- LME lead cash prices decline 1.5% w‑o‑w

- LG Energy Solution plans LFP battery production

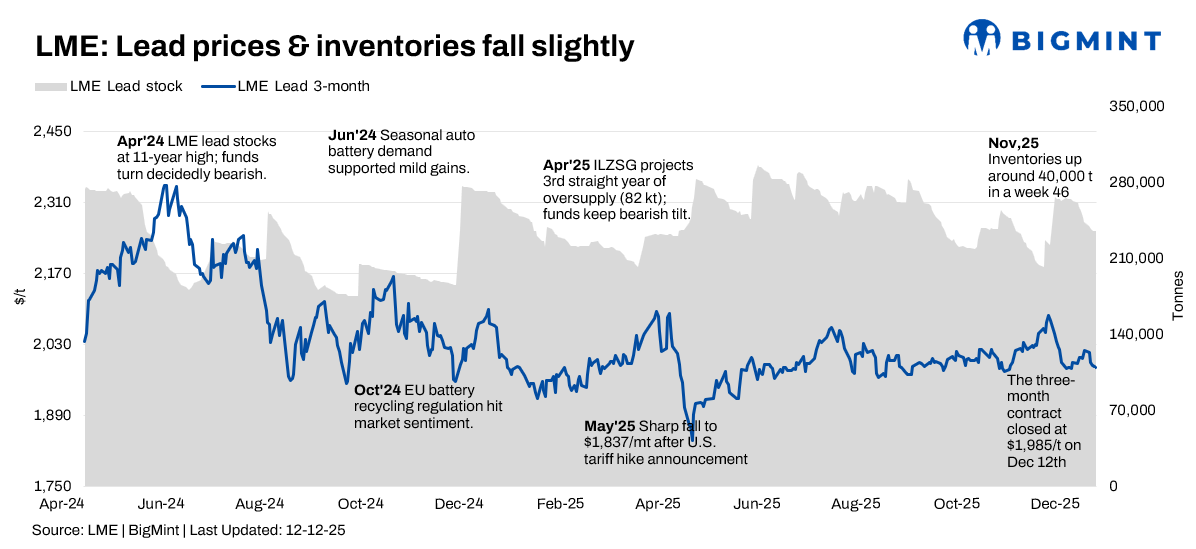

The LME lead market softened during 8-12 December 2025, drifting lower amid macro headwinds and surplus concerns, while high inventories and a well‑flagged 2025 surplus kept sentiment cautious despite modest stock drawdowns.

Price trends

LME lead cash prices eased from about $1,961.5/t on 8 December to 1,932.0 $/t by 12 December, a decline of $29.5/t or roughly 1.5% week‑on‑week. Over the same period, 3‑month prices also weakened, tracking the cash market lower and leaving lead down around 4.9% over the past month and about 2% below the same time last year on CFD benchmarks that track the underlying LME market. Intraday moves were modest and mainly driven by broad base‑metal sentiment and currency shifts rather than any specific lead‑sector shock, underlining the market’s current range‑bound, surplus‑dominated character.

Inventory analysis

LME lead stocks remained high in absolute terms but began to trend lower compared with late‑November peaks. Exchange data show stocks falling from 239,825 t on 8 December to 235,550 t on 10 December, and further to around 233,000-234,000 t by 12 December, implying a week‑on‑week decline of roughly 2%. Even after this drop, total LME‑related stocks (including off‑warrant estimates) still point to a structurally oversupplied refined market, with queues at key hubs such as Singapore indicating that large tonnages remain available to the market. Chinese social and on‑exchange inventories were relatively stable over the same period, so the global physical balance stayed comfortably supplied despite some regional tightening in concentrate flows.

MCX lead trends (8-12 December)

On India’s MCX, lead futures mirrored the soft tone on LME, edging lower over the week. The near‑month contract was trading close to about INR 183,500-184,000/t on 8 December and eased to roughly INR 182,100-182,200/t by 12 December, implying an approximate w-o-w decline of around 0.7-1.0% as prices tracked the 1-2% slip in international benchmarks. Domestic demand from replacement battery and inverter segments remained steady but not strong enough to offset pressure from abundant global supply and muted risk appetite, resulting in a mildly negative weekly performance.

SHFE lead trend

On the Shanghai Futures Exchange (SHFE), the most‑traded January 2026 lead contract fluctuated near CNY 17,000/t, consolidating at CNY 17,120/t by 12 December. Prices fell 0.3% w-o-w, staying close to multi-month lows, supported only marginally by smelter cost pressure and intermittent production cuts. Weak macro sentiment and concerns over China’s property sector limited upside.

Battery sector updates

- Panasonic & Zoox: Panasonic Energy will supply 2170-format cylindrical lithium-ion batteries to Amazon-owned robotaxi maker Zoox starting early 2026. Cells will initially be sourced from Japan, with future production in Kansas.

- Korean LFP Expansion: LG Energy Solution plans LFP battery production in Ochang (2027) after expanding in China, Michigan, and Poland. SK On will convert part of its Georgia line and build a 3 GWh ESS LFP plant in Seosan (mid-2026), while Samsung SDI targets 30 GWh capacity by late 2026 and mass production by 2028 to meet rising AI-linked ESS demand.

Outlook

Across LME, MCX and SHFE, lead continues to trade with a neutral‑to‑soft bias heading into mid‑December. High visible stocks and 2025 surplus expectations cap the upside, while stable but unspectacular replacement battery demand prevents a steeper slide. Unless there is a meaningful disruption in mine or smelter output or a stronger‑than‑expected macro rebound, lead is likely to stay range‑bound with a slight downward tilt, and any price rallies are still more likely to be used for hedging rather than signal the start of a sustained bull phase.

Leave a Reply