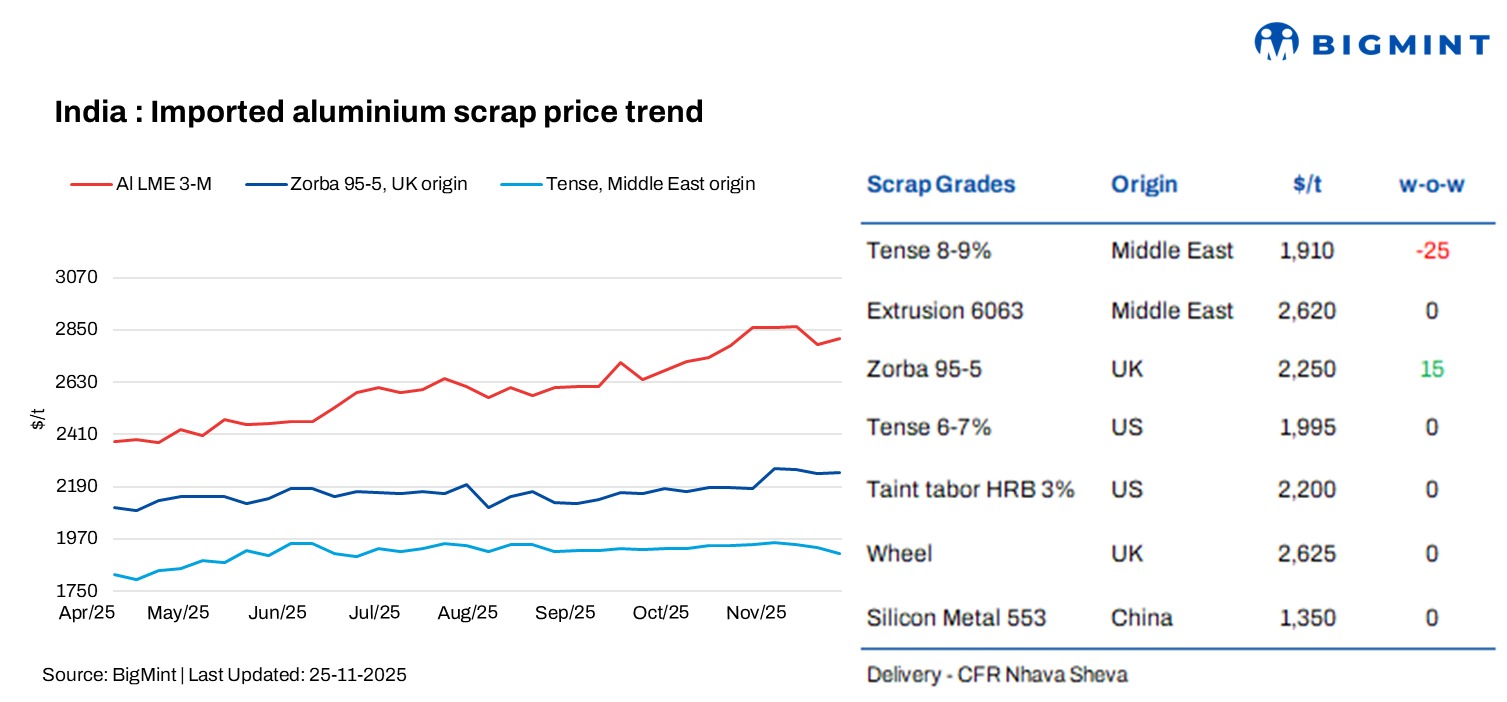

India’s imported aluminium scrap prices remain rangebound w-o-w, following minimal movements on the London Metal Exchange (LME). BigMint assessed UAE-origin Tense scrap at $1,910/tonne (t), down by $25/t w-o-w, while UK-origin Taint Tabor C/S (9-10%) stood at $2,010/t, stable w-o-w.

UK-origin Zorba 95/5 stood at $2,245/t w-o-w, stable, while UAE Extrusion 6063 decreased by $5/t to 2,640/t w-o-w. Meanwhile, UK-origin Wheel rangbebound at $2,625/t w-o-w.

LME prices increase w-o-w; inventories rose

At closing on 25 November, LME aluminium prices stood at $2,815/t, up by $50/t from $2,739/t recorded on 18 November. Meanwhile, aluminium inventories at registered LME-warehouses increased by 3,950 t to 548,025 t from 544,075 t in the previous week, indicating easing supply concerns.

How did India’s aluminium scrap imports move m-o-m?

India’s aluminium scrap imports saw only a minimal m-o-m change, indicating a steady and stable flow of material. Imports in September stood at 196,700 t, while October recorded 201,500 t, reflecting a mild increase of just 2.4%. Market participants note that this small uptick shows neither a strong surge nor a meaningful slowdown, suggesting that buying patterns remained largely consistent, with no major shifts in global pricing or domestic demand affecting volumes during the period.

Market Sentiments

India’s imported aluminium scrap market remains subdued, with muted buying interest as strong global scrap prices and a rangebound LME trend keep sentiment cautious. Domestic scrap prices remain largely flat, creating a clear disconnect between domestic and international levels. This bid–offer mismatch is prompting many buyers to delay fresh bookings, leading to thin trading across major ports.

Market participants highlight weak demand, with buyers restricting purchases to minimum quantities across key grades such as Tense, Zorba, and TT. Although some deals are happening, they remain low in volume, reflecting an overall risk-off tone. Sellers have also diverted Zorba shipments to Thailand, where buying interest and realizations currently appear stronger.

A source mentioned “Tense and TT scrap saw low buying activity this week as importers stayed cautious amid steady global offers. A market participant shared that buyers are only taking small trial lots, avoiding big bookings. US-origin TT remains preferred for its cleaner quality, but sellers aren’t reducing prices. Overall, trades stayed limited with only a few containers moving at stable but firm levels”.

Additionally, Twitch scrap (a high-quality aluminium scrap grade recovered from shredders (mainly automobile scrap) availability remained tight this week, especially from the UAE, as Japanese smelters secured more material for their December production plans. A market participant shared that Middle East exporters are holding very limited stocks, with increasing volumes being diverted to Japan and South Korea due to stronger buying interest. As a result, offers into India have reduced significantly, and even higher bids from Indian buyers are being rejected. Overall, the Twitch market is expected to stay tight until early December unless fresh arrivals improve.

On the other hand, semi-finished alloy demand-especially ADC12-remains firm, supported by the automotive sector. This has limited downside pressure on domestic prices but has not translated into higher imported scrap buying.

China Silicon

According to BigMint’s assessment, China’s 553-grade silicon prices remained stable at $1,350/t CFR Mundra.

As per reports, China’s silicon exports fell sharply in October, weighed down by comfortable spot inventories and slower demand from downstream sectors. According to customs data, China exported 45,073 t of silicon (Si 99.99% max) in October, marking a 30.8% decline y-o-y and a 35.8% drop m-o-m.

Market participants noted that weaker consumption from the aluminium alloy and polysilicon sectors, combined with sufficient domestic supply, encouraged overseas buyers to defer purchases. Many international consumers had already replenished stocks during August–September and were in no rush to build inventories again in October. As a result, export activity slowed significantly, keeping sentiment subdued through the month.

Outlook

Imported aluminium scrap prices are expected to remain rangebound in the near term, as weak buying interest and steady global offers keep the market cautious. Although overall demand is subdued and buyers are resisting higher imported values, auto-linked grades such as ADC12 and related casting scraps could see stronger momentum, supported by firm enquiries from die-casting and automotive manufacturers. Unless global prices soften meaningfully or domestic levels adjust upward, most grades will likely continue to trade in a tight, sideways band, with only the auto segment showing clearer strength.

Leave a Reply