- Weak demand, broader base metals softness prompts dip

- LME lead inventories decline for fourth consecutive week

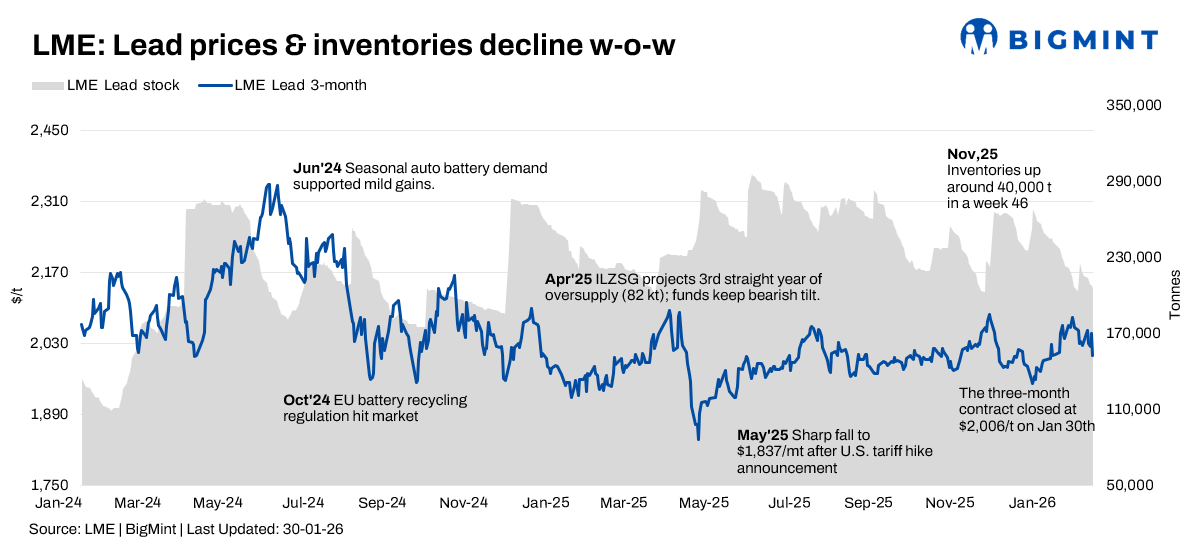

London Metal Exchange (LME) lead prices came under renewed pressure during 26-30 January 2026, correcting downward after a brief mid-week rebound. While steady inventory drawdowns offered underlying support, weak downstream demand and broader base metals softness capped upside momentum.

Price trends

LME lead cash prices opened the week at $2,009/t on 26 January but declined sharply in the first half, slipping to $1,972.5/t on 28 January. Prices staged a brief recovery to $2,004/t on 29 January before sliding again to close the week at $1,957/t, marking a 2.6% w-o-w decline.

The three-month contract followed a similar trajectory, easing from $2,056/t at the start of the week to $2,023/t mid-week, rebounding briefly to $2,050/t, and then settling lower at $2,006.5/t on 30 January, down around 2.4% w-o-w. Despite the correction, prices continued to hold above the key $2,000/t psychological support, limiting deeper losses.

Inventory analysis

LME lead inventories extended their downtrend for the fourth straight week, falling from 213,600 t on 26 January to 205,575 t by 30 January, a weekly decline of 8,025 t (3.76%). The sustained drawdown reflects continued warrant cancellations and steady physical offtake.

However, total stocks remain relatively elevated compared with historical averages, reinforcing market caution. Participants continue to track Chinese supply-side developments and regional availability closely, with inventories still acting as a ceiling on any sustained price recovery.

MCX lead trends (26-30 January)

On the MCX, near-month lead futures on 27 February 2026 witnessed sharp volatility during the week, tracking global weakness and mid-week profit-taking. Prices rose from INR 191,300/t on 27 January to a weekly high of INR 201,650/t on 29 January, before retreating to settle at INR 191,350/t on 30 January, ending the week largely flat w-o-w.

Open interest increased from 513 lots to 905 lots, indicating fresh participation and rollover activity, while trading volumes spiked mid-week, suggesting active short-term positioning.

SHFE lead trend

On the SHFE, lead prices edged slightly lower over the week, with the contract slipping around 0.7% w-o-w from $2,448/t (RMB 17,017/t) on 26 January to $2,431/t (RMB 16,899/t) on 30 January. While smelter maintenance provided some supply-side support, muted spot demand and a largely neutral SHFE-LME arbitrage environment weighed on sentiment.

Market updates

- MaxVolt launches ReEarth recycling arm: India-based MaxVolt Energy launched MaxVolt ReEarth, a dedicated lithium battery recycling platform focused on end-of-life battery processing, black mass recovery, and critical mineral extraction. The initiative supports India’s EV ecosystem and reinforces the shift toward a circular battery economy through closed-loop recycling solutions.

- Ampyr Australia signs recycling pact: AMPYR Australia entered a partnership with Renewable Metals to trial recycling of end-of-life lithium batteries at a demonstration facility in Western Australia. The agreement supports AMPYR’s plan to deploy 6,000 MWh of BESS capacity by 2030, with Renewable Metals’ process claiming recovery rates of up to 95% for critical minerals, including copper and manganese.

Outlook

LME lead prices are expected to remain largely stable with a bearish bias, pressured by weak demand signals and broader macro uncertainty, despite ongoing inventory drawdowns. The $2,000-2,050/t range for three-month contracts remains a key support zone. A clearer recovery would require stronger battery restocking activity and further visible declines in exchange inventories.

In India, lead prices are likely to continue tracking global trends, with currency movements, recycling activity, and battery demand acting as the primary swing factors.

Leave a Reply