- Concentrate tightness strengthens copper market fundamentals

- Weak China demand, surplus expectations restrict sharper gains

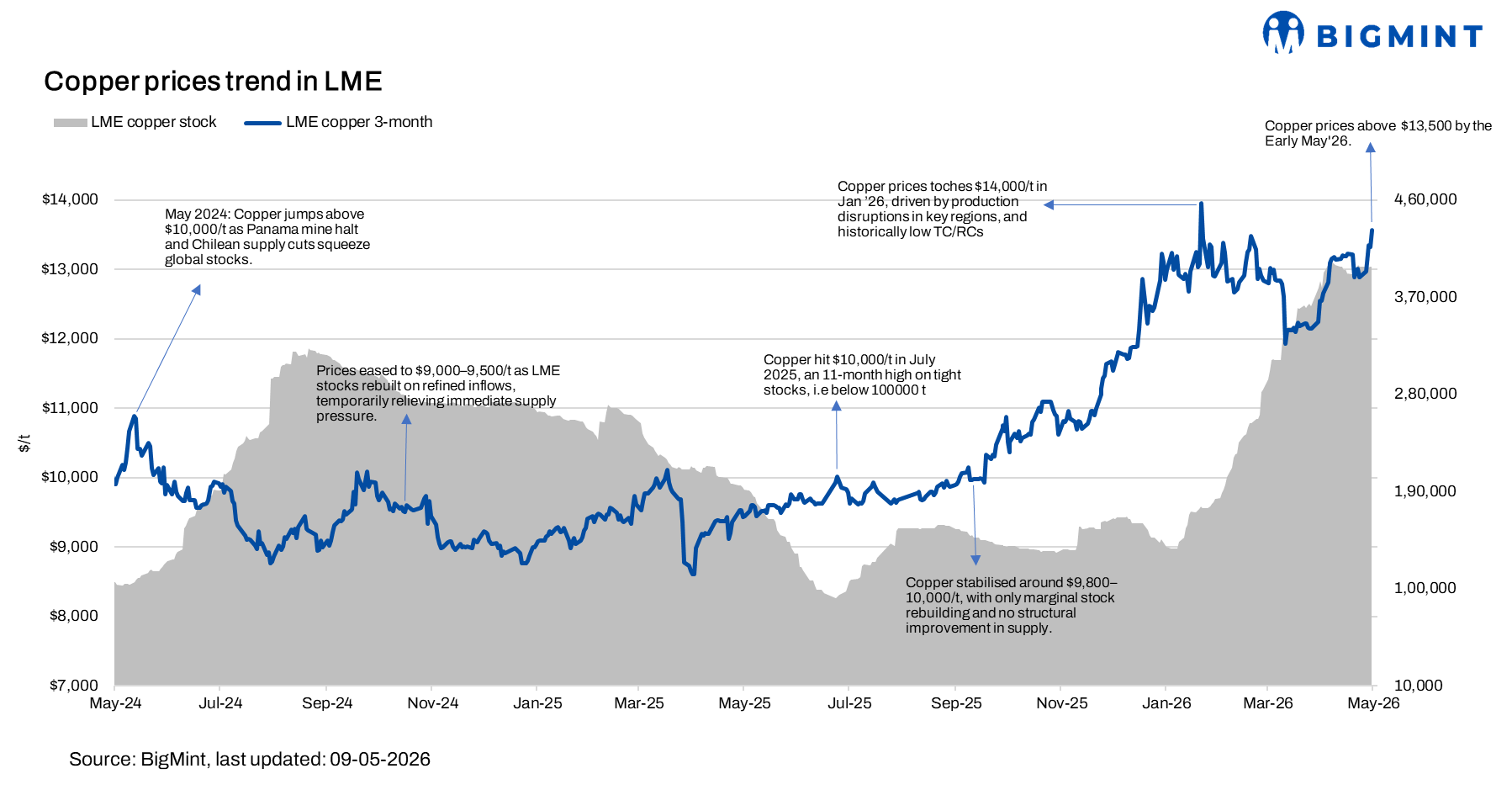

Copper prices on the London Metal Exchange (LME) increased by about $678/t (5.26%) to $13,573/t in the week ended 8 May 2026 from $12,895/t a week ago, reflecting firm market sentiment amid continued supply-side concerns and sustained buying interest despite marginally higher exchange inventories.

Prices remained volatile through the week, supported by continued supply-side concerns and geopolitical uncertainty despite cautious downstream demand in China. Tight copper concentrate availability and persistent disruptions across key producing regions continued to support prices, although surplus expectations and subdued spot buying limited stronger upside momentum.

However, upside gains remained capped by weak consumption signals from China, where strong refined output and cautious buying activity during the Labour Day holiday period reflected subdued underlying demand. Expectations of continued refined market surplus also weighed on overall sentiment.

At the same time, geopolitical tensions surrounding the United States and Iran and continued uncertainty around the Strait of Hormuz supported the market by raising concerns over disruptions in sulphur and raw material supply chains, which kept sulphuric acid costs elevated.

Additionally, tightness in the concentrate market, reflected in continued pressure on treatment and refining charges (TC/RCs) amid constrained mine supply and operational disruptions, provided underlying support to copper prices despite intermittent corrections.

Overall, supply-side risks and geopolitical concerns continued to underpin copper prices, while weak downstream demand and refined market surplus expectations restricted sharper upside during the week.

Japan update

Japan’s refined copper production remained weak in FY’25, with output declining by 7.6% y-o-y to 1.43 mnt, while shipments fell 6% to 1.34 mnt amid subdued electric wire demand and lower exports. Output dropped below 1.5 mnt for the first time in 14 years due to production cuts at some smelters following deteriorating raw material procurement conditions.

On the demand side, weak downstream consumption and lower export shipments continued to weigh on overall market activity, although March 2026 witnessed a marginal recovery in production and shipments after six months of decline. Overall, sluggish demand conditions and procurement-related pressures kept Japan’s copper sector under pressure during FY’25.

India update

India’s copper scrap market remained firm w-o-w, supported by tight inflows and elevated overseas premiums amid limited scrap availability. Supply constraints persisted due to restricted arrivals from key exporting regions and continued diversion of quality material to Far East markets, while higher replacement costs further supported domestic offers.

On the imports side, EU-origin brass honey scrap into Mundra was heard around 60.5% of 3M LME, but higher replacement costs and cautious buying at elevated levels limited fresh bookings. Overall, tight scrap availability, firm overseas offers, and elevated domestic prices kept market sentiment supported

Outlook

Copper’s outlook remains finely balanced, with market direction expected to depend on whether supply-side risks or weak downstream demand intensify further. Tight concentrate availability, continued pressure on TC/RCs, and geopolitical uncertainty are likely to keep underlying market sentiment supported.

However, subdued consumption trends in China, cautious spot buying, and expectations of continued refined market surplus may restrict sharper upside momentum. As a result, copper prices are expected to remain volatile within a narrow range in the near term.

Leave a Reply