- China copper output at record highs may ease near-term global supply tightness

- India removes ADD on lithograde aluminium coils (>1150 mm), easing downstream supply

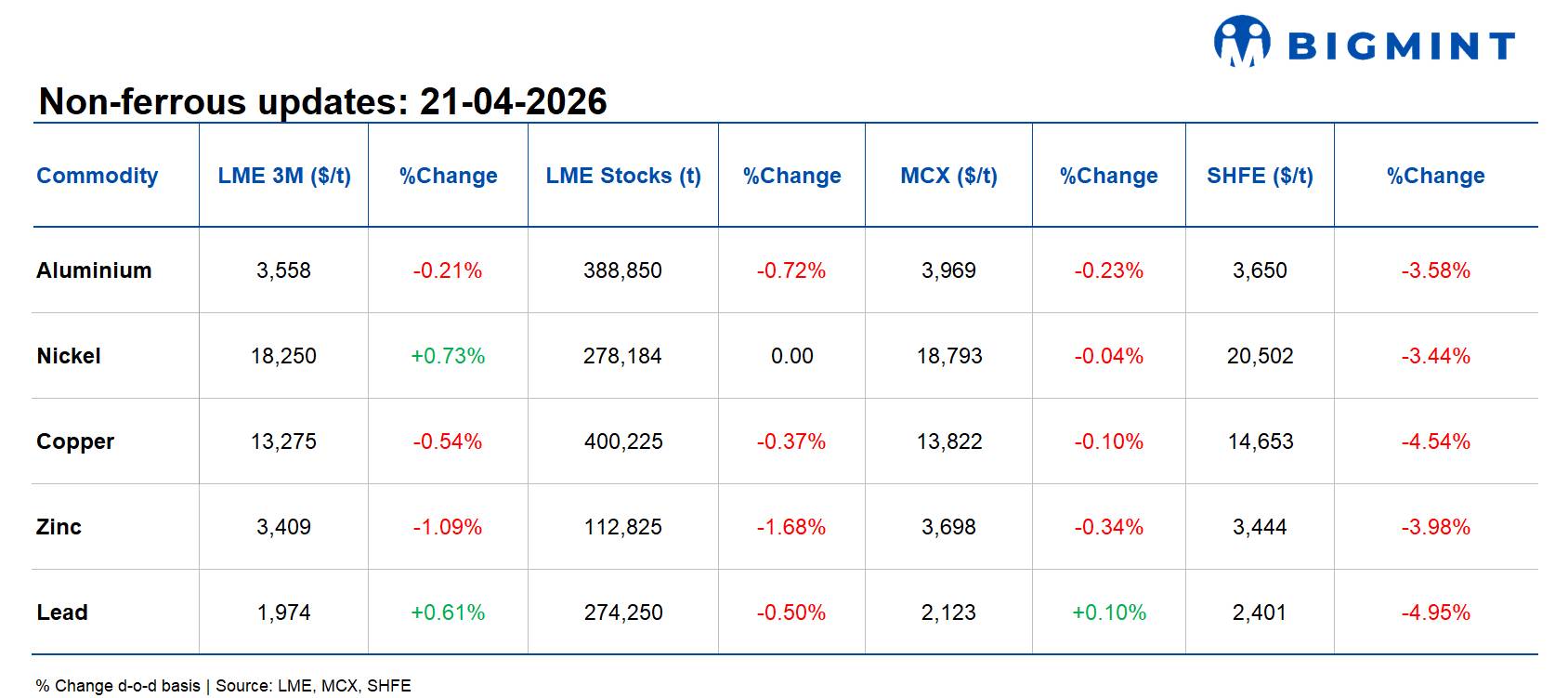

Base metals on the London Metal Exchange (LME) traded mostly lower on a d-o-d basis on 20 April 2026, with declines observed across most key metals, while a few registered modest gains. Zinc recorded the sharpest decline, falling 1.09% to $3,409/t, followed by copper, which slipped 0.54% to $13,275/t, and aluminium, down 0.21% to $3,558/t. In contrast, nickel edged higher by 0.73% to $18,250/t, while lead also increased 0.61% to $1,974/t.

On the inventory side, trends remained largely negative, indicating continued draw-downs across most metals. Zinc inventories recorded the steepest decline, down 1.68% to 112,825 t, followed by aluminium stocks, which fell 0.72% to 388,850 t. Lead inventories declined 0.50% to 274,250 t, while copper stocks eased 0.37% to 400,225 t. Meanwhile, nickel inventories remained unchanged at 278,184 t, indicating stable availability compared to other base metals.

Domestic market overview

India’s non-ferrous scrap markets remained largely stable on a d-o-d basis, with aluminium prices declining while copper also registered a decline. Aluminium tense scrap (loose), ex-Delhi, declined by INR 3,000/t or 1% to INR 287,000/t from the previous level of INR 290,000/t. Similarly, ex-Chennai prices declined by INR 2,000/t or 0.7% to INR 305,000/t from the previous level of INR 307,000/t, indicating balanced market conditions with mild downward price movement.

In contrast, copper armature scrap (Cu 99%), ex-Delhi, declined by INR 1,000/t or 0.1% to INR 1,135,000/t from INR 1,136,000/t, reflecting weaker demand and downward price pressure in the copper segment.

Other market updates

US exports surge, yet fail to replace Middle East oil gap

US crude exports rose to 5.44-5.48 million bpd in April-May 2026, while refined fuel exports touched 3.59 million bpd, supported by supply disruptions after the closure of the Strait of Hormuz, which typically handles nearly 20% of global oil flows.

Exports to Asia increased sharply to 3.29 million bpd in May from 1.11 million bpd in January, but remain insufficient to offset nearly 10 million bpd of earlier Middle East supplies to the region.

Similarly, US refined fuel shipments to Asia rose to 386,000 bpd, still well below the previous 1.58 million bpd, keeping supply pressure elevated across Asian markets.

India removes ADD on lithograde aluminium coils above 1150 mm width

The Government of India has excluded lithograde aluminium coils of width above 1150 mm from the scope of anti-dumping duty (ADD) on certain flat-rolled aluminium products imported from China, through Notification No. 05/2026-Customs (ADD) dated 17 April 2026. The amendment modifies the earlier Notification No. 68/2021-Customs (ADD) following revised findings by the DGTR (Dec 2025) and directions from the Delhi High Court (July 2025).

With this revision, lithograde coils above 1150 mm width will no longer attract anti-dumping duty, effectively narrowing the scope of the duty framework on aluminium flat-rolled imports and potentially easing raw-material availability for downstream users such as offset printing plate manufacturers.

Chile’s faster mining approvals may boost global copper supply outlook

Chile plans to accelerate mining permit approvals to unlock an investment pipeline exceeding $100 billion, a move that could support medium- to long-term global copper supply growth. The government aims to simplify nearly 200 procedures and reduce approval timelines by about 30%, improving project execution visibility.

With over $17 billion worth of mining projects already entering environmental review, faster clearances are expected to ease future supply tightness concerns and improve investor sentiment across the global copper market, particularly amid rising demand from energy transition and infrastructure sectors.

Rio Tinto nears 52-week high on strong Q1 production performance

Shares of Rio Tinto moved closer to their 52-week high after the company reported 9% y-o-y growth in copper-equivalent production in Q1 FY’26, supported by improved output across key assets including Oyu Tolgoi. The performance matched the upper end of market expectations and reinforced confidence in Rio’s diversified growth beyond iron ore.

Higher iron ore sales (72.4 mnt) and rising copper output (229 kt) also supported the positive outlook, highlighting operational resilience despite weather disruptions and ongoing geopolitical supply-chain risks. Strong production momentum is expected to support sentiment across global base-metals markets, particularly copper and aluminium.

China copper output hits record on sulphuric acid support

China’s refined copper output rose to a record 1.33 mnt in March 2026, taking Q1 production to 3.785 mnt, up 9.3% y-o-y, supported by strong earnings from sulphuric acid by-products. Chinese smelters are earning over 5,000 yuan per tonne of copper from sulphuric acid, improving operating margins despite weak treatment charges amid concentrate shortages.

Higher Chinese smelter activity could ease near-term global refined copper supply tightness and moderate price upside. However, output may soften in the coming months due to seasonal maintenance shutdowns, which could partially limit supply-side pressure on the market.

Leave a Reply