- Aluminium supply crunch deepens amid Middle East disruptions

- China ramps up crude stockpiling despite supply risks

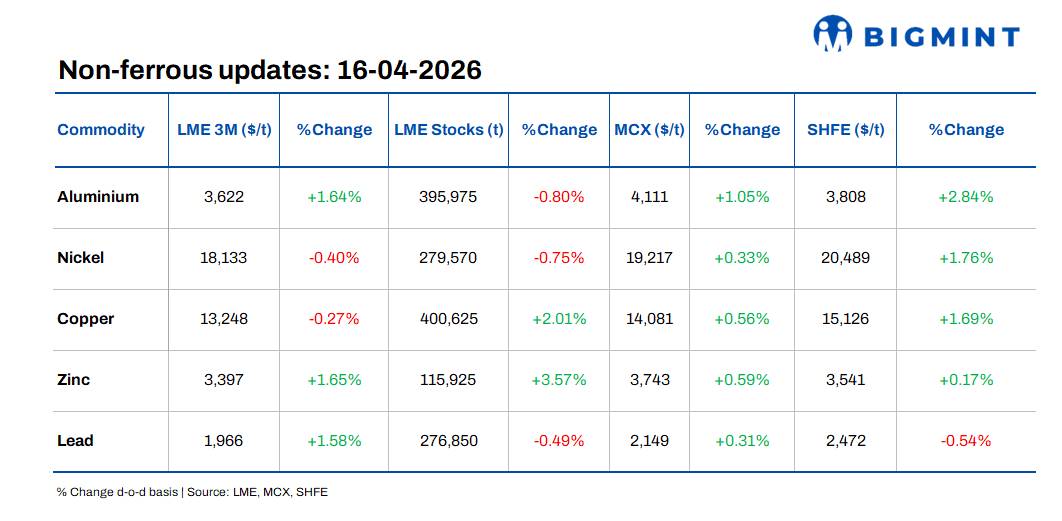

Base metals prices on the London Metal Exchange (LME) traded on a mixed note d-o-d on 15 April 2026, with gains in some metals offset by declines in nickel and copper. Zinc led the upside, rising 1.65% to $3,397/t, followed by aluminium up 1.64% to $3,622/t and lead gaining 1.58% to $1,966/t. In contrast, nickel declined 0.40% to $18,133/t and copper slipped 0.27% to $13,248/t.

Inventory trends were largely on the downside across base metals, indicating tightening availability. Aluminium stocks fell 0.80% to 395,975 t, nickel inventories declined 0.75% to 279,570 t, and lead stocks decreased 0.49% to 276,850 t. Meanwhile, copper inventories rose 2.01% to 400,625 t and zinc stocks increased sharply by 3.57% to 115,925 t, indicating relatively higher exchange availability.

Domestic market overview

India’s non-ferrous scrap market continued to show a firm trend d-o-d, supported by improved buying interest. Aluminium tense scrap (loose), ex-Delhi, increased marginally to INR 289,500/t, up by INR 500/t or 0.2% from INR 289,000/t. Meanwhile, ex-Chennai prices rose sharply to INR 305,000/t, gaining INR 8,000/t or 2.7% from INR 297,000/t, indicating stronger regional demand.

Copper armature scrap (Cu 99%), ex-Delhi, also strengthened to INR 1,150,000/t, up by INR 15,000/t or 1.3% from INR 1,135,000/t, reflecting firm buying activity and improved market sentiment.

Other market updates

Global aluminium supply squeezed by tariffs

The global aluminium market is entering a phase of acute supply tightness, driven by geopolitical tensions in the Middle East, trade tariffs, and energy-related constraints impacting production and logistics.

Disruptions across key Gulf producers and restricted shipping via the Strait of Hormuz have tightened supply chains, with Wood Mackenzie indicating a potential global deficit of up to 4 MnT.

On the exchange front, LME inventories have declined below 400,000 t, highlighting reduced availability, while policy measures such as the US 50% import tariff have further elevated premiums and constrained trade flows.

Market dynamics are increasingly shifting towards physical availability concerns, with near-term supply recovery expected to remain limited amid ongoing geopolitical and structural challenges.

China builds crude stockpiles despite supply risks

China continued to expand its crude oil stockpiles in March, with a surplus of around 1.74 Mn bpd as imports and domestic production outpaced refinery throughput.

Crude imports stood at 11.77 Mn bpd, while domestic output reached 4.49 Mn bpd, exceeding processing demand of 14.52 Mn bpd, indicating continued stockpiling despite global disruptions.

The stock build comes amid Middle East supply risks, with China leveraging its estimated 1.2 Bn barrels of reserves to maintain supply security and cushion potential import disruptions.

However, refined fuel exports are declining sharply, tightening regional supply, while future imports may ease due to geopolitical uncertainties and trade disruptions

Oil steady amid scepticism over US-Iran talks

Oil prices remained largely unchanged, with Brent near $95/bbl and WTI around $91.7/bbl, as markets weighed diplomatic signals against ongoing supply disruptions.

Sentiment remained cautious as investors doubted that renewed US-Iran talks would lead to a swift resolution, given repeated breakdowns in negotiations.

Supply risks continue to dominate, with disruptions in the Strait of Hormuz-handling around 20% of global oil flows-tightening physical markets and keeping prices volatile.

Analysts estimate up to 13 Mn bpd of flows impacted, indicating persistent supply tightness despite diplomatic efforts.

KGHM eyes nearshore copper assets to cut logistics costs

As per reports, Poland-based copper producer KGHM is exploring investments in copper mines across Europe and Morocco to secure raw material supply closer to its smelting operations and reduce logistics costs.

The company has reportedly signed a cooperation agreement with Morocco’s ONHYM and Managem Group and has deployed geologists to assess potential deposits, with initial results expected in the coming weeks.

The move reflects a strategic shift towards supply chain optimisation, with KGHM also evaluating changes in its processing network, including a potential transition of its Legnica smelter towards recycling operations.

Leave a Reply