- Aluminium scrap prices remain stable in India

- 2025 was copper’s biggest year since 2009

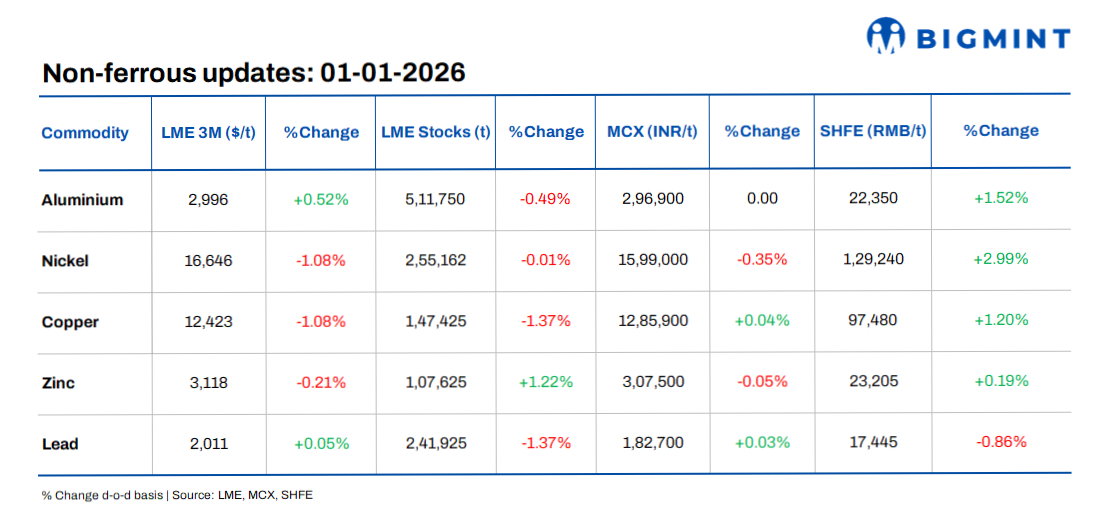

Base metals prices on the London Metal Exchange (LME) were mixed on 31 December, with selective gains and losses across the complex. Aluminium prices edged up 0.52% to $2,996/t, supported by relatively stable sentiment, while lead inched higher by 0.05% to $2,011/t. In contrast, nickel and copper both declined 1.08%, with nickel settling at $16,646/t and copper at $12,423/t, reflecting some profit-taking after recent volatility. Zinc prices also softened slightly, easing 0.21% to $3,118/t.

LME warehouse inventories also showed a divergent trend. Aluminium stocks fell 0.49% to 511,750 t, while copper inventories dropped 1.37% to 147,425 t, signalling continued tightening. Lead stocks declined by 1.37% to 241,925 t, and nickel inventories were broadly stable, edging down 0.01% to 255,162 t. In contrast, zinc stocks rose 1.22% to 107,625 t, pointing to easing availability pressures.

Domestic market overview

In India’s non-ferrous markets, BigMint assessed copper armature scrap at INR 1,110,000/t ex-Delhi, down by INR 50,000/t d-o-d. Meanwhile, aluminium Tense scrap prices remained stable at INR 204,000/t ex-Delhi and at INR 191,000/t ex-Chennai, respectively.

Other updates

Chinalco revises capital contribution structure for joint venture

Aluminum Corporation of China Limited has confirmed the incorporation of Chinalco Qianxing (Chengdu) Technology Co., Ltd. and revised its capital contribution structure, opting to meet its entire commitment in cash instead of partly through high-purity gallium production. The company has so far injected $14 million toward its total pledged contribution of $42 million, while other partners have completed their paid-in capital. The change does not affect the joint venture’s registered capital, equity structure, or contribution schedule and is expected to simplify funding without impacting control or dilution. Analysts continue to maintain a ‘Buy’ rating on the stock with a target price of $1.6/share.

Copper records biggest annual gain since 2009

Copper posted its strongest annual performance since 2009, surging 42% on the LME in 2025 as near-term supply tightness and long-term electrification demand outweighed softer Chinese consumption. Prices hit a record $12,960/t amid year-end buying, driven partly by accelerated shipments to the US ahead of potential 2026 import tariffs, which tightened availability outside the US and concentrated global stocks on COMEX. Supply disruptions at major mines in Indonesia, the DRC and Chile added further strain. While China’s property-led demand remains weak in the near term, long-term fundamentals stay bullish, with global copper consumption projected to rise by over a third by 2035 on clean energy, EV adoption and grid expansion. Copper ended the year at $12,403/t, down 1.1% on the final trading day.

Zinc eases on profit booking after supply-led rally

Zinc prices slipped 0.21% to $3,118/t as profit booking followed a speculative rally driven by supply-tightness concerns, despite fresh mine-side constraints in China that are set to curb zinc concentrate output. Maintenance at mines in central and southwest China is expected to reduce production days and cut metal output by around 700 t, with concentrate supply likely to fall m-o-m. However, weak downstream demand in China, ongoing deterioration in property activity, and a sharp rise in refined zinc output-up 13.3% y-o-y to 654,000 t in November-capped upside. Globally, refined zinc production is projected to rise 2.7% to 13.8 mnt in 2025, while ILZSG data show the market deficit narrowing to 600 t in October, with a 76,000 t surplus recorded over the first 10 months of 2025.

Leave a Reply