- Lead inventories rise more than 40,000 t in week

- MCX prices slide despite firm domestic demand

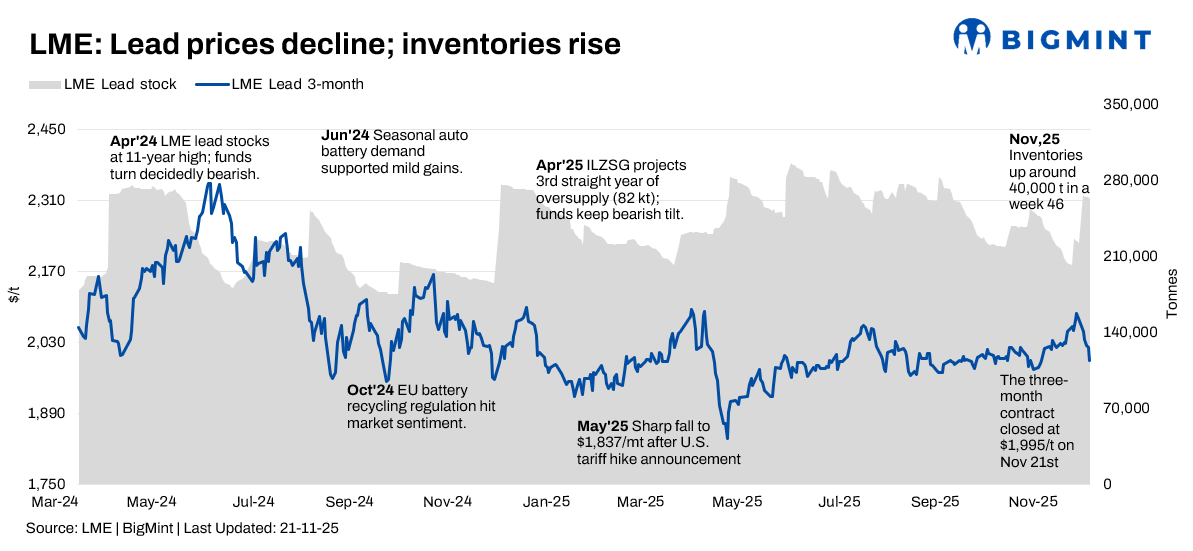

The lead market experienced a downward trend during Week 46 (17-21 November), driven by a sharp surge in LME inventories and rising concerns over US monetary policy. Although domestic demand in India offered some temporary support, LME lead prices, which opened the week on a firmer note, fell steadily as the week progressed.

Price trends

LME lead cash-settlement prices trended lower for most sessions, marked by noticeable daily fluctuations. The week opened at $2,024/t on 17 November and moved down towards a weekly low of $1,980/t before closing at $1,977/t on 21 November, representing a w-o-w decline of approximately 2.3%. The three-month LME lead contract followed a similar trajectory and finished at $1,995/t, reflecting an almost 3% drop for the week. The sharp surge of more than 40,000 t in LME inventories significantly pressured market sentiment. This unexpected rise in stocks overshadowed previous tightness and contributed to the consistent downward price movement.

Inventory analysis

LME lead inventories rose substantially through the week, reaching 262,850 t on November 21. This increase was the primary bearish driver during the period, signalling a loosening in near-term supply availability at a time when the market had been expecting tighter conditions. The sudden growth in inventories, coupled with continued uncertainty over the US Federal Reserve’s rate-cut trajectory, added to the pressure on lead prices across the LME complex.

MCX lead trends

MCX lead prices tracked global weakness while also responding to domestic fundamentals. The MCX lead November contract closed at INR 182,250/t on 17 November and eased to INR 180,850/t by 21 November, reflecting a decline of 0.76%. Early in the week, domestic prices were influenced by the stronger LME lead trend, but as global weakness intensified, the Indian market also witnessed some profit booking. Despite the decline, MCX prices remained relatively stable due to ongoing interest from downstream consumers and the influence of rupee movements.

SHFE lead trend

On the Shanghai Futures Exchange, lead prices also weakened. During the week from 14 November to 21 November, the SHFE 2512 lead contract fell RMB 505/t or about 2.86% to RMB 17,165/t from RMB 17,670/t. The decline reflected subdued downstream demand, rising social inventories, and a generally bearish technical set-up. Prices opened near RMB 17,140/t on 21 November and closed slightly higher intraday, but overall sentiment remained weak.

IESA urges reforms to boost India’s battery recycling

The India Energy Storage Alliance (IESA) has appealed to the government to simplify regulations, incentivise innovation, and promote industry-policymaker collaboration to build a circular battery economy. With the market projected to more than double from $554 million in 2024 to $1.3 billion by 2033, IESA says reforms are vital to address feedstock constraints and accelerate sustainable growth.

Outlook

The near-term outlook for the lead market remains cautiously bearish. The sharp rise in LME inventories, ongoing macroeconomic uncertainty, and soft demand conditions in major consuming regions, particularly China, are expected to keep prices under pressure. Inventory movements, US monetary policy direction, and downstream consumption trends are expected to provide clearer guidance heading into the coming weeks.

Leave a Reply