- Nickel slides on weaker market sentiment

- Macro and supply signals weigh on sentiment

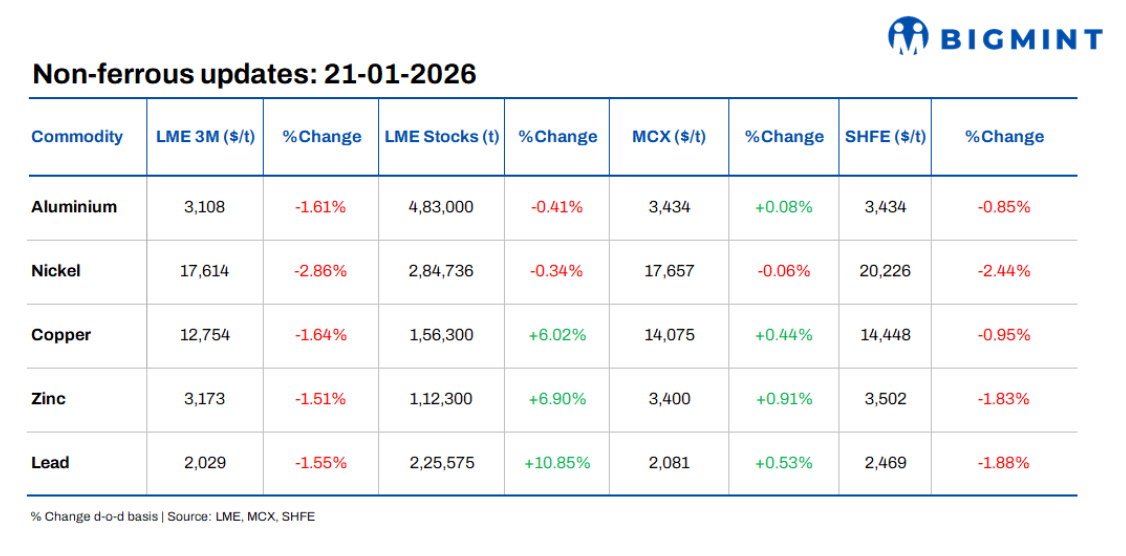

Base metals prices on the London Metal Exchange (LME) retreated on 21 January, with losses seen across the complex. Aluminium prices fell 1.61% to $3,108/t, while LME stocks declined 0.41% to 483,000 t, pointing to continued inventory drawdowns. Nickel also weakened sharply, sliding 2.86% to $17,614/t, as stocks edged down 0.34% to 284,736 t.

Copper prices dropped 1.64% to $12,754/t, accompanied by a sharp 6.02% rise in inventories to 156,300 t, indicating strong inflows at exchange warehouses. Zinc moved lower as well, down 1.51% to $3,173/t, with stocks rising 6.90% to 112,300 t, highlighting improving near-term availability. Lead recorded losses of 1.55%, settling at $2,029/t, while inventories surged 10.85% to 225,575 t, signalling easing supply tightness.

Domestic market overview

In India’s non-ferrous metals markets, aluminium Tense scrap prices were largely range-bound d-o-d. Ex-Delhi assessments held steady at INR 206,000/t, reflecting cautious buying interest, while ex-Chennai prices rose by INR 1,500/t to INR 206,000/t, pointing to relatively firmer regional demand. Meanwhile, copper armature scrap prices, ex-Delhi, fell by INR 7,000/t (down 0.6%) to INR 1,120,000/t, as market participants turned cautious after recent highs.

Other updates

Venezuela’s aluminium revival faces steep hurdles

Venezuela has the resource base to revive its bauxite-alumina-aluminium industry, with large, high-quality bauxite reserves and existing but idle mines, refineries and smelters supported by hydropower. However, years of underinvestment, sanctions, ageing infrastructure and chronic power outages have left key assets largely non-operational. Restarting the sector would require heavy capital investment to modernise facilities and secure reliable electricity, though aluminium’s growing strategic importance could revive foreign interest if geopolitical and cost challenges are addressed.

BHP lifts FY26 copper guidance on record output

BHP raised its FY26 copper production guidance after delivering stronger-than-expected output across key assets, led by record concentrator throughput at Escondida and higher guidance at Antamina, while Spence and Copper SA remained on track. Favourable pricing and operational gains underpinned performance, reinforcing copper’s role as BHP’s strategic growth pillar amid accelerating electrification demand. The miner continues to invest across its copper pipeline, targeting around 2 mnt/y of attributable copper production in the 2030s, positioning the portfolio to benefit from both near-term market strength and long-term energy transition trends.

Oil prices ease amid US-EU trade jitters

Oil prices slipped in Asian trade as markets turned risk-averse over rising geopolitical and trade tensions between the US and EU, triggered by President Donald Trump’s push to annex Greenland and threats of 10% tariffs on imports from several European nations. Sentiment remained cautious ahead of the IEA’s monthly oil market report, which is widely expected to flag a potential supply glut with global output set to outpace demand growth this year and provide early guidance for 2027. On the supply side, prices found limited support after Kazakhstan temporarily halted production at the Tengiz and Korolev fields due to power issues, though the outage is expected to last up to 10 days.

Leave a Reply