- Deliveries of Russian aluminium banned by LME in Apr’24

- SHFE stocks plunge to a 16-month low amid robust demand

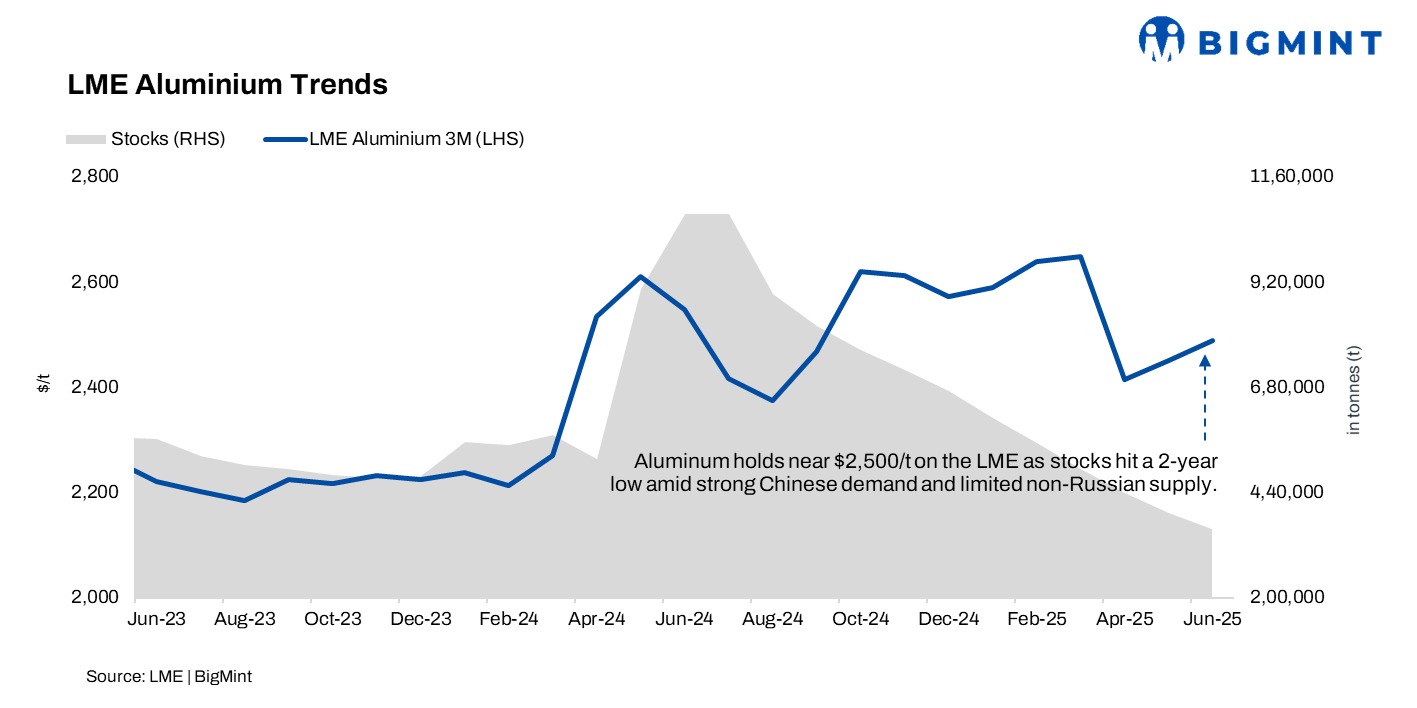

Over the past two years, the London Metal Exchange (LME) has witnessed a dramatic decline in aluminium inventories. In mid-2023, LME warehouses held over 1.3 million tonnes (mnt) of aluminium. By June 2025, this figure had nearly halved, returning to levels last seen in 2022. As a result, the market has become more turbulent beneath the surface, even though LME three-month prices have remained relatively stable at around $2,500/t. However, short-dated spreads have grown notably tight and volatile, signalling increased stress in the system.

The LME aluminium market has a long history of fierce competition among traders, especially those with significant financial resources. The landscape shifted further after the LME banned deliveries of new Russian aluminium in April 2024. This recent move echoes previous inventory battles, but the current volatility may be masking a critical market signal rather than just market “noise”.

Aluminium spreads tighten as LME stocks dwindle

Aluminium stands as the largest global base metals market, with annual consumption hovering at around 100 mnt. Traders are known for taking exceptionally large positions, and recent months have seen a mega long position disrupt nearby spread structures. The benchmark cash-to-three-months spread has moved from a comfortable contango of over $42/t in April to a small backwardation. The “tom-next” spread — a reliable indicator of market stress — reached a backwardation of $12.30/t last week.

Currently, only about 321,800 t of aluminium are available in LME warehouses, and roughly two-thirds of this is Russian-origin metal. Russian aluminium is less desirable in Western markets due to sanctions and quotas, with the US and UK imposing outright bans in April 2024 and the EU planning a full ban by the end of 2026. The status of the 323,000 t in off-warrant storage is unclear, but there is no evidence of this metal moving onto warrant to ease the tightness. Metal arrivals into the LME system have been minimal — just 150 t so far this month — indicating that efforts to draw out hidden stocks have not succeeded.

The LME’s ban on post-April 2024 Russian metal may be disrupting the usual strategy of tightening spreads to force holders to release inventory. This assumes, however, that there is ample aluminium available for delivery — a premise increasingly in doubt given the lack of significant arrivals since March.

China’s surging Russian aluminium imports

China’s role in the global aluminium market has grown more prominent. The country’s imports of Russian primary aluminium jumped from 291,000 t in 2021 to 1.13 mnt in 2024, with a further 48% y-o-y increase to 741,000 t in the first four months of 2025. This surge reflects China’s structural shift towards greater reliance on imports, as its smelters approach the government’s annual capacity cap of 45 mnt. The national run-rate has remained steady at about 44 mnt since the start of the year, while demand — especially from the solar sector — keeps the domestic market tight. Shanghai Futures Exchange (SHFE) stocks have dropped to a 16-month low of 110,000 t, and the forward curve is now in backwardation.

China is also trying to expand secondary aluminium production from scrap to offset the cap on primary output. Yet, this is complicated by changing global scrap flows, with more material heading to the US due to tariff exemptions and potential EU export tariffs. These shifts could tighten global scrap supply, forcing processors outside the US to rely more on primary metal.

The ongoing squeeze on the LME aluminium contract is just the latest in a series of major trades aimed at controlling available stocks. However, it has not succeeded in drawing more metal into the system, and the persistent inventory downtrend increasingly appears to be a genuine market signal, not just the usual churn of LME stocks.

Leave a Reply