- Market remains cautious despite Fed rate cut expectations

- MCX prices hold firm on steady demand despite ample supply

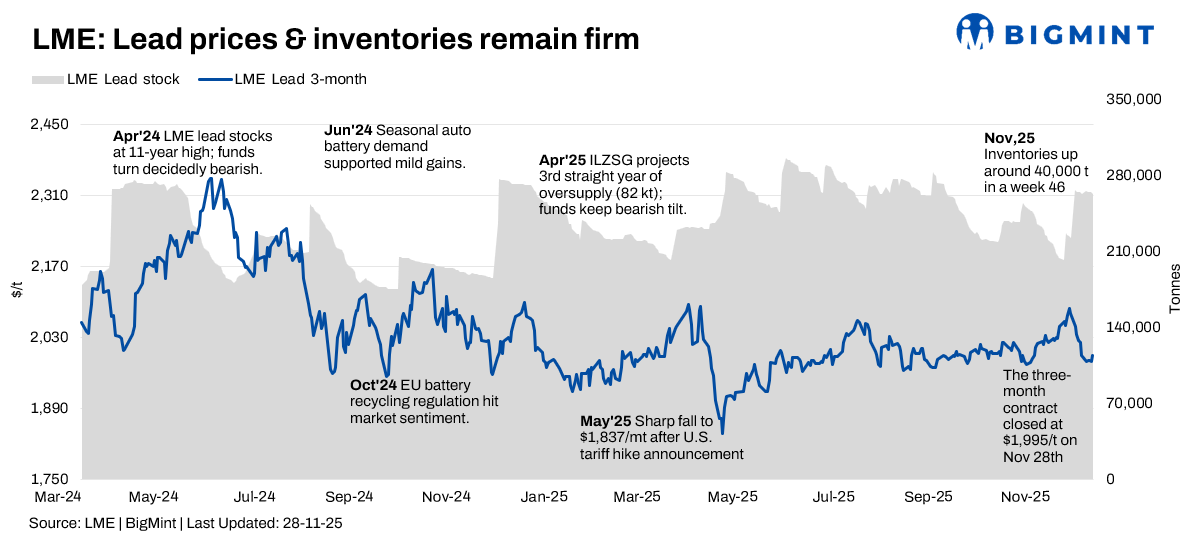

The London Metal Exchange (LME) lead market showed a marginal uptrend over 24-28 November 2025, with prices fluctuating narrowly amid steady inventories and a backdrop of global surplus fundamentals. Trading remained range-bound, as dip-buying offset concerns over softer demand signals from battery and construction sectors, while elevated warehouse stocks in key locations such as Singapore tempered any stronger upside momentum.

Price trends

LME lead cash prices opened around $1,960/t on 24 November, dipped to a low near $1,940/t mid-week, then recovered to close at approximately $1,990/t by 28 November, posting a modest weekly gain of about 1.5%. The three-month contract followed a similar path, trading from roughly $1,983/t to $1,995/t, up around 0.6% w-o-w after touching lows near $1,982/t amid fluctuating sentiment. Prices stabilised near the $1,980-1,990/t range, reflecting cautious positioning ahead of key economic data despite support from expectations of Fed rate cuts.

Inventory analysis

LME lead stocks remained ample and stable during the week, fluctuating narrowly from 265,275 t on 24 November to 264,975 t by 26 November, showing a minimal net change of less than 0.1%. This high stock level — well above historical averages — continued to signal structural oversupply, with combined registered and off-warrant inventories exceeding 400,000 t in late November amid ongoing load-out queues in Singapore averaging 95 days. Industry forecasts pointed to a 2025 surplus of around 32,000-102,000 t through year-end, capping price gains despite some regional tightness in prompt material.

MCX lead trends (24-28 November)

On the MCX, lead futures for the December contract traded around INR 180,000-182,000/t, opening near INR 181,200/t on 24 November and closing at approximately INR 181,700/t by 28 November, with a weekly gain of about 0.27%. Domestic prices reflected global stability, supported by steady demand from battery manufacturers but pressured by high imports and ample availability.

SHFE lead trend

On the SHFE, the most-active lead contract declined modestly by 1.0% from RMB 17,110/t on 24 November to RMB 16,945/t by 27 November, after hitting a near one-year low near RMB 15,885/t mid-week. The moderate rebound mid-week reflects cost support from smelter production halts, which tightened ingot supply amid balanced onshore demand. However, export pressures persisted, weighing on prices.

Amara Raja, Exide: strategies for EV era

Amara Raja Energy and Mobility has a presence in the Indian lead‑acid battery segment through its Amaron brand, operating 14 manufacturing units with integrated plastic and lead‑recycling facilities. Holding around 25% of India’s market share, it exports to more than 60 countries. The company is investing in new‑energy solutions, with plans for a 1 GWh lithium-ion project by FY’27 and scaling to a 16 GWh gigafactory by 2030, aiming to support electric vehicle and energy storage demand.

Exide Industries is a long-established player in energy storage, with a wide distribution network across India and exports to multiple countries. The company is transitioning to lithium-ion batteries through its subsidiary, investing INR 5,000 crore in a 6 GWh gigafactory, expected to start trials by FY’26. Strong OEM partnerships, particularly in the two-wheeler segment, position Exide to play a significant role in India’s EV battery market while maintaining its lead-acid battery operations.

Outlook

Lead markets across LME, MCX, and SHFE remain in consolidation mode amid persistent surpluses and high LME stocks, with late-November prices showing small gains of 0.5-1.5% on LME despite SHFE weakness. Key monitors into December include warehouse dynamics, Chinese export flows, and battery sector demand amid global EV slowdown risks. Structural oversupply suggests limited upside unless significant supply disruptions emerge.

Leave a Reply