- Sharp mid-week fall in LME inventories boosts prices

- Global refined lead demand projected to rise 2% in 2025

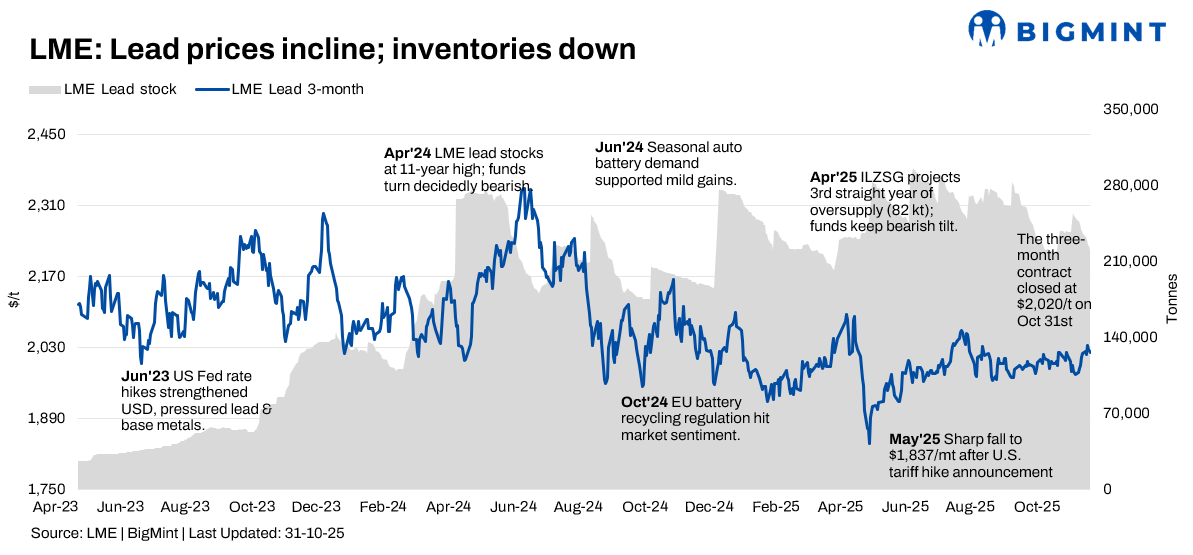

The global lead market experienced high volatility and price fluctuations during Week 43, ending with a marginal increase on the London Metal Exchange (LME). The market was driven by conflicting signals, including a sharp mid-week LME inventory destocking and a slump in the Shanghai Futures Exchange (SHFE) market due to a shutdown notice from major battery producers.

Price trends

LME lead cash-settlement prices showed notable fluctuations throughout the week. The week opened at $1,987/tonne (t) on 27 October and experienced a dip before fluctuating upward. By 31 October, LME lead settled at $2,017/t. This represents an approximate w-o-w increase of 1.51% in the cash price.

The three-month LME lead contract mirrored this general upward trend, settling at $2,020/t on 31 October, up 0.09% as against 24 October.

Inventory analysis

LME lead inventories saw a sharp destocking during the week. Stocks fell from 232,375 t on 27 October to 220,300 t on 31 October, with mid-week destocking exceeding 12,000 t. This significant decline in LME inventory, a strong bullish signal, was a key factor in supporting LME prices. Conversely, Chinese social inventory of lead ingots showed a consolidating trend, influenced by increased secondary lead production and a halt in procurement from major battery producers.

MCX lead trends (27-31 October)

MCX lead prices tracked the volatile global sentiment and were influenced by domestic factors. The MCX lead futures contract for November settled at INR 183,300/t on 27 October and closed at INR 183,350/t on 31 October, showing a slight increase of 0.42% over the week. Prices were influenced by the strong LME market but tempered by the weak Chinese demand signals and domestic factors. Consequently, amid conflicting signals from the strong LME and weak SHFE markets, the Indian market witnessed cautious trading activity.

SHFE lead trend

SHFE lead prices remained under pressure during the week due to the slump in domestic demand. The most-traded SHFE lead 2512 contract opened high at RMB 17,640/t before fluctuating downward and finally settling at RMB 17,390/t on 31 October, down 1.42% for the week. The market was bearish due to the unexpected halt in procurement from major battery producers, which outweighed the LME’s bullish signals.

Global refined lead demand forecast to climb up in 2025-2026 – ILZSG

Global refined lead demand is projected to rise 1.8% to 13.25 mnt in 2025 and 0.9% to 13.37 mnt in 2026. According to further projections, European demand will rebound 1.8% after a 2024 decline, led by Germany and Poland. The US will recover 6.6% on stronger battery output, while Chinese consumption is set to grow 0.9% in 2025 but fall 1.7% in 2026. Gains are also expected in Brazil, Türkiye, and Vietnam.

Outlook

The near-term lead outlook is mixed and volatile. While the significant LME destocking provides a bullish signal, the sharp slump in Chinese demand, as indicated by the SHFE market reaction to battery producer notices, is a major bearish factor. Market participants will closely monitor the sustainability of demand and inventory movements in both the LME and Chinese markets. The divergence between LME and SHFE trends is expected to continue influencing price direction in the short term.

Leave a Reply