- Prices fall below key $2,000/t level as bearish sentiment dominates

- LME stocks continue to decline; SHFE volatility reflects mixed Chinese market signals

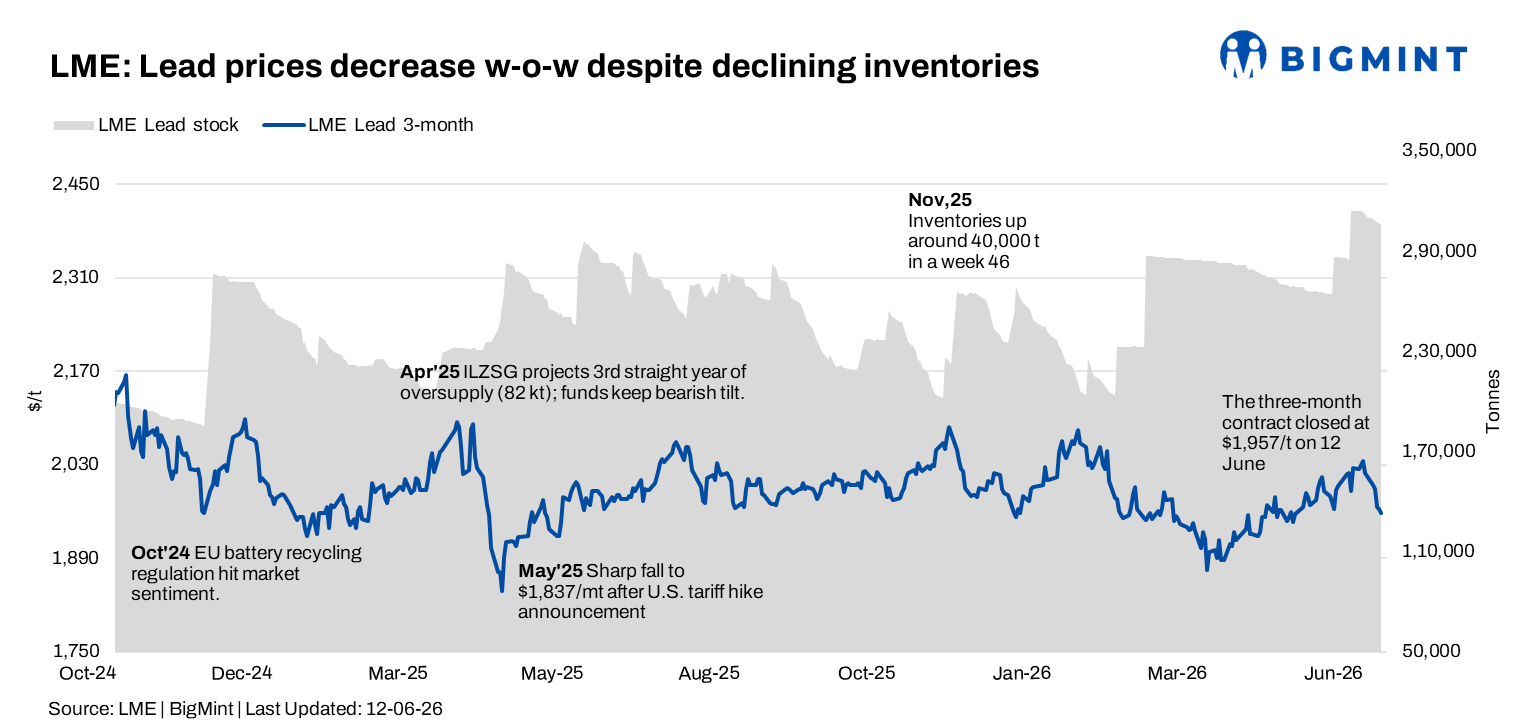

Lead prices on the London Metal Exchange (LME) weakened further during the week ended 12 June 2026, extending losses from the previous reporting period as selling pressure intensified across the base metals complex. The market slipped below the psychological $2,000/t threshold, weighed down by cautious industrial demand and broader risk-off sentiment.

However, continued declines in LME warehouse inventories helped cushion downside pressure, suggesting ongoing material outflows despite softer market fundamentals.

Price trends

The LME three-month lead contract opened the week at $1,999/t on 8 June and remained under pressure throughout the reporting period. Prices briefly recovered to $1,994/t on 9 June but failed to sustain gains, gradually easing to settle at $1,957/t on 12 June, the lowest level of the week.

LME cash lead prices followed a similar trajectory. Cash settlement values declined from $1,990/t on 8 June to $1,957/t on 12 June, reflecting persistent weakness in spot market sentiment.

On a w-o-w basis, the three-month contract fell by $56/t from $2,013/t recorded on 5 June, while cash prices declined by $46/t from $2,003/t over the same period.

The breach of the key $2,000/t support level indicates deteriorating near-term momentum. Immediate resistance is now seen around $1,990-2,000/t, while fresh support is emerging near $1,940-1,950/t.

Inventory analysis

LME lead inventories continued their downward trend during the week, providing a supportive counterbalance to falling prices.

Stocks declined steadily from 309,250 t on 8 June to 308,050 t on 9 June, 307,225 t on 10 June, 306,650 t on 11 June, and further to 305,875 t on 12 June.

Overall, exchange inventories fell by 4,475 t during the week, extending the drawdown seen in the previous reporting period.

The sustained inventory decline suggests ongoing warehouse outflows and relatively balanced physical supply conditions. Nevertheless, inventories remain elevated by historical standards, limiting the bullish impact of stock reductions on overall market sentiment.

SHFE lead trends

On the Shanghai Futures Exchange (SHFE), lead prices displayed mixed performance during the week.

SHFE lead prices eased from $2,354/t on 8 June to $2,346/t on 10 June before rebounding sharply to $2,389/t on 11 June. However, prices retreated significantly to $2,248/t on 12 June, indicating heightened volatility in the Chinese market.

The sharp decline at the end of the week suggests cautious sentiment among Chinese participants despite generally stable domestic demand conditions.

MCX price movements

On the Multi Commodity Exchange (MCX), lead futures traded lower in line with global market weakness.

The June 2026 lead contract opened at INR 207/kg on 8 June and touched a weekly high of INR 207.05/kg on the same day. Prices subsequently trended lower, reaching a weekly low of INR 203.25/kg on both 11 and 12 June before settling at INR 205.05/kg on 12 June.

On a w-o-w basis, the contract declined by INR 1.60/kg from INR 206.65/kg recorded on 5 June.

Open interest increased from 412 lots on 8 June to 424 lots on 12 June, although it peaked at 471 lots on 11 June before moderating. The rise in open interest during periods of falling prices suggests fresh short positions entered the market, reflecting bearish sentiment among participants.

Trading volumes remained moderate, indicating cautious participation as traders assessed the market’s ability to hold above the INR 203/kg support zone.

Outlook

Lead prices are expected to remain under pressure in the near term after slipping below the important $2,000/t level. While declining LME inventories continue to provide underlying support, weak price performance suggests market participants remain cautious amid subdued demand conditions and broader macroeconomic uncertainty.

The extent to which inventories continue to tighten will remain a key factor to watch. Any further stock drawdowns could help stabilize prices, though stronger demand-side signals will likely be required for a meaningful recovery.

Immediate resistance is seen around $1,990-2,000/t, followed by $2,020/t, while support is expected near $1,940-1,950/t. The overall market tone has shifted to neutral-to-bearish, with inventory declines currently insufficient to offset prevailing selling pressure.

Leave a Reply