- Africa’s aluminium output falls after Mozal smelter shutdown

- India seeks US waiver extension for continued Russian oil imports

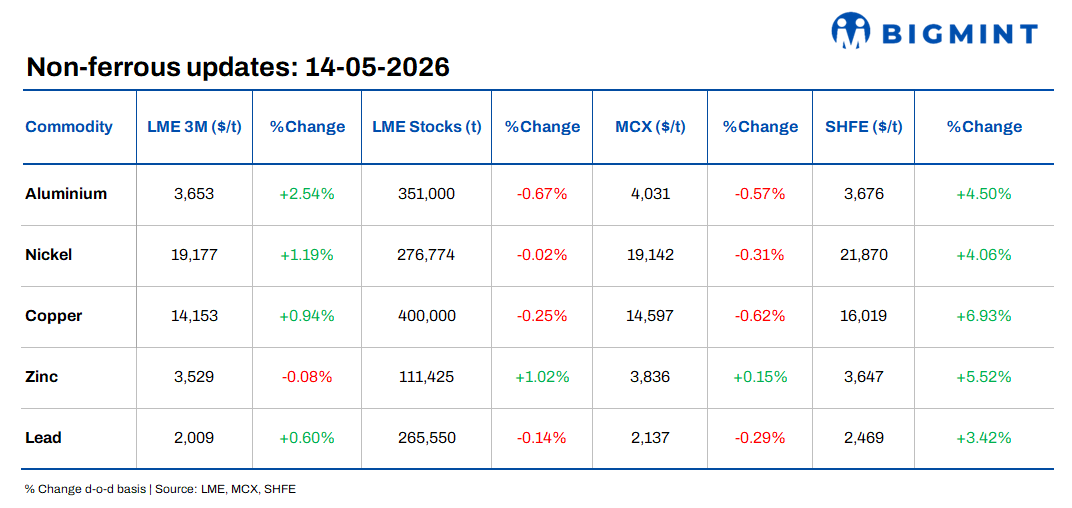

Base metals prices on the London Metal Exchange (LME) traded higher on 13 May 2026, with gains in aluminium, nickel, copper and lead, while zinc edged marginally lower. Aluminium recorded the strongest increase among major metals, rising 2.54% to $3,653/t, followed by nickel, which gained 1.19% to $19,177/t. Copper increased 0.94% to $14,153/t, while lead rose 0.60% to $2,009/t. Meanwhile, zinc marginally declined by 0.08% to $3,529/t. The broader non-ferrous complex remained supported amid firm global market sentiment.

On the inventory side, LME stocks largely trended lower across major metals. Aluminium inventories declined 0.67% to 351,000 t, lead stocks fell 0.14% to 265,550 t, and nickel inventories edged lower by 0.02% to 276,774 t. Meanwhile, zinc inventories increased 1.02% to 111,425 t, while copper stocks rose marginally to 400,000 t, indicating balanced near-term supply conditions across the base metals complex.

Domestic market overview

India’s non-ferrous scrap market showed a mixed d-o-d trend. Aluminium tense scrap (loose) prices remained stable, with ex-Delhi prices unchanged at INR 298,000/t and ex-Chennai prices steady at INR 310,000/t amid balanced spot market activity.

Meanwhile, copper armature scrap (Cu 99%), ex-Delhi, increased by INR 25,000/t or 2.1% d-o-d to INR 1,215,000/t from INR 1,190,000/t, supported by stronger global copper prices and elevated replacement costs.

Other market updates

Mozal shutdown exposes Africa’s vulnerability

Africa’s aluminium production declined 6.2% q-o-q to 381,000 t in Q1 2026 from 406,000 t in Q4 2025 following the shutdown of the Mozal aluminium smelter in Mozambique, highlighting the region’s growing vulnerability to power disruptions and concentrated production dependence. Output also fell 3.3% y-o-y from 394,000 t recorded in Q1 2025.

Market participants noted that Africa’s aluminium supply chain remains heavily dependent on South Africa and Mozambique, making regional output increasingly sensitive to electricity shortages, hydro-power disruptions and infrastructure constraints. The Mozal shutdown, linked to unresolved power supply issues and rising energy costs, has intensified concerns over long-term supply stability across the African aluminium sector.

Alba Q1 sales fall 17% amid Gulf shipping disruptions

Aluminium Bahrain (Alba) reported a 17% y-o-y decline in Q1 2026 sales volumes to 312,563 t as the ongoing Middle East conflict and disruptions in the Strait of Hormuz impacted regional shipping and export flows. Net finished aluminium production also declined 14% to 339,734 t after the company temporarily shut nearly 19% of its smelting capacity in March amid escalating regional tensions.

Despite lower production and sales volumes, Alba’s net profit surged 316% y-o-y to BHD 75.3 million ($199.7 million), supported by sharply higher aluminium prices amid tightening global supply conditions. The company stated it continues monitoring alumina inventory levels closely while optimizing raw material usage following ongoing supply chain disruptions across the Gulf region.

India seeks extension of US waiver for Russian oil imports

India has reportedly approached the US administration seeking an extension of the waiver permitting Russian oil imports, as the ongoing Iran conflict continues heightening risks across global energy markets. The request comes amid concerns over potential supply disruptions, tighter crude availability and rising freight and insurance costs linked to escalating geopolitical tensions in the Persian Gulf region.

Market participants believe prolonged instability in the Middle East could further increase volatility in global crude prices, prompting major energy-importing nations such as India to secure alternative supply flexibility to maintain stable domestic energy flows.

Leave a Reply