- Record SHFE trading volumes, weak US dollar contribute to price gains

- One-hour LME trading disruption on Friday drags copper down sharply

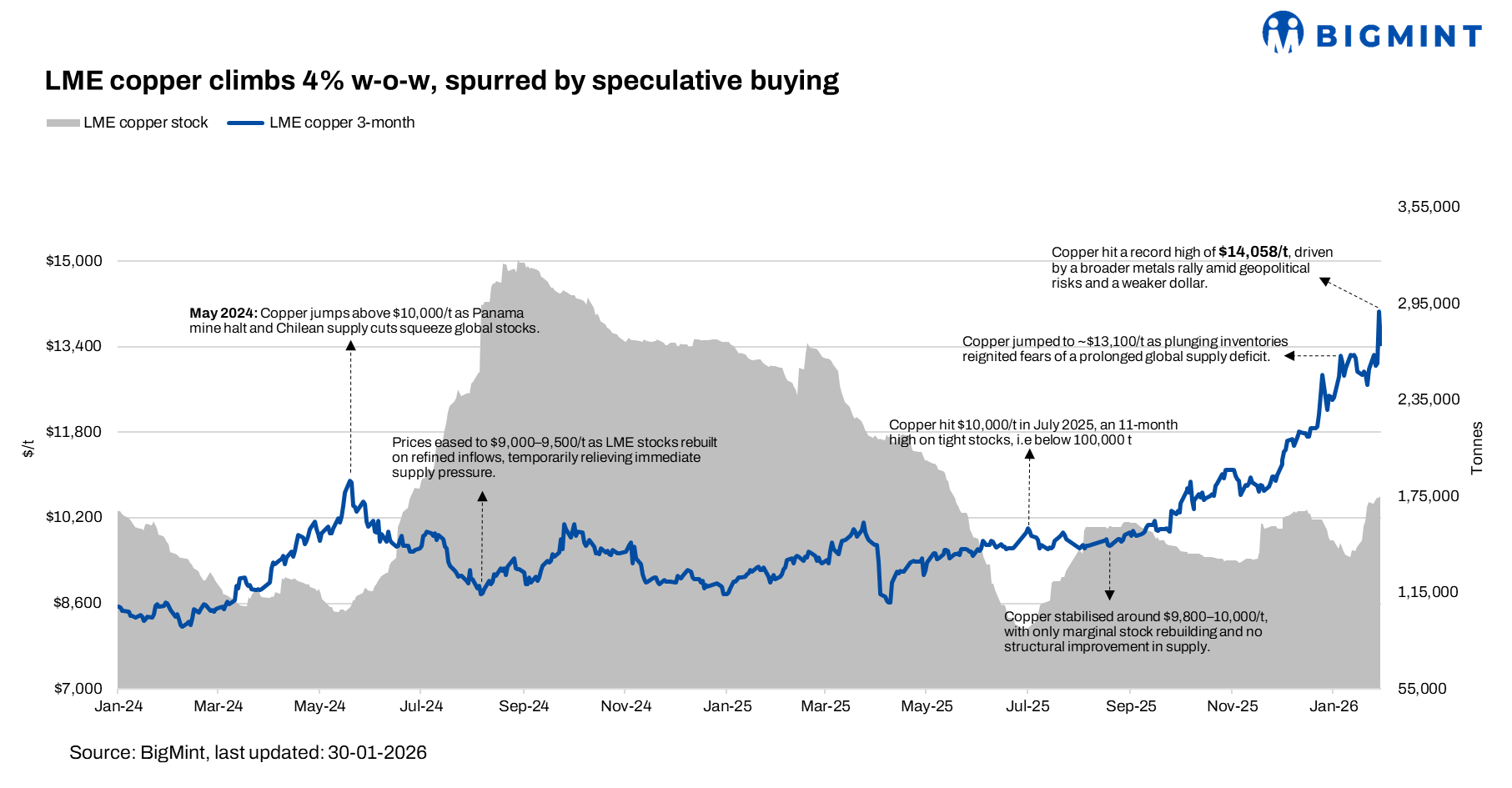

LME copper prices rose sharply by 4% w-o-w in the week ending 30 January 2026, briefly hitting record highs on 29 January. The gains extended a broader metals rally, driven by investors flocking to physical assets amid heightened geopolitical risks and a persistently weak US dollar.

Pricing, inventory trends

LME copper prices averaged $13,377/t in the week ended 30 January, up $506/t or 4% w-o-w. Prices opened the week at around $13,250/t and strengthened mid-week, reaching $14,058/t, and closed the week at $13,445/t.

Meanwhile, LME copper inventories witnessed an 8% inflow, reaching at 173,140 t w-o-w from 160,615 t in week 4.

Factors impacting prices

Copper prices surged this week, briefly surpassing $14,000/t before retreating to around $13,800/t amid profit-taking and broader metals market corrections. The rally was driven largely by speculative buying in China, supported by demand from AI infrastructure, EVs, data centres, and power projects. Goldman Sachs warned of a potential Q2 reversal due to US trade policy while highlighting elevated price levels and ongoing supply-demand imbalances. Weekly gains were also bolstered by record SHFE trading volumes, a weak US dollar, and geopolitical tensions, even as physical demand in China remained soft, with the Yangshan premium at $20/t — the lowest since July 2024.

Volatility spiked further after a one-hour LME trading disruption on Friday, sending copper down to near $13,000/t post-resumption and underscoring fragile market conditions amid rapid intraday swings.

Outlook

Copper prices are expected to remain supported near current levels in the near term, underpinned by tight global supply, robust demand from AI, EVs, and power projects, and ongoing geopolitical tensions. Volatility may persist due to speculative flows, weak US dollar dynamics, and potential policy-driven market corrections.

Leave a Reply