- LME inventories increase by 4% w-o-w

- Firm US dollar pressures metal prices

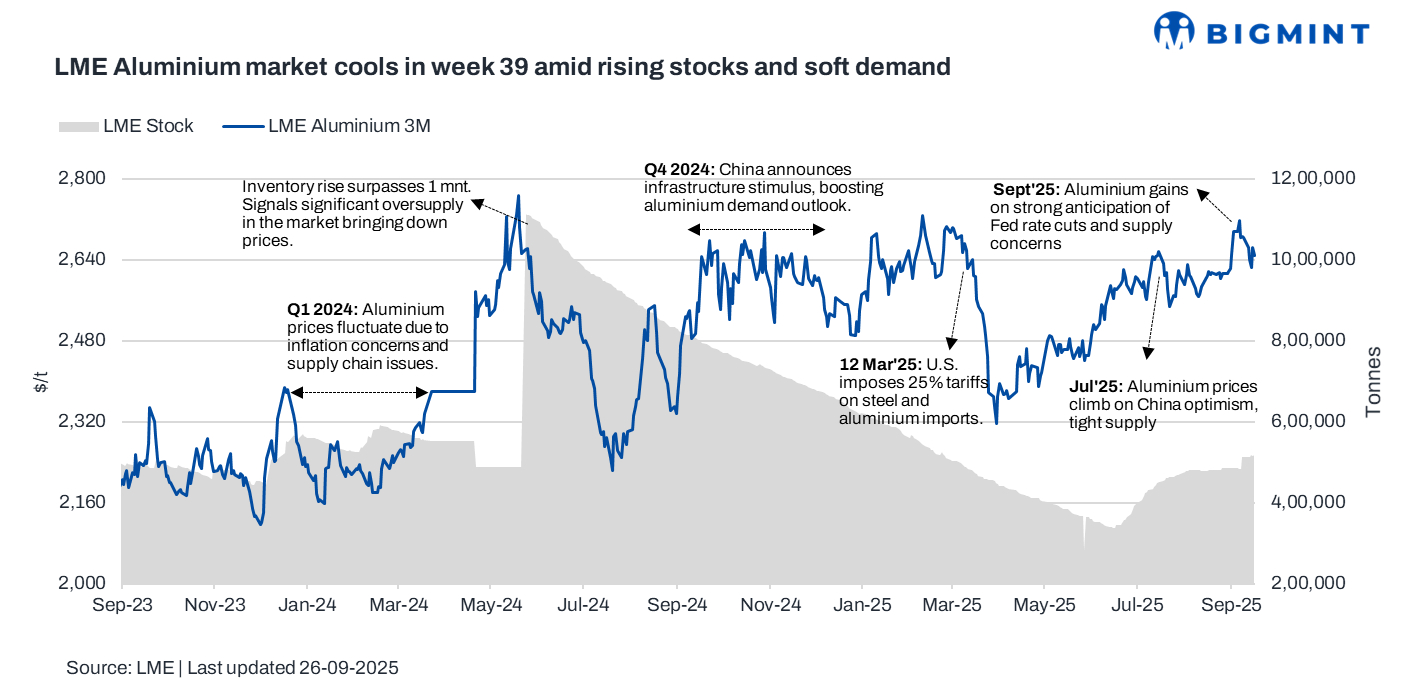

London Metal Exchange (LME) aluminium prices dipped during week 39 of CY’25 (22-26 September 2025).

LME aluminium prices eased w-o-w, weighed by firm Chinese supply data, a firmer dollar, and subdued pre-holiday trading activity.

Pricing, inventory trends

LME aluminium prices averaged $2,648/tonne (t) in week 39, decreasing by $45/t w-o-w or 2% from week 38 (15-19 September). Prices opened the week at $2,664/t, rose to around $2,625/t mid-week, and closed slightly higher at $2,648/t.

Meanwhile, aluminium stocks at LME warehouses edged up by 4% w-o-w, to 515,705 t in week 39 from 496,125 t in week 38.

Major market updates

China’s primary aluminium production rose 1.22% y-o-y in August 2025, while imports increased by 12.9% y-o-y to 320,000 t, reflecting ample supply. Exports of unwrought aluminium and related products surged to 542,000 t in July from 489,000 t in June, further adding to market pressure.

According to the International Aluminium Institute (IAI), global primary aluminium output rose 0.9% y-o-y to 6.277 mnt in August, indicating a broad-based supply increase. Meanwhile, SHFE aluminium stocks dipped 0.6% w-o-w, suggesting steady domestic demand, though not enough to offset broader market softness.

On the demand side, North American aluminium consumption declined 4.4% y-o-y in H1CY’25, partly due to weaker exports under renewed tariff pressure, adding to bearish sentiment.

With Chinese markets entering a week-long holiday and speculative activity subdued, LME aluminium faced limited buying interest, leading to a marginal price correction over the week.

Outlook

Aluminium prices may remain under pressure in the near term due to firm global supply, rising LME inventories, and weak demand from key regions such as North America. With China entering a holiday lull and speculative interest subdued, prices are likely to stay range-bound unless demand indicators improve or supply risks re-emerge.

Leave a Reply