- Mid-week rally fades after testing $1,990/t

- MCX prices edge higher; open interest builds

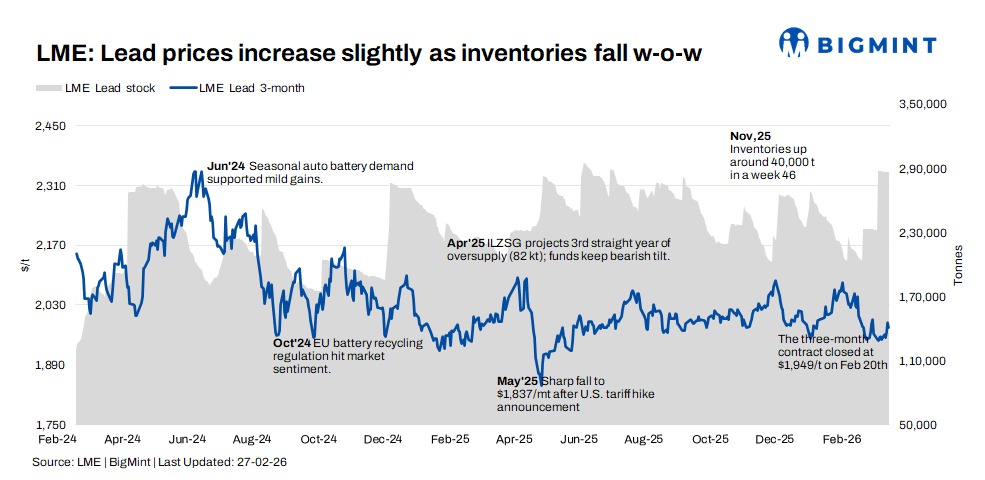

Lead prices on the London Metal Exchange (LME) trended higher in the week ended 27 February, supported by a mid-week rally before easing toward the close. While prices briefly strengthened toward the $1,990/t mark in the three-month contract, late profit-taking capped further upside.

Price trends

LME cash lead opened at $1,911/t on 23 February and dipped to a weekly low of $1,903/t on 24 February before rallying to a weekly high of $1,944/t on 26 February. Prices subsequently eased to close at $1,928/t on 27 February, marking a modest w-o-w gain.

The three-month contract followed a similar trajectory, rising from $1,960/t at the start of the week to a weekly high of $1,989/t on 26 February, before settling at $1,977/t on 27 February. The contract once again approached but failed to sustain momentum beyond the psychologically significant $2,000/t resistance level.

The price action indicates cautious optimism, with buying interest emerging on dips but selling pressure intensifying near the upper end of the recent range.

Inventory analysis

LME lead stocks remained broadly stable during the week, edging lower to 286,100 t on 27 February from 286,325 t at the start of the week, reflecting a modest 225 t drawdown.

The marginal inventory decline contrasts with the sharp build seen in the prior week and suggests stabilising visible supply conditions. However, the absence of a significant draw limits the strength of the bullish narrative, keeping the market balanced.

Unless a sustained stock decline emerges, inventory levels may continue to act as a moderating factor on price rallies.

SHFE lead trends

On the Shanghai Futures Exchange (SHFE), lead prices firmed gradually during the week, rising from $2,377/t on 23 February to $2,399/t by 27 February.

The steady upward movement in the Shanghai market provided supportive cross-exchange cues, although gains remained measured and did not trigger aggressive arbitrage-driven flows.

Post-holiday inventory digestion by lead-acid battery manufacturers reduced spot procurement early in the week. Subdued downstream demand from the automotive replacement battery segment kept refined lead offtake weak. However, primary and secondary smelters restarted operations gradually, improving sentiment in the latter half of the week, while battery manufacturing units resumed production, supporting expectations of demand recovery.

MCX price movements

On the Multi Commodity Exchange of India (MCX), the March 2026 lead contract traded within an INR 187,650-190,200/t range during the week.

Prices closed at INR 189,550/t on 27 February, higher compared with INR 188,600/t on 23 February. Open interest rose from 405 lots at the start of the week to 544 lots by week-end, indicating fresh long build-up alongside the price uptick.

A weaker INR against the USD increased the landed cost of imported lead and lifted global reference prices in domestic currency terms, adding upward pressure on MCX lead. Volumes improved mid-week but remained moderate overall, reflecting selective domestic participation aligned with firm global cues.

Outlook

Lead is likely to trade within the $1,900-2,000/t range in the near term. While stable inventories remove immediate bearish pressure, the contract’s repeated failure to decisively breach $2,000/t suggests persistent overhead resistance.

The pace of downstream demand recovery in China and currency movements in India will remain key variables. Until clearer signals emerge, prices may continue to oscillate within the established range, with dips attracting buying interest and rallies facing selling near resistance.

Leave a Reply