- EGA-Sohar deal talks signal consolidation in Gulf aluminium sector

- Falling crude inventories heighten India’s energy security concerns

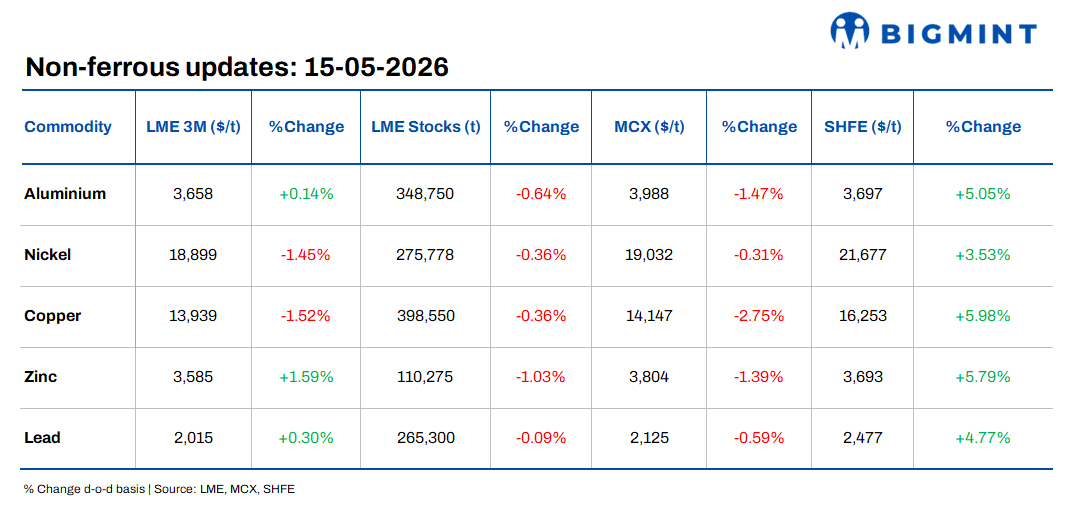

Base metals prices on the London Metal Exchange (LME) showed a mixed trend on 14 May 2026, with gains in zinc, lead, and aluminium offset by declines in copper and nickel. Zinc recorded the strongest gain among major metals, rising 1.59% to $3,585/t, followed by lead, which edged up 0.30% to $2,015/t. Aluminium also increased marginally by 0.14% to $3,658/t, while copper and nickel declined by 1.52% and 1.45% to settle at $13,939/t and $18,899/t, respectively. The overall trend reflected cautious sentiment across the non-ferrous complex.

On the inventory side, LME stocks declined across all major metals, indicating continued drawdowns in exchange inventories. Zinc inventories recorded the sharpest decline, falling 1.03% to 110,275 t, followed by aluminium, which decreased 0.64% to 348,750 t. Copper and nickel stocks slipped 0.36% each to 398,550 t and 275,778 t, respectively, while lead inventories edged down 0.09% to 265,300 t, reflecting relatively balanced near-term supply conditions across the complex.

Domestic market overview

India’s non-ferrous scrap market showed a mixed d-o-d trend. Aluminium tense scrap (loose) prices increased, with ex-Delhi prices rising by INR 6,000/t or 2% to INR 304,000/t and ex-Chennai prices increasing by INR 1,000/t or 0.3% to INR 311,000/t, supported by firm domestic sentiment and improved buying interest.

Meanwhile, copper armature scrap (Cu 99%), ex-Delhi, declined by INR 5,000/t or 0.4% to INR 1,210,000/t, reflecting weaker copper sentiment and cautious downstream buying activity.

Other market updates

Hormuz uncertainty cuts India’s crude oil stocks by 15%

India’s crude oil inventories have declined nearly 15% since the onset of the US-Iran conflict, as uncertainty surrounding the Strait of Hormuz disrupted import flows and tightened domestic supply conditions. Indian refiners continued operating at steady run rates despite lower crude arrivals, accelerating the drawdown in inventories.

The Strait of Hormuz, which handles nearly 20% of global oil trade, remains under heightened geopolitical stress amid tighter maritime controls and reduced shipping activity, increasing energy security concerns for major Asian importers such as India. Persistent supply disruptions and elevated crude prices continue to keep volatility high across global energy markets.

EGA in talks to acquire stake in Sohar aluminium

Emirates Global Aluminium (EGA) is reportedly in advanced discussions to acquire a stake in Oman-based Sohar Aluminium, signalling continued consolidation and strategic expansion across the Gulf aluminium sector. Sources indicated that EGA may take over Abu Dhabi National Energy Co.’s (TAQA) holding in the smelter, further strengthening UAE-Oman industrial integration.

The development comes amid heightened supply concerns and growing focus on securing regional aluminium production capacity following disruptions in Gulf trade flows and ongoing geopolitical tensions around the Strait of Hormuz.

Sulphur squeeze intensifies pressure on Indonesia’s nickel sector

Indonesia’s nickel sector is facing mounting cost pressure amid surging sulphur prices linked to ongoing disruptions around the Strait of Hormuz. Indonesia, which accounts for nearly 60% of global nickel supply, relies heavily on Gulf sulphur imports for HPAL processing used in battery-grade nickel production.

Rising sulphur and sulphuric acid costs, along with stricter ore quotas and higher ore pricing formulas, have significantly pressured smelter economics, forcing some HPAL operators to cut output. The supply squeeze has supported nickel prices, with LME nickel recently touching around $20,000/t amid tightening global supply expectations

Finland’s Arctial smelter targets first aluminium output by H2 2029

Rio Tinto-backed Arctial aims to commence first hot metal production from its planned low-carbon aluminium smelter in Finland in H2 2029, with the project targeting an annual output of around 610,000 t. The project, expected to take a final investment decision in 2027, could increase Europe’s primary aluminium production by nearly 20%.

The development has gained strategic importance amid tightening aluminium availability in Europe following disruptions to Gulf exports through the Strait of Hormuz. Rising regional supply risks and elevated European aluminium premiums continue to strengthen the case for new low-carbon domestic production capacity in Europe.

Leave a Reply