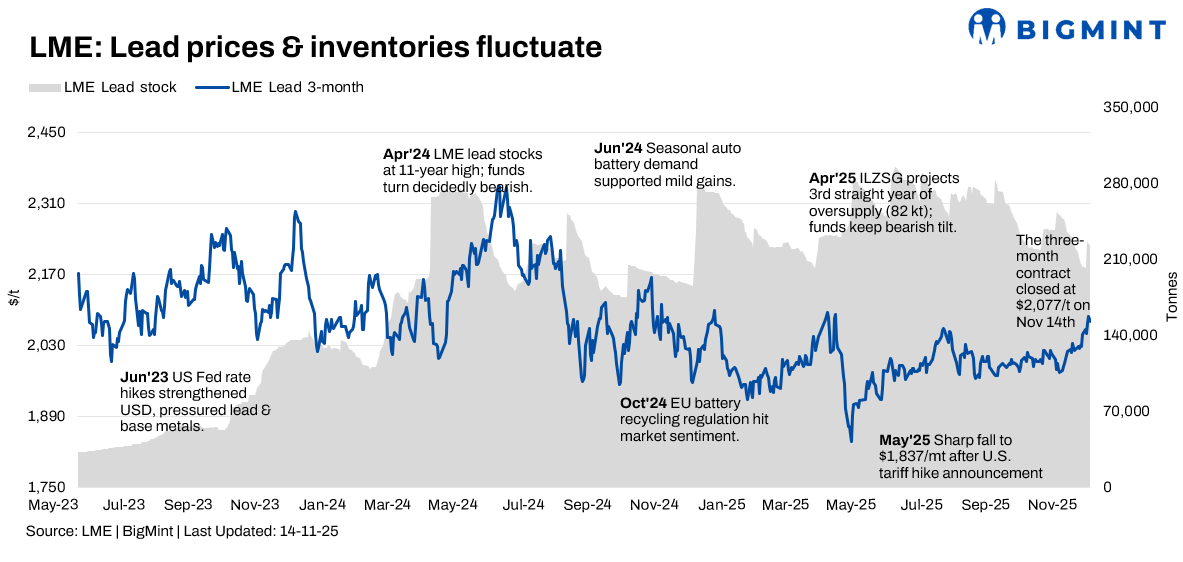

Lead prices on the London Metal Exchange (LME) stayed range-bound in the week ended November 14. Prices moved within a tight range, closing slightly higher despite a mid-week dip triggered by disappointing US economic data. Tightening LME inventories supported the market for most of the week, although weak Chinese demand continued to exert downward pressure.

Price trends

LME lead cash-settlement prices fluctuated throughout the week, opening at $2,043.50/t on November 10, falling to a weekly-low of $2,037/t on November 11, and rising to a high of $2,058/t on November 13, before closing at $2,056/t on November 14.

The market experienced strong mid-week momentum, with LME inventories falling to an eight-month low early in the week, coupled with an easing US government shutdown risk, pushing prices to a near nine-month high of $2,097/t.

However, disappointing US economic data in the latter half of the week prompted a pullback. The three-month contract followed a similar trajectory, starting the week at $2,062/t on November 10, rising to $2,087/t on November 13, before moderating to $2,077/t by the week’s close.

Inventory analysis

LME lead inventories displayed mixed movements. Stocks began the week at 202,200 tonnes on November 10, rose sharply by 12.13% to 226,725 tonnes on November 11, and then trended downward for the remainder of the week, settling at 222,475 tonnes on November 14. This late-week decline supported prices despite continued weakness in Chinese demand.

MCX lead trends (November 10-14)

MCX Lead prices reflected volatile global sentiment and domestic factors. The MCX Lead contract for the November expiry closed around INR 183,950/t on November 10th. While prices faced mid-week pressure, ending around INR 183,550/t on November 14th, but likely reflecting the same upward trend for the week’s settlement [Please clarify]. The Indian market was supported by factors like the rupee’s performance and tightening LME inventories, despite subdued domestic battery consumption.

SHFE lead trend

The most-traded SHFE lead 2512 contract opened at 17,440 yuan/t on November 10. After early-week fluctuations that saw a low of 17,435 yuan/t, a technical breakout propelled prices to a near nine-month high of 17,815 yuan/t. However, weak downstream demand and rising social inventories ahead of the delivery period caused a sharp late-week correction. By 15:00 Beijing time on November 14, SHFE lead settled at 17,495 yuan/t, up 75 yuan/t, or 0.43% w-o-w.

Exide Q2 profit falls to INR 221 crore

Exide Industries reported a net profit of INR 221 crore in Q2, down from INR 298 crore a year earlier. Revenue decreased 2.1% y-o-y to INR 4,178 crore from INR 4,267 crore, while EBITDA declined to INR 394.5 crore (versus INR 484 crore), reducing the EBITDA margin to 9.4% from 11.3%. The company attributed the setback to the mid-August GST rate cut, which delayed channel purchases and forced temporary production cuts.

Outlook

The near-term lead outlook for LME lead prices remains mixed. Market direction will depend heavily on US macroeconomic signals, especially economic data releases and interest-rate expectations. While tightening LME inventories offer support, weak Chinese demand presents a counter-force. Market participants will closely track consumption trends, SHFE movements, and LME stock dynamics for clearer price direction in the coming weeks.

Leave a Reply