- LME mixed as zinc gains and inventories rise

- Supply recovery builds while macro and geopolitics weigh

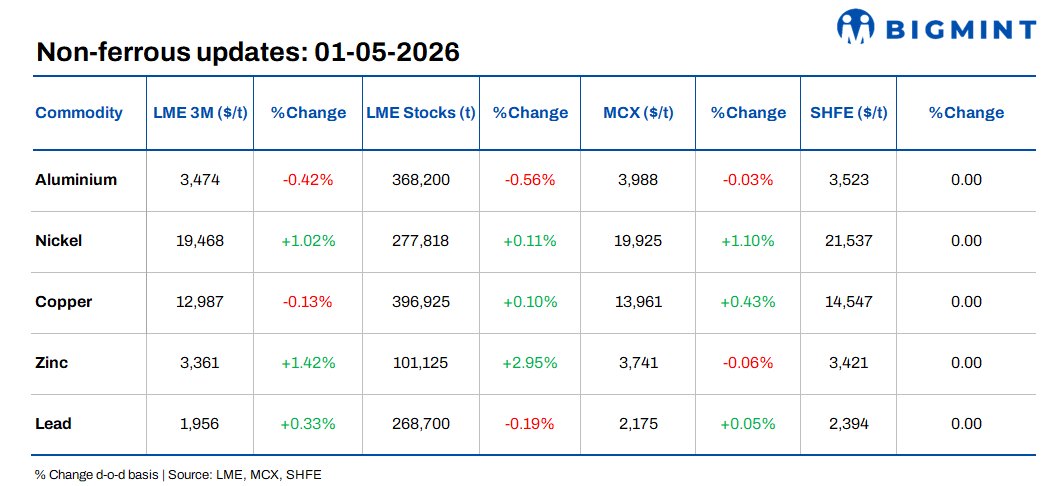

Base metals on the London Metal Exchange (LME) showed a mixed trend on 30 April 2026, with performance varying across commodities. zinc emerged as the strongest gainer, rising 1.42% to $3,361/t, while nickel also posted notable gains of 1.02% to $19,468/t. Lead edged higher by 0.33% to $1,956/t, whereas aluminium and copper declined marginally by 0.42% and 0.13%, settling at $3,474/t and $12,987/t, respectively.

On the inventory front, LME stocks presented a mixed picture. Zinc inventories recorded a sharp increase of 2.95% to 101,125 t, indicating easing supply tightness. Copper stocks rose slightly by 0.10% to 396,925 t, while nickel inventories also edged up by 0.11% to 277,818 t. In contrast, aluminium stocks declined by 0.56% to 368,200 t, and lead inventories fell by 0.19% to 268,700 t, suggesting selective tightening in specific metals.

Domestic market overview

India’s non-ferrous scrap prices remained stable on a day-on-day basis, with no changes observed across key categories. In the aluminium segment, aluminium tense scrap (loose), ex-Delhi, was steady at INR 295,000/t, unchanged from the previous day. Similarly, ex-Chennai prices held firm at INR 308,500/t, reflecting a flat trend in regional markets.

In the copper segment, copper armature scrap (Cu 99%), ex-Delhi, also remained unchanged at INR 1,138,000/t, indicating steady demand-supply conditions with no immediate price movement in the domestic market.

Other market updates

Glencore Q1 copper output rises 19%; marketing arm seen beating guidance

Glencore reported a 19% y-o-y increase in Q1 2026 copper production to 199,600 t, supported by improved ore grades in African operations and higher output at the Antamina mine in Peru.

However, cobalt production declined sharply by 39%, as the company prioritised copper output at its Democratic Republic of Congo assets amid export quota restrictions.

The company maintained its full-year 2026 production guidance, despite operational challenges and mine closures in Australia. Meanwhile, its marketing division is on track to exceed the upper end of its annual EBIT guidance of $2.3-3.5 billion, backed by strong Q1 performance.

Rising input costs (diesel, sulphuric acid) remain a concern, but stronger commodity prices are expected to support margins going forward

Century aluminum resumes output at Iceland smelter

Century Aluminum has restarted production at its Grundartangi smelter in Iceland, restoring supply after months of disruption caused by an electrical equipment failure that had curtailed operations significantly.

The smelter, with an annual capacity of around 320,000 t, had previously operated at reduced levels-cutting nearly two-thirds of output and tightening European aluminium availability.

The restart, achieved earlier than initially expected, is likely to ease near-term supply tightness in the European market and could weigh on regional premiums going forward.

US crude futures rise; volatile amid Iran conflict

US crude futures edged higher, with WTI rising by 41 cents to $105.50/bbl, after earlier hitting an intraday high of $110.93/bbl, reflecting heightened market volatility.

The upward movement comes amid ongoing geopolitical tensions involving Iran, which continue to disrupt global oil flows, particularly through the Strait of Hormuz, a key energy transit route.

Despite a ceasefire earlier in April, uncertainty around diplomatic progress and potential military escalation has kept prices elevated, with both Brent and WTI on track for multiple consecutive monthly gains.

Overall, supply concerns and geopolitical risk premiums remain the primary drivers of oil price volatility in the near term.

Aluminium prices soften on weak macro, pre-holiday demand

Domestic and global aluminium prices declined, weighed down by weak macro sentiment and subdued pre-holiday demand.

Hawkish signals from the US Federal Reserve and geopolitical tensions impacted market confidence, while downstream buyers remained cautious, limiting purchases.

Overall, sluggish demand and macro headwinds kept aluminium prices under pressure in the near term.

Leave a Reply