- High inventories, strong output, dollar strength pile pressure on prices

- Tight concentrate supply, demand recovery may support prices

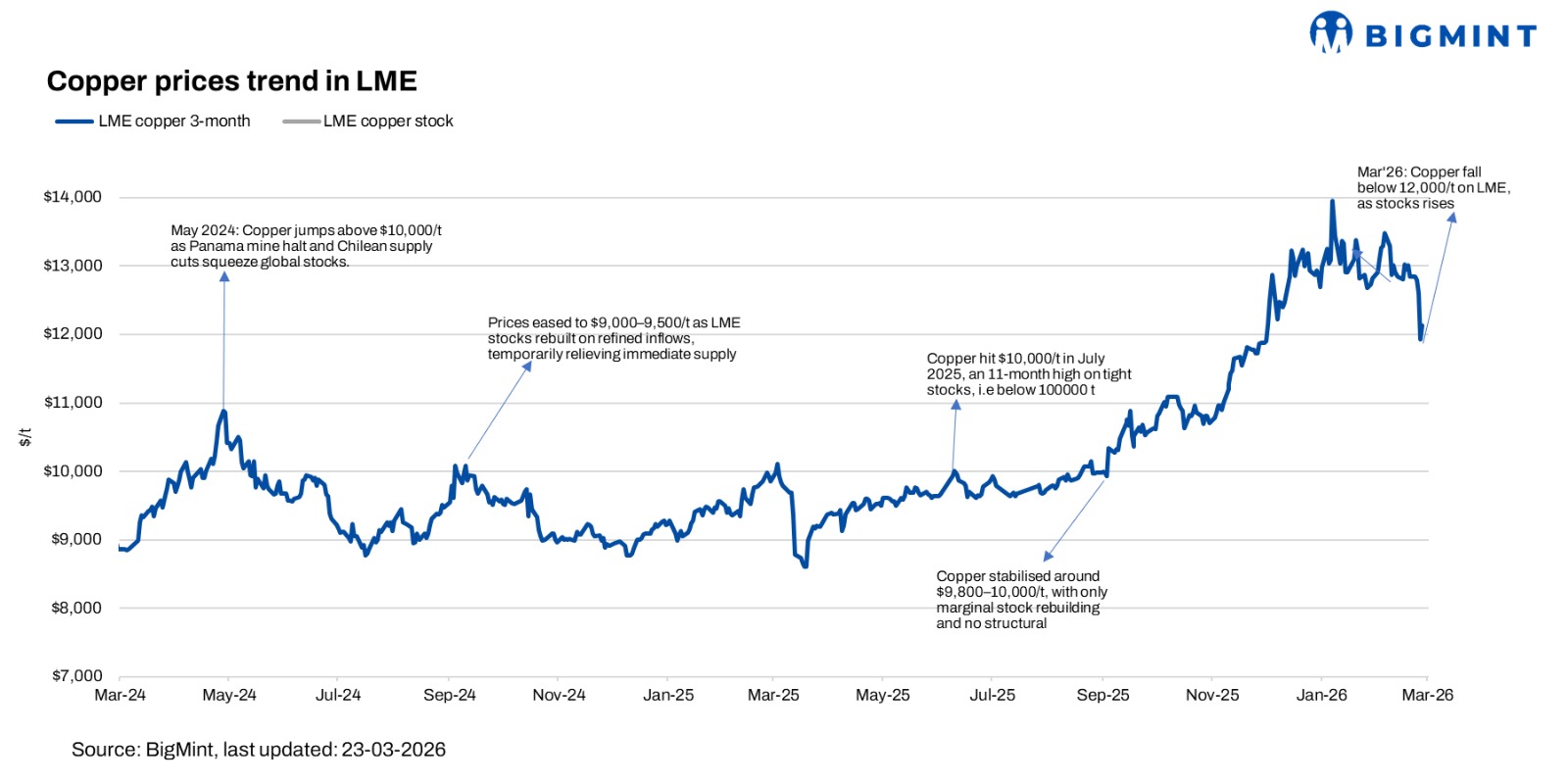

Copper prices on the London Metal Exchange (LME) witnessed a sharp correction over the past week, with the three-month contract falling by nearly $1,000/t w-o-w to settle at $11,930/t on 20 March, compared to around $12,900/t on 13 March. The decline reflects a mix of macro pressure and weakening physical fundamentals.

A key driver was the strengthening US dollar, supported by firm economic data and expectations of higher interest rates for longer. A stronger dollar makes copper more expensive for buyers using other currencies, which reduces both investment flows and physical buying interest, especially from price-sensitive markets.

On the supply side, LME copper inventories rose sharply w-o-w, increasing by over 40,000-50,000 t and crossing the 300,000-t mark. This rise indicates improved material availability in the market, easing earlier tightness and reducing urgency among buyers.

Demand from China remained relatively subdued, with slower offtake from key downstream sectors such as wire and cable. At the same time, higher refined copper exports from China have added additional supply into the global market, as domestic production continues to outpace consumption.

China’s refined copper production hits record high

China’s refined copper production surged to nearly 15 mnt in 2025, up sharply from ~13.6 mnt in 2024, marking a record high. What makes this rise particularly significant is that it occurred amid severe copper concentrate shortages and historically low TC/RCs, indicating that smelters expanded output despite deteriorating processing economics.

This reflects the capacity-led nature of China’s copper industry, where production decisions are increasingly driven by installed smelting capacity rather than raw material availability. The aggressive ramp-up highlights the strategic importance of maintaining output levels, even under margin pressure, to retain global dominance.

Outlook

Copper prices on the LME are expected to remain rangebound with a slight bearish bias in the near term. Elevated inventories and strong refined output, particularly from China, will keep supply comfortable. A firm US dollar may continue to cap upside by limiting buying interest. However, ongoing tightness in concentrate supply could prevent a sharp downside. Any recovery in Chinese demand or restocking activity may provide support, but near-term sentiment remains cautious.

Overall, the price correction was driven by a combination of stronger dollar pressure, rising exchange inventories, and soft downstream demand, which together weakened market sentiment and pushed copper prices lower during the week.

Leave a Reply