- China’s renewable energy, transportation sectors drive demand

- Inventories drop 4%, geopolitical disruptions fuel tight supply

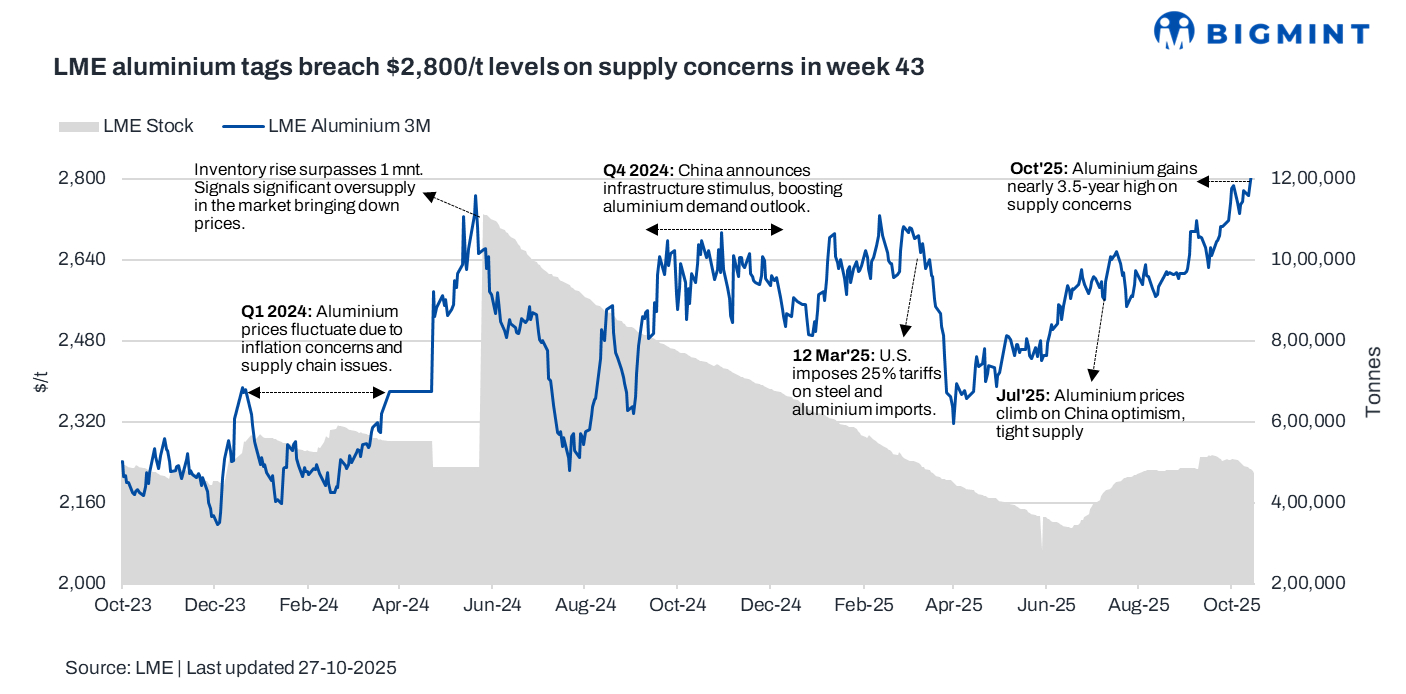

London Metal Exchange (LME) aluminium prices gained to a three-year high during week 43 of CY’25 (20-24 October 2025).

Pricing, inventory trends

LME aluminium prices averaged $2,811/tonne (t) in week 43, marking a $59/t or 2.1% rise w-o-w from week 42 (13-17 October). The week began with prices at $2,766/t, which inched up to around $2,812/t mid-week and closed strong at $2,852/t.

Supporting the price rally, LME aluminium inventories declined by 3.8% to 480,915 t in week 43 from 499,915 t in the previous week, indicating tightening supply conditions.

What’s driving the unstoppable rally in aluminium?

Aluminium prices are soaring as demand rises, led by China’s renewable energy and transportation sectors, while supply remains tight due to the metal’s energy-intensive production and geopolitical disruptions. Conflicts in Eastern Europe and the Middle East, alongside sanctions on Russia, have limited supply. A weaker dollar has boosted demand, and renewed US tariffs on aluminium imports have further strained global trade, pushing companies toward recycling and sustainable sourcing alternatives.

Additionally, as per the International Aluminium Institute (IAI), global primary aluminium production totalled 6.08 million tonnes (mnt) in September, down from 6.276 mnt in August but up from 6.028 mnt a year earlier. The global daily average output rose slightly to 202,700 t. China produced 3.644 mnt, while other Asian regions made 400,000 t.

Outlook

LME aluminium prices are expected to remain firm in the short term, supported by tightening inventories, robust demand from China’s renewable and transport sectors, and lingering geopolitical risks. Further gains are possible if supply constraints deepen, though a brief pullback toward $2,750/t levels could occur if demand eases or inventory levels stabilise.

Leave a Reply