- Chinese smelters resume output, LME stocks increase

- Long-term outlook stays bullish on tight supply and big investments like the Adani-Caravel deal.

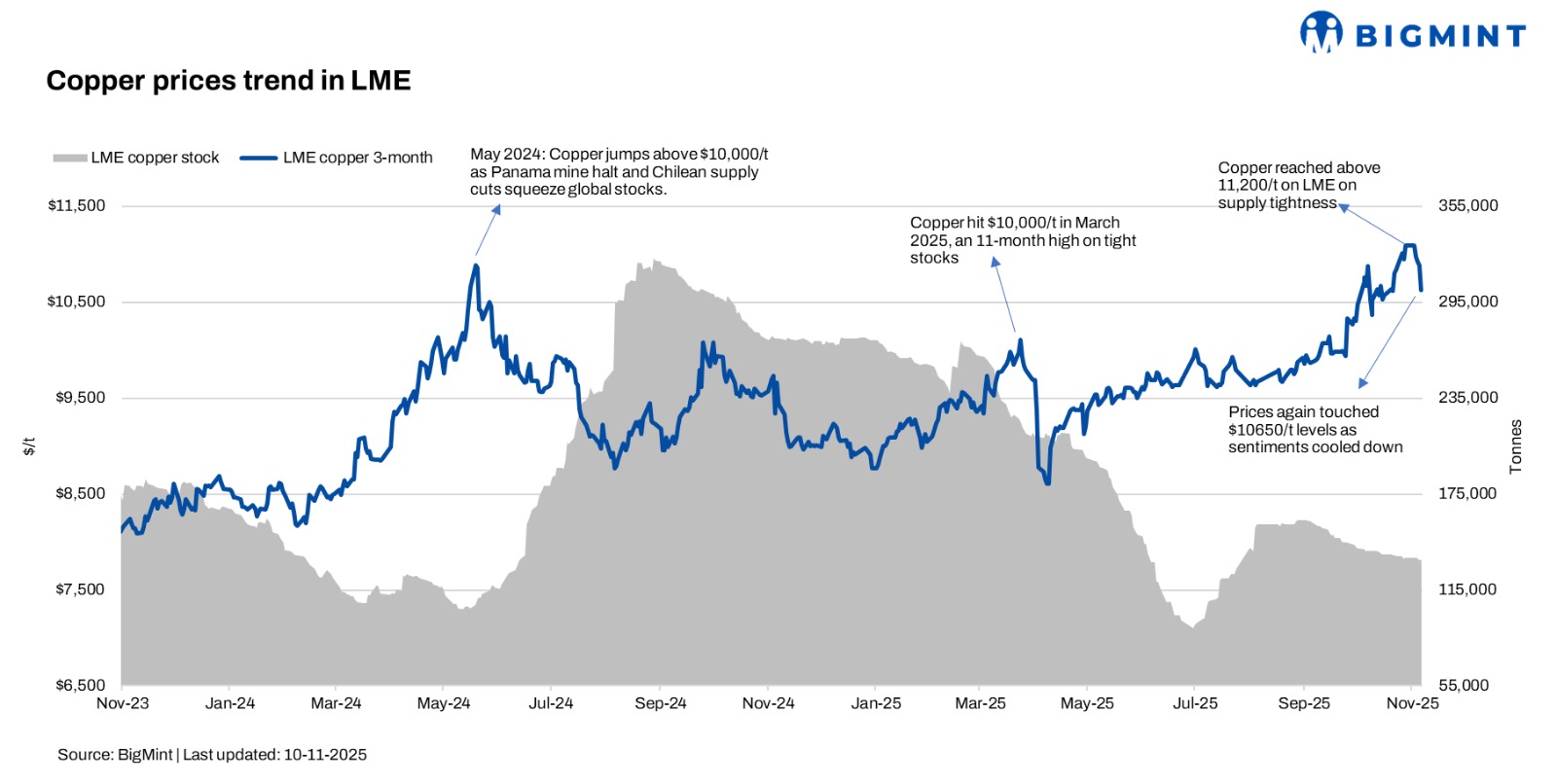

Global copper prices have softened this week, slipping from around $10,920/tonne (t) on the London Metal Exchange (LME) to nearly $10,720/t, as the market saw a round of profit-booking, a firmer US dollar, and softer spot demand from China. After a strong rally driven by mine disruptions and tightening inventories, traders are now reassessing whether the recent surge was overstretched in the near term.

Market scenario

A major driver behind the correction is profit-taking by funds and physical traders. Copper rallied sharply through October on mine issues in Chile, Indonesia, and Panama, and falling LME inventories. With prices close to multi-month highs, short-term players have locked in gains, creating downward pressure. Meanwhile, a modest recovery in the US dollar — on expectations of delayed rate cuts — made commodities costlier for non-US buyers, prompting further selling.

Chinese consumption indicators were also mixed. While structural demand remains strong, spot buying of cathodes and rods has not increased at the same pace as futures, leading to temporary demand fatigue. Some Chinese smelters resuming operations post-maintenance also eased immediate supply concerns.

However, sentiment around the long-term copper outlook remains bullish, supported by tight raw-material supply, declining TC/RCs, and major investments in smelting and refining. A key example is the recent Adani-Caravel Minerals deal, under which Kutch Copper will gain long-term access to 62,000-71,000 t of copper concentrate annually for its 0.5 mnt smelter in Gujarat. Such strategic tie-ups signal that producers expect structurally tight copper markets and are securing feedstock to protect themselves from spot-market volatility and high import premiums.

Outlook

While near-term prices have corrected, the broader market narrative remains unchanged – global inventories are low, mine supply is constrained, and long-term demand from EVs, renewables, grid expansion, and data centres continues to rise. Many analysts expect copper to stabilise and remain firm through Q4, as fundamentals still point to an undersupplied market.

Leave a Reply