- Production surges 14% in July ahead of festive season

- ADC12 tags expected to stay rangebound

India’s automobile industry witnessed a mixed performance in July 2025, reflecting varying trends across segments, as per latest data from the Federation of Automobile Dealers Associations (FADA) and the Society of Indian Automobile Manufacturers (SIAM).

Passenger vehicle sales continued to show strong momentum, while two-wheeler sales remained sluggish, highlighting the contrasting demand dynamics in the market. Factors such as festive season stocking, easing supply chains, and rural demand patterns played a crucial role in shaping monthly trends.

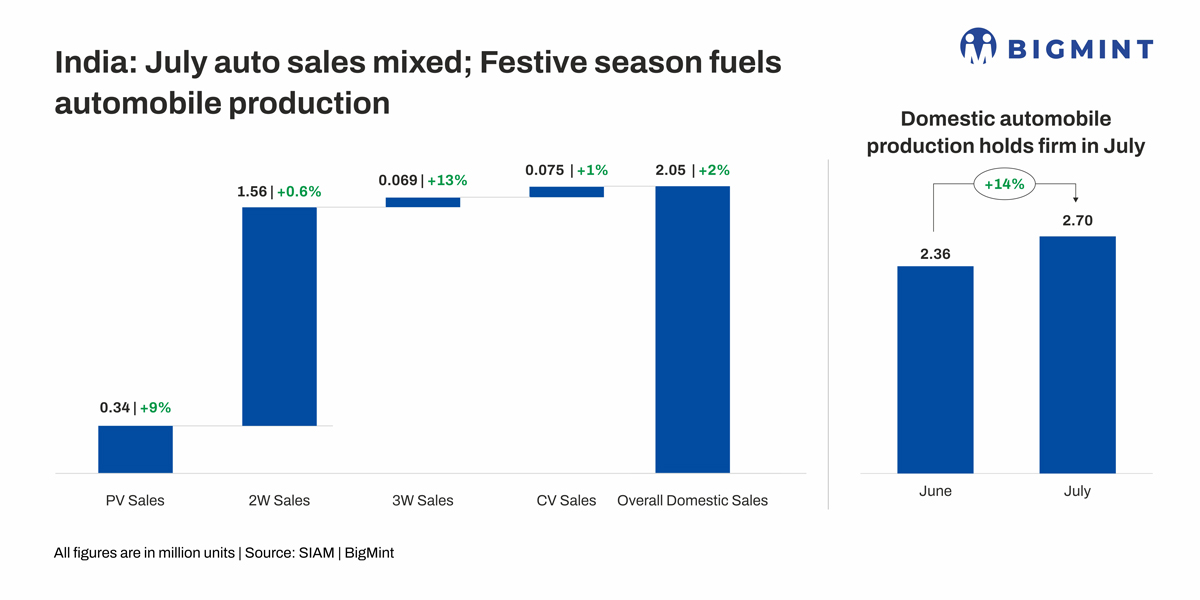

According to FADA’s retail data, passenger vehicle sales rose 10% m-o-m to 3,28,613 units in July, up from 2,97,722 units in June. The segment benefitted from strong urban demand and improved availability of popular models. In contrast, two-wheeler sales slipped 6% m-o-m to 13,55,504 units, reflecting weaker rural sentiment and the impact of erratic monsoon rains.

Three-wheeler sales, however, grew by 11% to 1,11,426 units, supported by rising demand in last-mile connectivity and urban transport. Commercial vehicles posted a mild 2% decline to 79,948 units, while tractors saw healthy growth of 15% to 88,722 units, aided by robust demand from the agricultural sector. Overall retail sales stood at 19,64,213 units, marginally lower by 2% compared to June.

On the wholesale side, SIAM data showed a slightly different picture. Passenger vehicle sales grew 9% m-o-m to 3,40,772 units, aligning with the retail uptrend. Two-wheeler sales inched up 0.5% to 15,67,267 units, indicating that OEM dispatches remained stable despite weak retail traction. Three-wheeler sales recorded a sharp 12.3% increase to 69,403 units, while commercial vehicle sales were largely flat at 75,000 units.

Domestic sales overall rose 2% to 20,52,442 units. Production volumes also surged significantly by 14% to 26,98,519 units in July, as manufacturers ramped up output ahead of the festive season. Inventory levels witnessed a steep rise of 81.5% m-o-m, climbing to 6,46,077 units, indicating a heavy stock build-up at the dealer level.

The divergence between retail and wholesale data highlights the cautious sentiment among customers versus the optimistic stance of manufacturers.

While OEMs pushed higher dispatches in anticipation of festive demand, weak two-wheeler retail sales suggest rural consumption challenges persist. At the same time, steady passenger vehicle demand and the uptick in tractors and three-wheelers provide some relief for the sector. Going forward, industry performance will hinge on monsoon progress, rural income recovery, and festive season demand, with OEMs expected to keep a close eye on inventory build-up.

Impact on aluminium ADC12 alloy

Production has remained steady as manufacturers ramp up operations ahead of the festive season. Demand for ADC12 aluminium ingots, a key material in automotive manufacturing, is expected to stay strong, buoyed by increased festive season activity.

Despite a decline in LME aluminium prices, scrap prices–which are a crucial raw material input–have remained firm. This stability is attributed to a persistent shortage of scrap in the market, preventing any significant price drop.

According to BigMint’s bi-monthly ADC12 assessments for August , prices for ADC12 automobile OEM-grade ingots are currently at INR 230,000/t in Delhi NCR and INR 232,000/t in Chennai, both on 30-day payment terms.

Overall, prices are expected to remain rangebound with no major corrections, as the upcoming festive season is anticipated to boost automobile sales and sustain demand.

Outlook

For August and the remainder of Q2FY’26, industry participants anticipate a gradual recovery in the automobile sector, supported by the upcoming festive season, improved rural incomes following a favourable monsoon, and accommodative monetary policy measures, including recent repo rate cuts. Passenger vehicles are likely to sustain demand, while two-wheelers may witness a modest pickup as rural consumption strengthens.

However, market players have flagged potential production constraints due to export licensing controls from China on rare earth magnets, which could affect electric vehicle (EV) and high-efficiency motor manufacturing.

Leave a Reply