- Global copper output expected to grow 2.5% in 2025

- Chinese Spot TC/RCs plunge on concentrate shortages

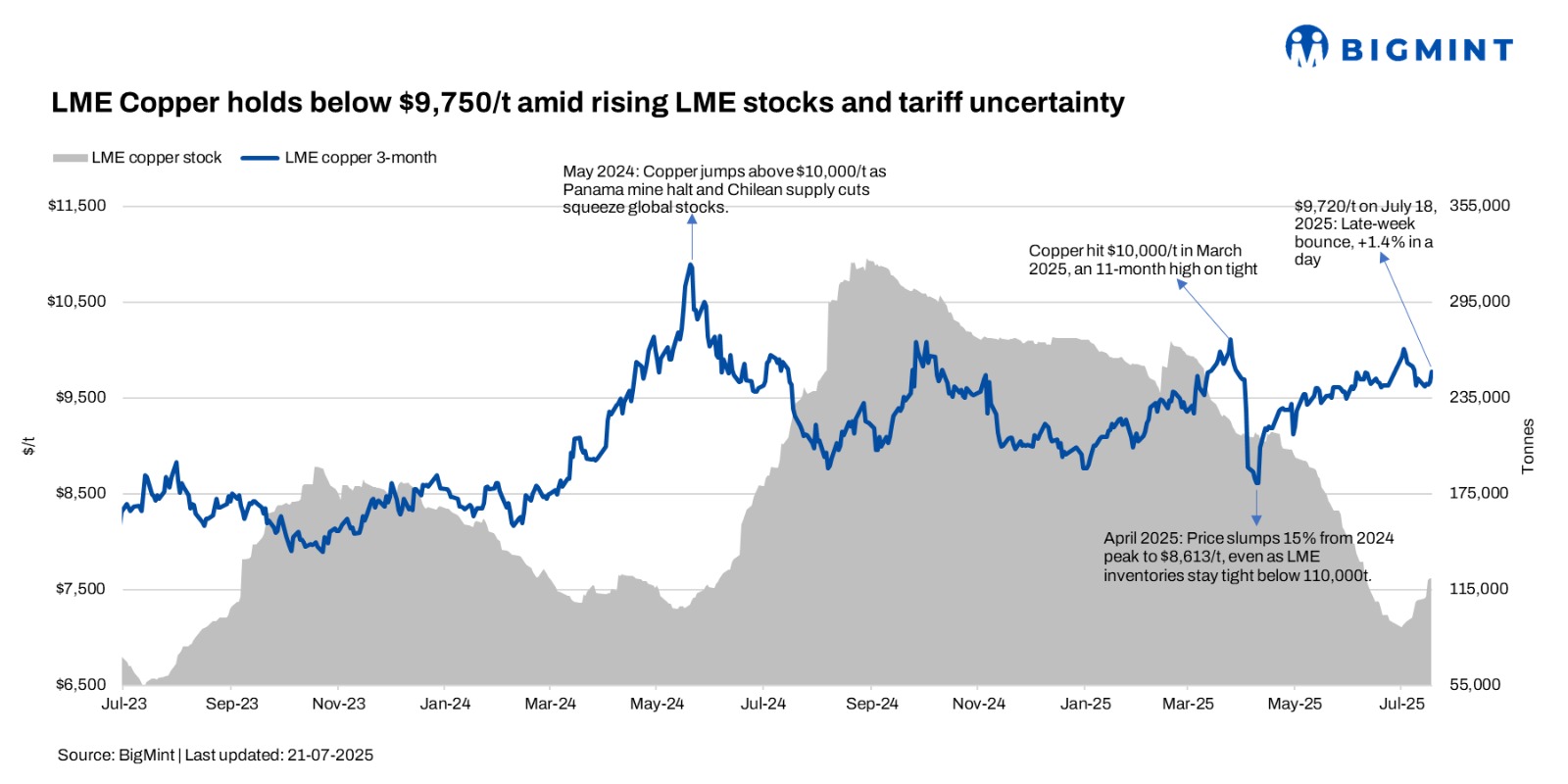

Copper prices on the London Metal Exchange (LME) slipped 0.6% w-o-w, with the 3-month contract settling around $9,670/tonne (t). This decline was driven by a combination of macroeconomic uncertainties, shifting speculative positions, and evolving market fundamentals.

LME inventories climb up but remain below recent highs

LME copper inventories posted a strong 12.4% w-o-w rise to 122,175 t on 18 July from 108,725 t in the previous week. While this build-up helped ease immediate supply tightness, it remains well below the levels seen earlier this year. In May 2025, stocks frequently surpassed 170,000 t and even hit over 200,000 t in the spring, indicating that current levels are not at multi-year highs.

Tariff uncertainty clouds outlook

Market sentiment remains cautious, partly due to the impending US copper import tariffs expected in early August. The tariff has disrupted trade flows, with buyers alternating between stockpiling and holding back. This uncertainty, coupled with weak industrial signals from China and other macroeconomic headwinds, has led many market participants to adopt a defensive stance. Additionally, profit-taking and reduced fund positioning have contributed to the softer tone.

Long-term fundamentals still supportive

Despite the short-term bearish undertone, long-term fundamentals remain constructive. Continued growth in green energy, electric vehicles, and global infrastructure is expected to boost copper demand in the coming years. For now, however, near-term volatility is likely to persist until there is more clarity on trade policy, economic trends, and stock levels.

Mine output expands globally

Copper mine production is on a stronger growth trajectory compared to recent years. According to the International Copper Study Group, global output is expected to grow 2.5% in 2025, building on a 2% rise during January-April. Key drivers include project ramp-ups in Peru, Chile, the Democratic Republic of the Congo (notably Kamoa-Kakula), and Mongolia’s Oyu Tolgoi. In the first four months, Peru’s production rose 5% y-o-y, while combined output from China and the DRC increased 4.8%. India and other Asian producers outside China also reported gains of around 3.5%.

Spot TC/RCs under pressure

Although exact recent spot Treatment and Refining Charges (TC/RCs) have not been disclosed, market reports suggest that Chinese smelters have accepted near-zero or even negative spot TC offers. The sharp drop reflects ongoing concentrate shortages and fierce competition among smelters, which are now operating under significant margin pressure due to the tight global supply environment.

Leave a Reply