- Demand worries outweigh supportive supply disruptions

- China’s slowing industrial momentum piles pressure on prices

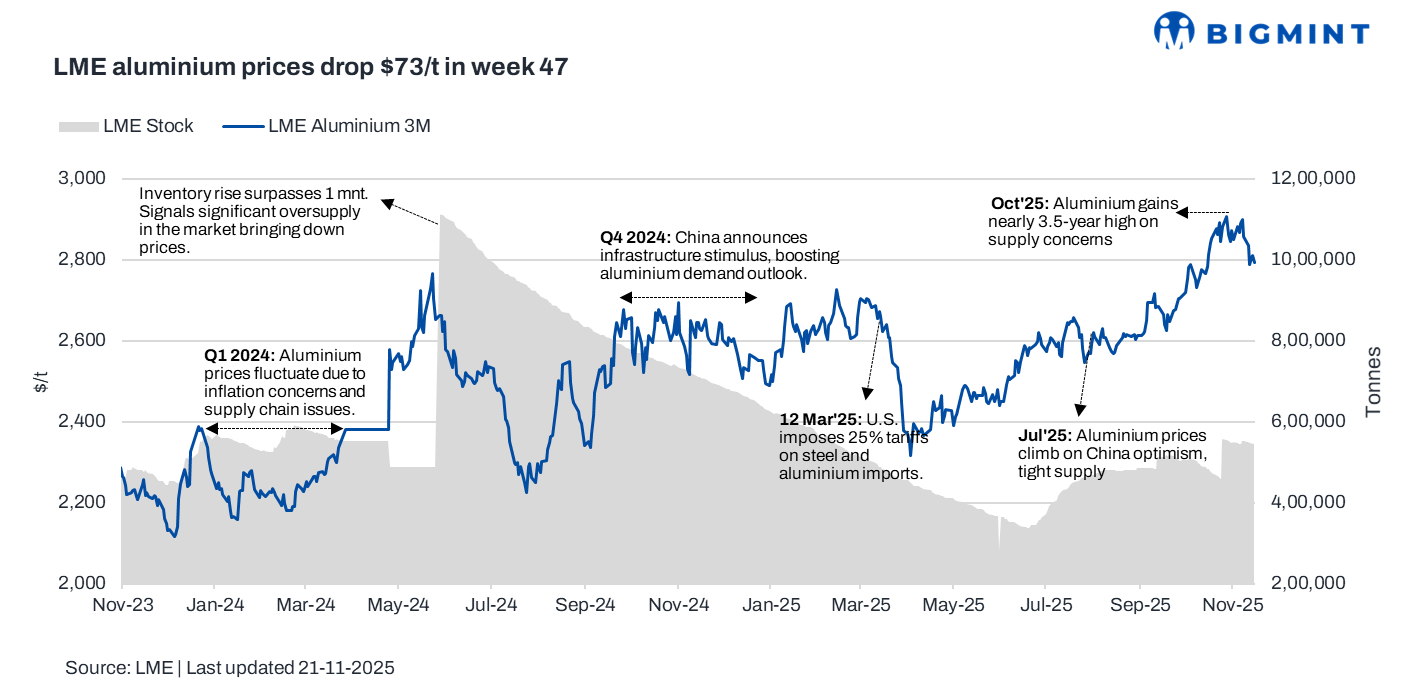

LME aluminium prices fell during week 47 of CY’25 (17-21 November). Aluminium prices fell this week as global risk sentiment weakened ahead of key US economic data releases, prompting broad selling across commodities. Soft Chinese macro indicators added pressure, overshadowing supply concerns from smelter disruptions and refinery closures that otherwise limited sharper downside in the market.

Pricing, inventory trends

LME aluminium prices averaged $2,806/tonne (t) in week 47, marking a $73/t or 2.5% drop w-o-w from week 46 (10-14 November). The week began with prices at $2,834/t, which dropped to around $2,806/t mid-week and closed at $2,792/t.

Meanwhile, LME aluminium inventories witness outflows for the week at 547,285 t from 548,420 t in week 46.

What impacted prices this week?

Aluminium prices fell this week as risk appetite weakened across global markets ahead of key US economic data releases. The broader risk-off sentiment pushed traders to reduce exposure to industrial metals, exerting downward pressure on aluminium. However, the decline was partially cushioned by persistent concerns that Chinese smelters are nearing government-imposed capacity ceilings, a factor that could limit future supply.

While China’s primary aluminium output rose 0.4% y-o-y to 3.8 mnt in October, it was down a steep 9% from September, indicating momentum loss on the supply side. Weak macroeconomic indicators from China further weighed on demand expectations, though sentiment stabilized somewhat after Beijing introduced fresh growth-support measures and the U.S. made progress in avoiding a government shutdown.

Supply disruptions also provided some support, preventing a deeper correction. The Grundartangi smelter in Iceland halted one potline due to electrical failure, Century Aluminium cut production by two-thirds, and Alcoa announced the closure of its Kwinana alumina refinery amid deteriorating bauxite grades.

SHFE aluminium stocks rose 1.4% from last week, whereas Japanese port inventories fell 3.6% to 329,100 t. China’s demand remained robust, reflected in unwrought aluminium exports of 542,000 t in July and a 10.4% y-o-y rise in October imports to 350,000 t. Cumulative January-October imports reached 3.36 mnt, up 6.1% y-o-y.

Outlook

Aluminium prices may remain rangebound in the near term as traders await key US economic data and clearer signals on China’s industrial recovery. Supply risks from smelter outages and refinery closures could offer limited support, but weak macro sentiment and uneven demand trends may cap upside. Market volatility is likely to persist into the coming weeks.

Leave a Reply