- Chinese stocks stay high on weak battery sector demand

- India’s lead ingot imports decline 15% y-o-y in Jan-Jul’25

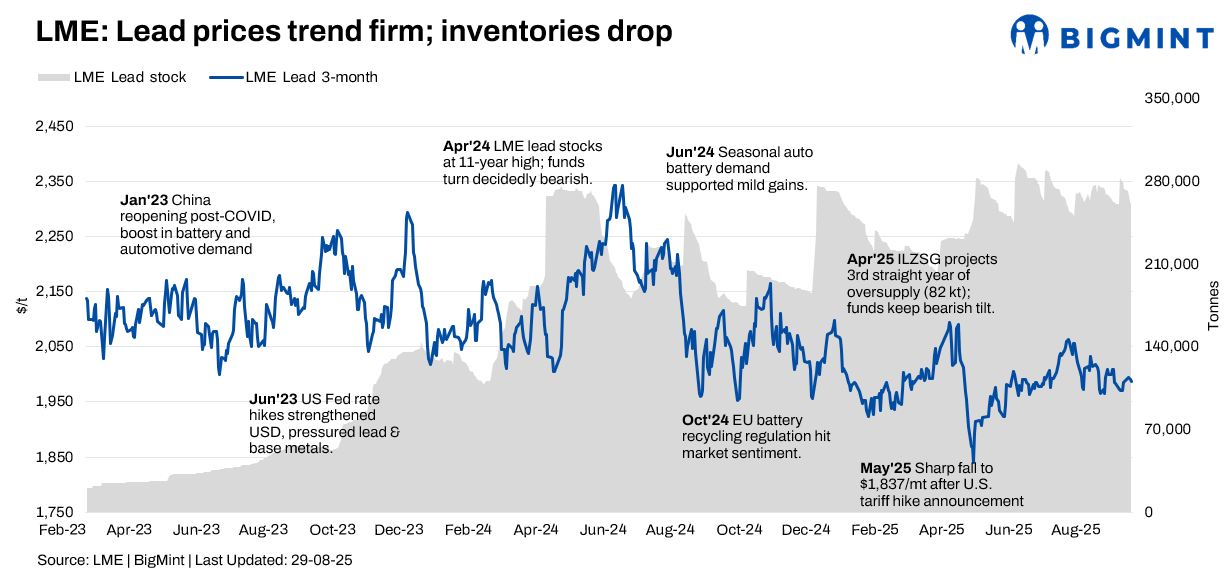

The London Metal Exchange (LME) lead market moved slightly higher during Week 35 (25-29 August 2025), supported by falling exchange inventories and a softer US dollar. However, market sentiment remained cautious, as concerns over sluggish battery demand in China weighed on the upside momentum.

Price trends

LME lead cash-settlement prices showed modest gains through the week. Prices opened at $2,148/tonne (t) on 26 August and closed slightly higher at $2,171/t on 29 August. Similarly, the three-month LME lead contract edged up, closing at $2,172/t on 29 August against $2,149/t on 26 August.

Inventories

LME lead inventories registered a decline during the week, to 87,800 t on 29 August from 92,475 t on 26 August. This drawdown provided some price support. In contrast, Chinese social inventories of lead ingots remained elevated, standing at around 106,000 t as of 28 August, reflecting weak downstream demand from the battery sector. The divergence highlights the global market’s tighter near-term availability versus continued oversupply pressures in China.

MCX lead trends (25-29 August)

MCX lead prices posted a modest w-o-w gain, mirroring the steady performance in global markets. The futures contract, which closed at INR 183,450/t on 25 August, inched higher to INR 184,650/t on 29 August. The upward movement was supported by a decline in LME inventories that underpinned sentiment. However, persistent weakness in domestic battery demand limited stronger gains in the Indian market.

India’s lead ingot imports decline in Jan-Jul’25

India imported 256,058 t of lead ingots in January-July 2025, down 15% y-o-y from 302,584 t in the same period in 2024, as scrap gained preference over primary ingots. South Korea remained the top supplier at 46,689 t (-56%), followed by Malaysia at 40,286 t (-36%) and the UAE at 30,208 t, reflecting sharp declines from major sources.

Global supply

Globally, supply remained uneven. Smelter curtailments in South Korea’s Seokpo smelter (58-day shutdown) and reduced production at Nyrstar’s European plants tightened regional availability. In contrast, China’s secondary lead output rose 6% y-o-y to 4.67 mt in January-July 2025, with August run-rates expected to push growth to 7% y-o-y, offsetting overseas supply disruptions.

Outlook

Overall, lead prices are expected to remain range-bound, with seasonal battery replacement demand offering limited upside amid flat global consumption trends.

Leave a Reply