- Robust long-term demand outlook drives up prices

- Prices remain elevated despite slight drop mid-week

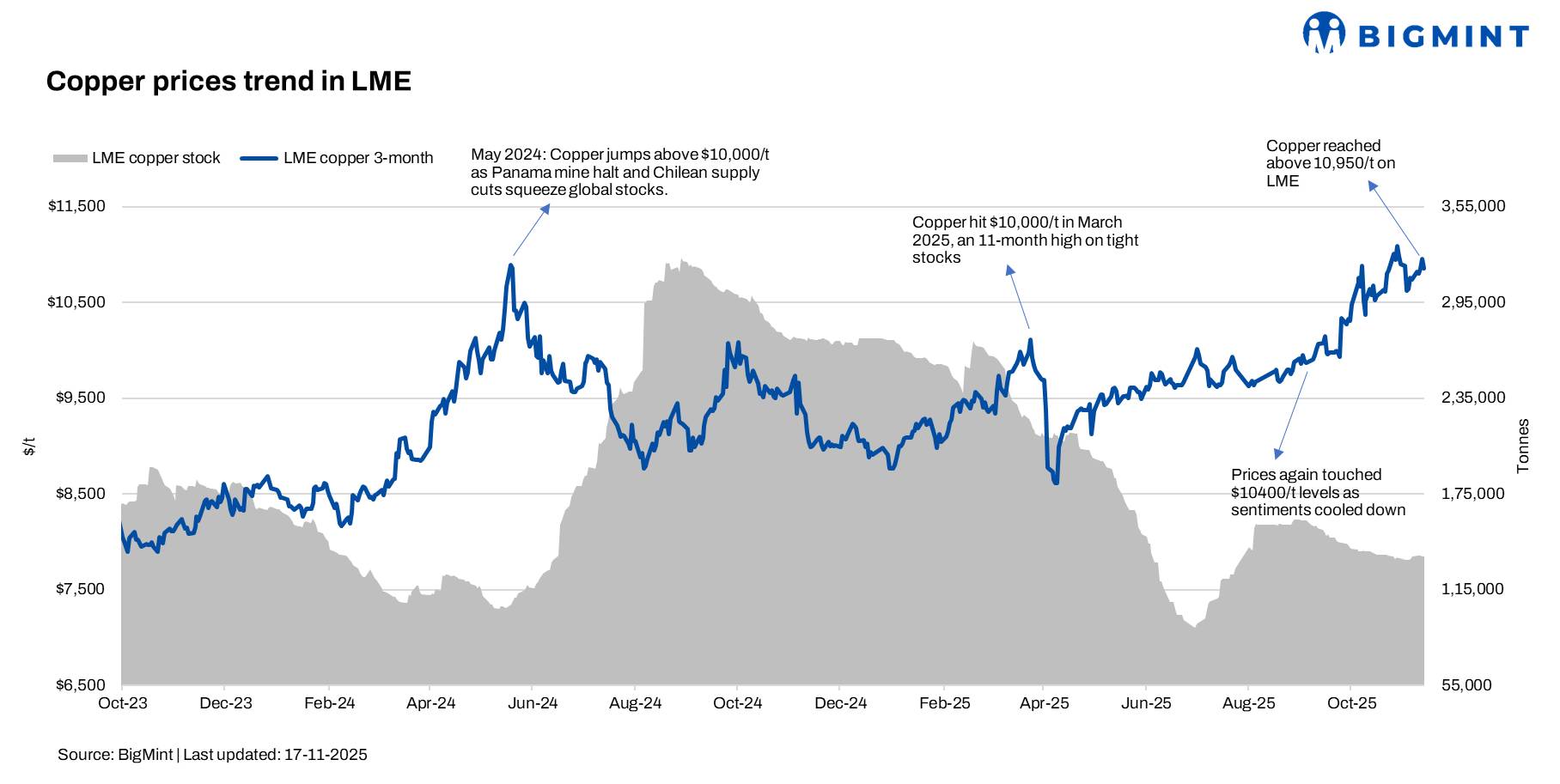

Copper prices on the London Metal Exchange (LME) increased last week, gaining from around $10,745/t on 7 November to nearly $10,855/t on 14 November amid constrained material availability. However, prices on 14 November were lower than the $10,959/t recorded on 13 November, as softer economic signals from China and reduced expectations of an immediate US Fed rate cut pressured sentiment. Major financial outlets noted that the pullback follows copper’s recent multi-month highs, with traders turning cautious amid weaker demand cues and broader market risk-off mood.

Market scenario

Overall, copper prices increased through the week, supported by tight supply conditions and expectations of a global refined copper deficit in 2026. LME cash values also firmed up, as buying interest improved around long-term demand themes such as power grid expansion, renewable energy projects, and electric-vehicle manufacturing. Supply challenges — including reduced concentrate availability and intermittent disruptions at key South American mines — continued to lend support.

Momentum shifted on 14 November, with copper falling from Thursday’s high of $10,959/t, as renewed doubts over a December US Fed rate cut led to a stronger dollar and a broad pullback across base metals. Comments from Federal Reserve officials signalling continued inflation concerns reduced expectations of near-term policy easing, pushing traders to scale back risk. At the same time, soft economic indicators from China — including slower factory output, muted retail activity and rising SHFE inventories — added pressure by highlighting weak physical demand. Despite the dip, prices remain elevated compared to earlier months, reflecting an overall tighter supply backdrop.

Outlook

Copper prices are expected to stay firm but volatile in the near term. The broader trend remains supported by tightening mine supply, steady demand from power infrastructure and EV sectors, and expectations of a refined copper deficit in 2026. However, upside momentum may be limited by weak Chinese economic data, soft physical demand, and continued uncertainty around the US Fed’s rate-cut timeline. If the dollar stays strong and China’s recovery remains slow, prices may face short-term pressure, but the medium-term outlook stays constructive with the market likely to remain tight into early 2026.

Leave a Reply