- Mid-week buying lifts complex; $2,000/t remains key resistance

- Stocks stay elevated but easing volumes temper bearish pressure

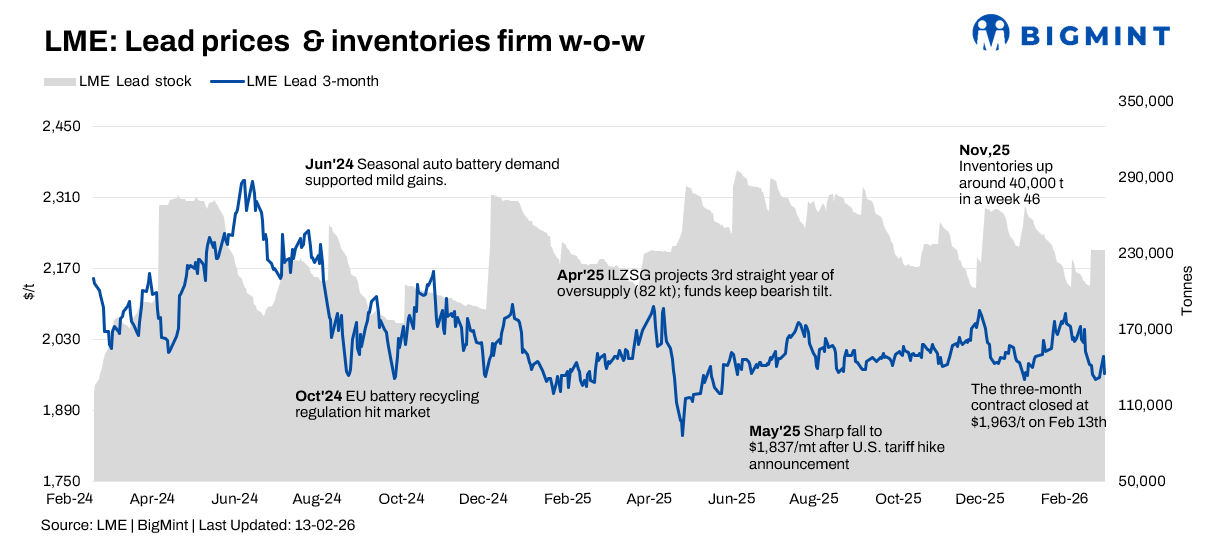

Lead prices on the London Metal Exchange firmed up in the week ended 13 February, supported by mid-week strength across the non-ferrous basket before profit-taking capped gains. Unlike the previous week’s sharp stock build, exchange inventories were broadly stable, providing a more balanced physical backdrop.

Price trends

LME cash lead opened at $1,903/t on 9 February and climbed to a weekly high of $1,949/t on 12 February, before settling at $1,918/t on 13 February, up 0.6% w-o-w. The three-month contract rose from $1,954/t to a peak of $1,997/t, closing at $1,963/t, up 0.7% w-o-w. The contract again tested resistance near the psychologically significant $2,000/t mark but failed to sustain a breakout, prompting fund-led profit booking toward week’s end.

Inventory analysis

LME lead stocks edged down marginally to 232,650 t on 13 February from 232,750 t at the start of the week, a modest 100 t decline. Mid-week inflows were limited compared with the prior surge, indicating a pause in heavy arrivals. While visible inventories remained elevated versus early-year lows, the absence of fresh builds tempered bearish pressure.

MCX price movements

On the MCX, the March 2026 lead contract tracked global cues but lacked domestic momentum, fluctuating between INR 189,000-193,000/t. Prices closed at INR 189,150/t on 13 February, down 0.9% w-o-w, with subdued volumes reflecting cautious battery-sector procurement.

SHFE lead trends

In contrast, dollar-denominated lead prices on the Shanghai Futures Exchange rose from $2,377/t to $2,415/t, signalling firmer sentiment amid relatively low concentrate treatment charges and underlying supply tightness. The stronger SHFE performance narrowed spreads, though import arbitrage remains largely unviable.

Outlook

Lead is likely to consolidate within the $1,900-2,000/t band in the near term. Stable exchange inventories reduce immediate downside risks, but elevated stock levels and muted physical demand may cap rallies unless sustained buying emerges. Cross-metal momentum and macro cues will remain key drivers.

Leave a Reply