- Risk appetite weakens across metals complex

- China supply concerns weigh on copper

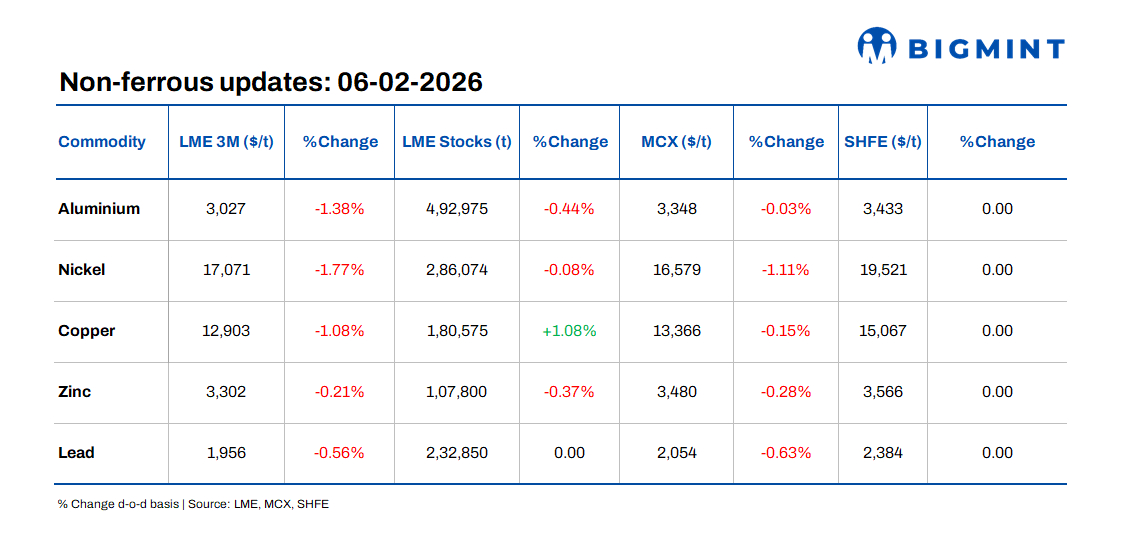

Base metals prices on the London Metal Exchange (LME) traded lower in the last session, reflecting a pullback in risk appetite across the complex. Aluminium led the declines, falling 1.38% to $3,027/t, while nickel slipped 1.77% to $17,071/t. Copper prices eased 1.08% to $12,903/t, zinc edged down 0.21% to $3,302/t, and lead declined 0.56% to $1,956/t, weighing on overall market sentiment.

LME warehouse inventories showed mixed trends, highlighting uneven supply conditions. Aluminium stocks fell 0.44% to 492,975 t, while zinc inventories declined 0.37% to 107,800 t, indicating slightly tighter availability in these segments. Nickel stocks edged marginally lower by 0.08% to 286,074 t. In contrast, copper inventories increased 1.08% to 180,575 t, pointing to improved near-term availability, while lead stocks were unchanged at 232,850 t.

Domestic market overview

In India’s non-ferrous scrap market, aluminium Tense scrap prices remained stable d-o-d across key regions. Ex-Delhi assessments were assessed to be at INR 211,000/t, while ex-Chennai prices were at INR 216,000/t. Meanwhile, Copper armature scrap prices, ex-Delhi, were down INR 25,000/t (3.3%) to INR 1,155,000/t.

Other updates

Aluminium left out of US, EU trade pacts

India’s aluminium industry was excluded from recent India–US and India–EU trade deals, but the impact is likely limited. Aluminium exports to both regions remain marginal, even under existing tariffs and CBAM. The real opportunity lies downstream, as lower tariffs on automobile imports could boost demand for aluminium-intensive components. Excess domestic processing capacity positions Indian players to benefit indirectly through higher automotive and value-added manufacturing demand.

Copper prices ease on rising China supply

Copper prices slipped 1.08% to $12,900/t pressured by rising supply in China, where refined output is expected to grow about 5% this year following a 10% rise last year. Inventories also increased across major hubs, with LME stocks climbing to a March high as material was redirected from the US to Asia, while SHFE inventories rose on the week. Despite near-term weakness, the longer-term outlook remains supportive, with Chile’s Cochilco raising its 2026 price forecast on resilient demand, a softer dollar and geopolitical risks, even as the refined market remains in surplus, according to the ICSG.

Leave a Reply